What this calculator does

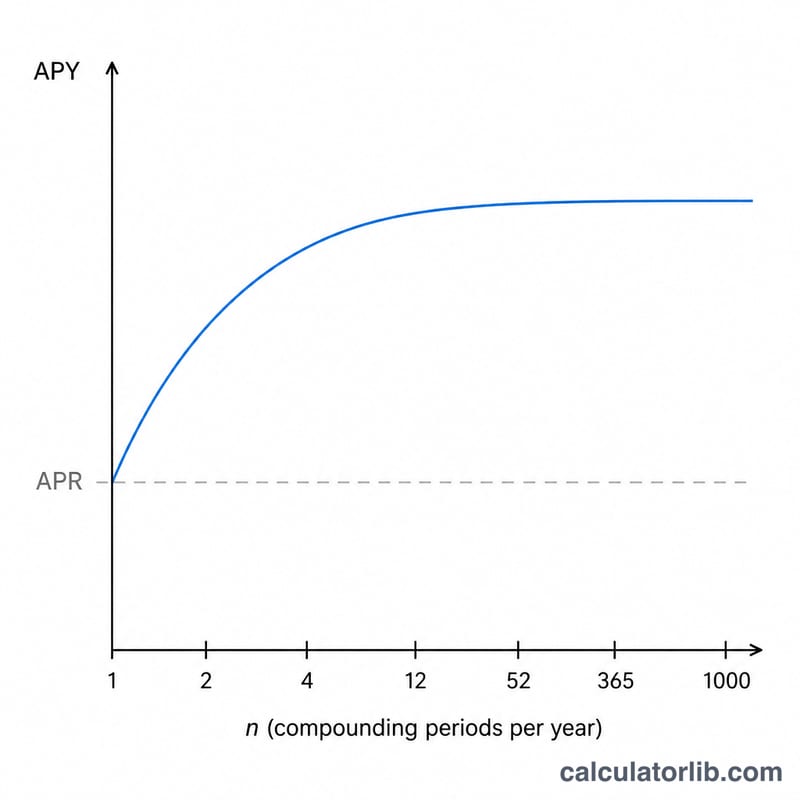

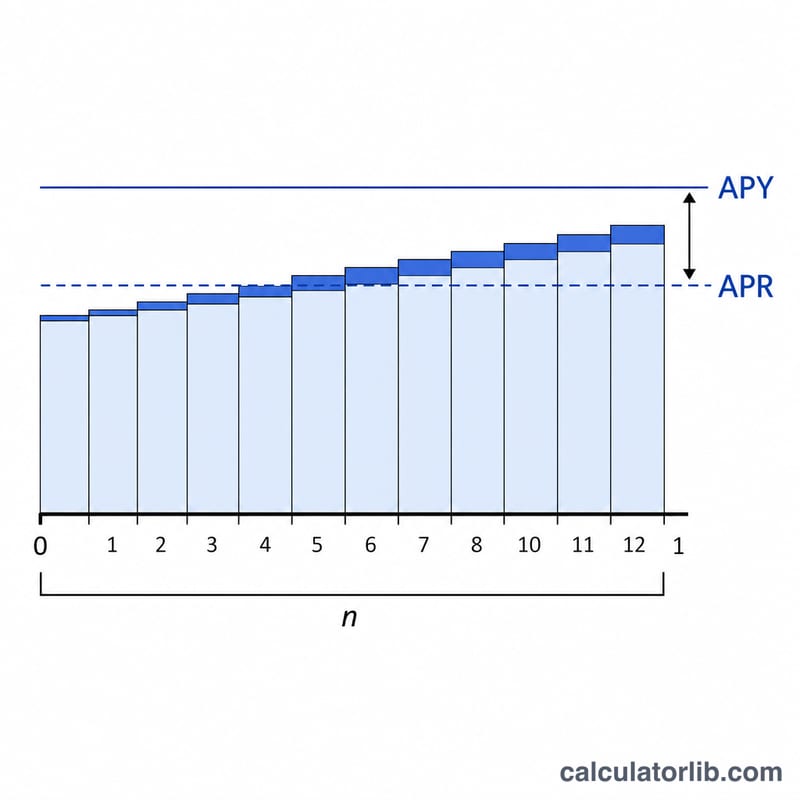

Credit cards and loans usually advertise an APR (Annual Percentage Rate), but interest is often charged more frequently than once a year — typically daily. When interest compounds, the rate you actually pay over a year is higher than the stated APR. That true figure is the APY, also called the Effective Annual Rate (EAR). This tool converts any APR into its APY for a chosen compounding frequency.

How to use it

Enter your card or loan's APR as a percentage (for example, 19.99). Choose how often interest compounds — most US credit cards compound daily (365 periods), but you can pick monthly, quarterly, or other frequencies. The calculator returns the effective annual rate and shows how much extra the compounding adds versus the headline APR.

The formula explained

The conversion is $$\text{APY} = \left(1 + \frac{\text{APR}/n}{\,}\right)^{n} - 1$$ where \(n\) is the number of compounding periods per year. Dividing the APR by n gives the periodic rate; raising the growth factor to the power n compounds it across the year; subtracting 1 leaves the net annual rate. More frequent compounding (larger n) produces a higher APY for the same APR.

Worked example

Suppose your card has an APR of 19.99% compounding daily (\(n = 365\)). The daily rate is \(0.1999/365 = 0.0005477\). Then $$\text{APY} = (1 + 0.0005477)^{365} - 1 \approx 0.22126$$ or about 22.13%. The compounding adds roughly 2.14 percentage points over the stated 19.99% APR.

Key Terms Defined

- APR (Annual Percentage Rate)

- The nominal annual interest rate stated on a card or loan agreement. It is a quoted figure that does not, by itself, account for how often interest is compounded within the year.

- APY / EAR (Effective Annual Rate)

- The actual yearly rate you pay or earn once compounding is included. APY and EAR are the same concept (APY is the consumer-facing label; EAR is the finance term). It is computed as \(\text{APY} = \left(1 + \frac{r}{n}\right)^{n} - 1\), where \(r\) is the APR as a decimal and \(n\) is the number of compounding periods per year.

- Periodic rate (APR/n)

- The interest rate applied in a single compounding period — the APR divided by the number of periods per year. For a 19.99% APR compounded daily, the daily periodic rate is \(19.99\% / 365 \approx 0.05477\%\).

- Compounding frequency (n)

- How many times per year interest is calculated and added to the balance. Common values are 1 (annual), 2 (semi-annual), 4 (quarterly), 12 (monthly), 52 (weekly), and 365 (daily). Most U.S. credit cards use daily compounding.

- Nominal vs effective rate

- The nominal rate (APR) ignores intra-year compounding; the effective rate (APY) folds it in. The two are equal only when \(n = 1\); for every \(n > 1\), the effective rate exceeds the nominal rate.

Interpreting Your APY

Your APY represents the true annual cost of carrying a balance once interest compounds on previously accrued interest. If you revolve a balance from month to month, interest charges effectively grow at the APY rather than the lower stated APR.

The gap between APR and APY widens in two situations: as the APR rises, and as compounding becomes more frequent. A low-rate card compounded monthly shows only a small gap, while a high-rate card compounded daily shows the largest spread — which is why the daily-compounding column in the table above is always the highest in each row.

Crucially, APY only matters if you carry a balance. Paying your statement in full each billing cycle keeps you within the grace period, so no interest accrues at all — neither at the APR nor the APY. The effective rate becomes your real cost only once a balance revolves past the due date.

Finally, APY measures interest alone. It excludes annual fees, late fees, cash-advance fees, and balance-transfer fees, and it assumes a constant balance over the year. Real-world cards have changing balances, new purchases, and payments, so your actual dollar interest will differ from a flat APY applied to a single starting balance. To estimate dollar charges on a specific balance, use a daily-interest or payoff calculator alongside this conversion. This is general information, not financial advice.

FAQ

Is APY always higher than APR? Yes, whenever there is more than one compounding period per year. With annual compounding (\(n = 1\)), APY equals APR.

Why do credit cards use daily compounding? Most US issuers apply a daily periodic rate (\(\text{APR} \div 365\)) to your balance each day, which makes the effective rate higher than the quoted APR.

Does this include fees? No. This converts the interest rate only. APR that bundles fees won't reflect those fees in the APY figure shown here.