What is the Effective Annual Rate (EAR)?

The effective annual rate (EAR), also called the annual equivalent rate or effective APR, is the true yearly interest you pay or earn once compounding is taken into account. A nominal APR of 12% compounded monthly is not actually 12% per year — because interest is charged on interest each month, the real cost is slightly higher. EAR makes rates with different compounding frequencies directly comparable.

How to use this calculator

Enter the nominal APR (the quoted annual rate) as a percentage, then choose how often interest compounds — annually, semi-annually, quarterly, monthly, weekly, or daily. The calculator returns the effective annual rate, plus the difference between the EAR and the stated APR so you can see the compounding "penalty."

The formula explained

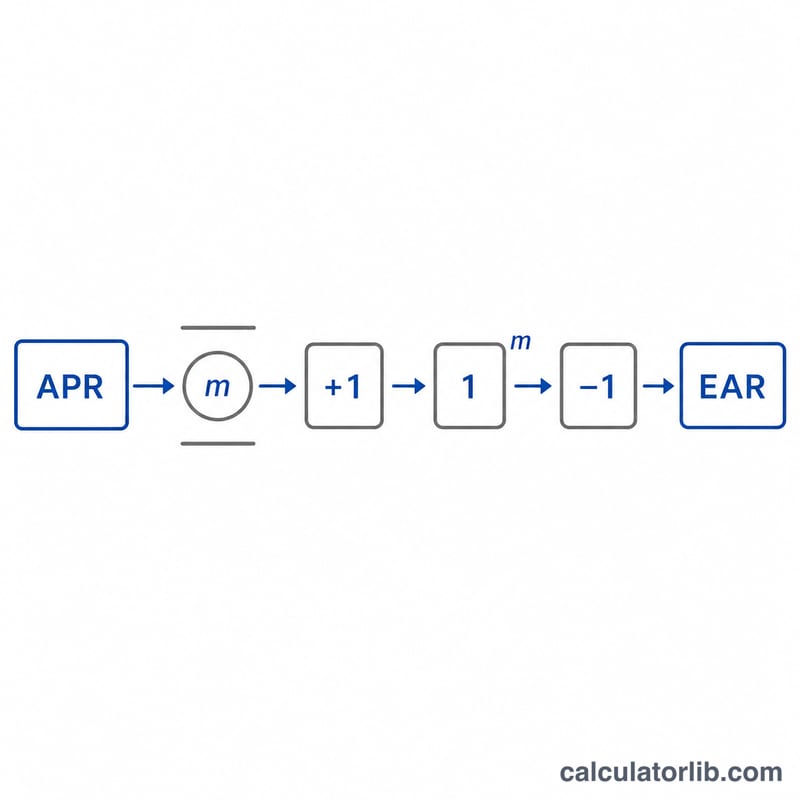

The EAR is calculated as $$\text{EAR} = \left(1 + \frac{\text{APR}}{m}\right)^{m} - 1$$ where APR is the nominal rate as a decimal and \(m\) is the number of compounding periods per year. Dividing APR by \(m\) gives the periodic rate; raising the growth factor to the power \(m\) compounds it across the whole year; subtracting 1 leaves just the interest portion.

Worked example

Suppose a credit card quotes a 12% APR compounded monthly (\(m = 12\)). The monthly rate is \(0.12 / 12 = 0.01\). Then $$\text{EAR} = (1 + 0.01)^{12} - 1 = 1.126825 - 1 = 0.126825$$ or about 12.6825%. So the real annual cost is roughly 0.68 percentage points higher than the advertised 12%.

FAQ

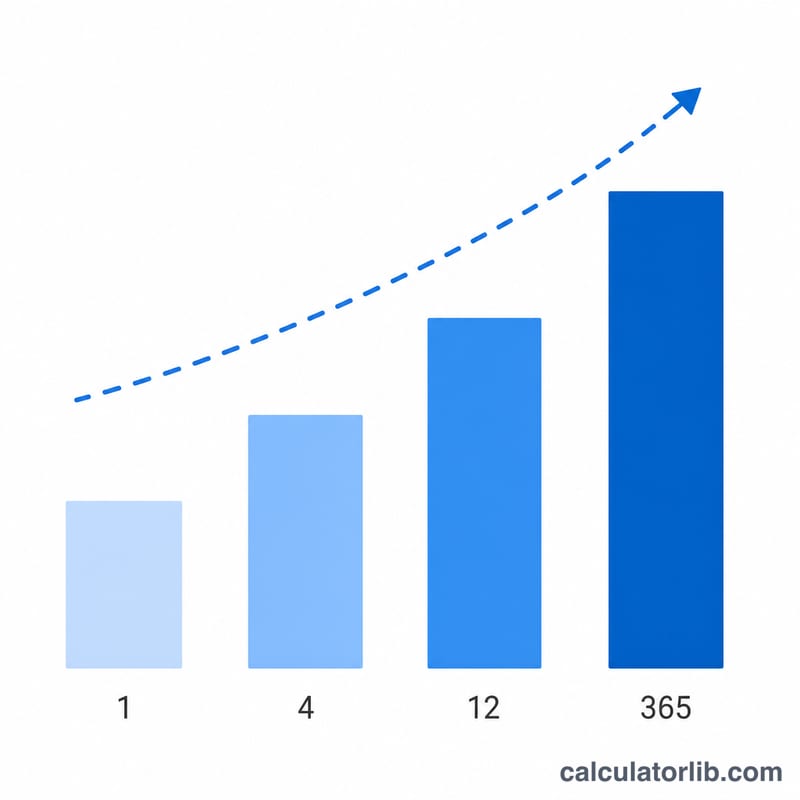

Is EAR always higher than the nominal APR? Yes, whenever there is more than one compounding period per year. With annual compounding (\(m = 1\)) the EAR equals the APR.

Does more frequent compounding increase EAR? Yes — daily compounding produces a slightly higher EAR than monthly for the same nominal rate, approaching the continuous-compounding limit \(e^{\text{APR}} - 1\).

Is EAR the same as APY? Effectively yes. APY (annual percentage yield) for savings and EAR for borrowing use the same compounding math.