What is the Effective Annual Rate (EAR)?

The Effective Annual Rate (EAR), also called the annual equivalent rate, is the true yearly interest rate you earn or pay once the effect of compounding is included. A bank may quote a nominal rate (APR) of 6%, but if interest compounds monthly you actually earn slightly more than 6% over the year. EAR turns any quoted rate plus its compounding frequency into a single, comparable number so you can line up different loans, savings accounts, or credit cards on equal terms.

How to use this calculator

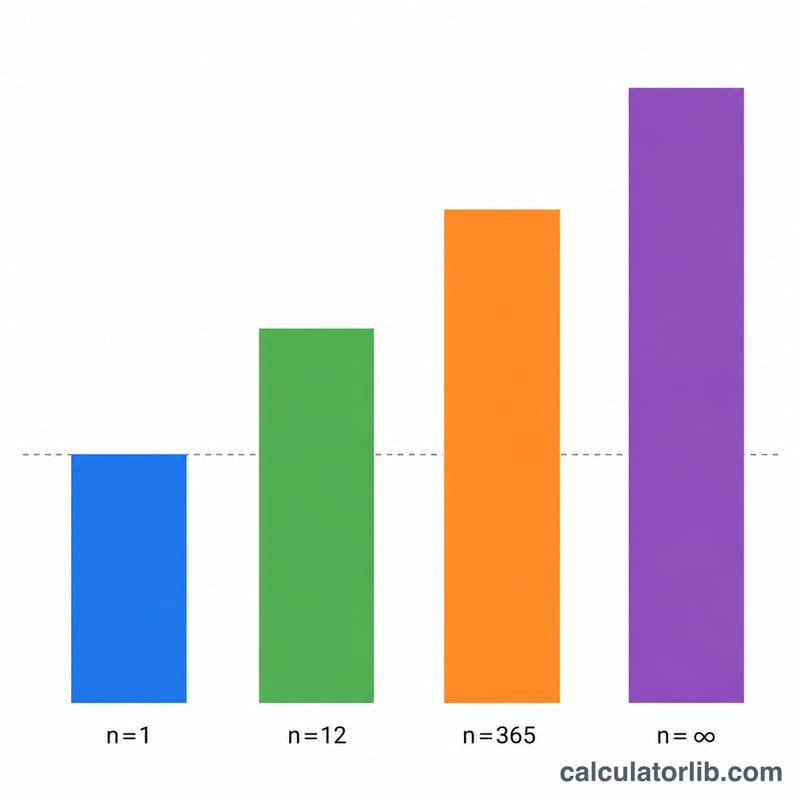

Enter the nominal (stated) annual interest rate as a percentage — this is the APR your bank or lender quotes. Then choose how often interest is compounded: annually, semiannually, quarterly, monthly, daily, or continuously. Press calculate and the tool returns the EAR as a percentage (and as a decimal). The more frequently interest compounds, the higher the EAR for the same nominal rate.

The formula explained

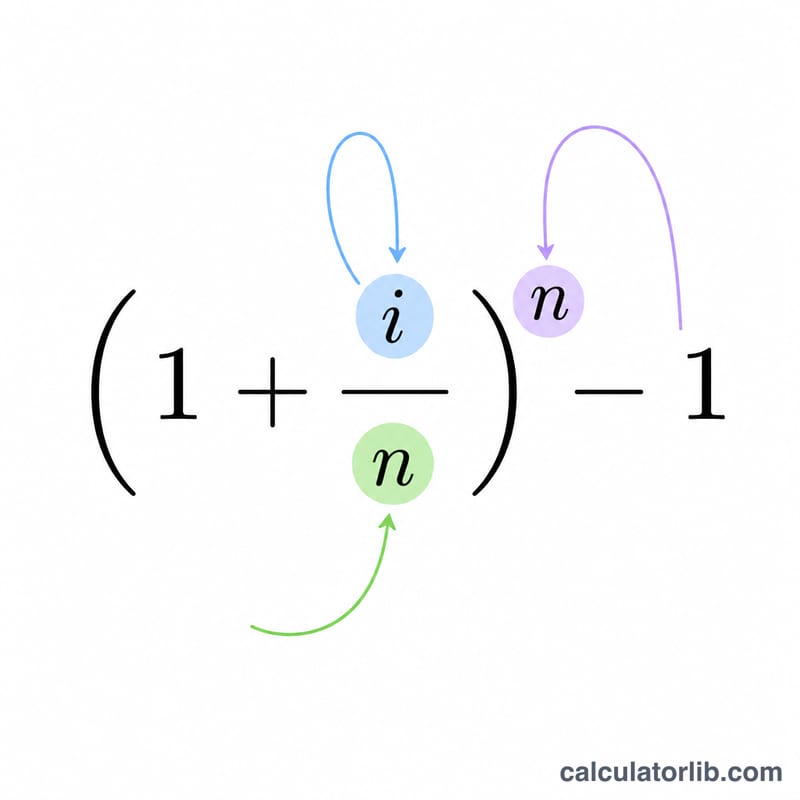

First convert the nominal rate to a decimal: \( i = \text{nominalRate} / 100 \). For finite compounding \(n\) times per year, $$\text{EAR} = \left(1 + \frac{i}{n}\right)^{n} - 1.$$ For continuous compounding the limit as \(n\) grows without bound gives $$\text{EAR} = e^{\,i} - 1,$$ where \(e \approx 2.71828\). Multiply the result by 100 to express it as a percentage. When \(n = 1\) (annual), EAR equals the nominal rate exactly; for \(n > 1\) with a positive rate, EAR is always larger.

Worked example

Suppose the nominal rate is 6% compounded monthly. Then \(i = 0.06\) and \(n = 12\). $$\text{EAR} = \left(1 + \frac{0.06}{12}\right)^{12} - 1 = 1.005^{12} - 1 = 1.0616778 - 1 = 0.0616778,$$ or about 6.1678%. With continuous compounding at the same 6%, \(\text{EAR} = e^{0.06} - 1 = 0.0618365\), or about 6.1837% — the highest possible EAR for that nominal rate.

FAQ

Is EAR the same as APR? No. APR is the nominal (stated) rate ignoring intra-year compounding. EAR accounts for compounding, so \(\text{EAR} \geq \text{APR}\) whenever interest compounds more than once a year.

Why does continuous compounding give the largest rate? As compounding becomes infinitely frequent the discrete formula converges to \(e^{i} - 1\), the mathematical upper bound for a given nominal rate.

What if the nominal rate is 0%? EAR is 0% regardless of frequency — there is no interest to compound.