What Is the Effective Annual Interest Rate?

The Effective Annual Rate (EAR), also called Annual Percentage Yield (APY), is the true annual interest rate you earn or pay once the effect of compounding is included. A stated (nominal) rate of 5% compounded monthly is not actually 5% per year — because interest earns interest, the real yield is slightly higher. This calculator converts any nominal annual rate into its effective equivalent for any compounding frequency.

How to Use It

Enter the nominal annual interest rate as a percentage, then choose how often interest compounds (annually, semi-annually, quarterly, monthly, weekly, or daily). The calculator returns the effective annual rate so you can compare products quoted at different compounding frequencies on an apples-to-apples basis.

The Formula Explained

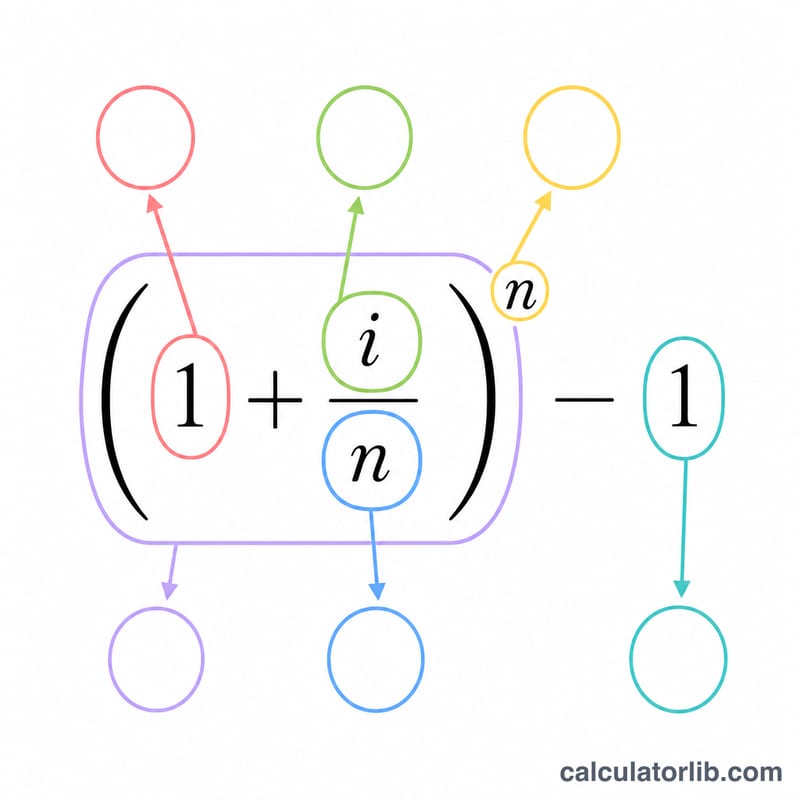

The formula is $$\text{EAR} = \left(1 + \frac{i}{n}\right)^{n} - 1$$ where \(i\) is the nominal annual rate expressed as a decimal and \(n\) is the number of compounding periods per year. Dividing \(i\) by \(n\) gives the periodic rate; raising to the power of \(n\) compounds it across the whole year; subtracting 1 isolates the growth portion. Multiply by 100 to express the result as a percentage.

Worked Example

Suppose a savings account pays a nominal 5% compounded monthly. Here \(i = 0.05\) and \(n = 12\). The periodic rate is \(0.05/12 \approx 0.0041667\). Then $$\text{EAR} = (1 + 0.0041667)^{12} - 1 = 1.0511619 - 1 = 0.0511619,$$ or about 5.1162%. So your money actually grows by roughly 5.12% per year, not 5%.

FAQ

What is the difference between APR and APY? APR (nominal rate) ignores intra-year compounding; APY (effective rate) includes it. APY is always equal to or greater than APR.

Does more frequent compounding always help? Yes — for the same nominal rate, daily compounding yields a slightly higher EAR than monthly, which yields more than annual.

Is the result the same as continuous compounding? No. Continuous compounding uses \(e^{i} - 1\). This tool uses discrete periods, which approach but never quite reach the continuous limit.