What is the ACB Loan Total Cost Calculator?

This calculator shows the full picture of an amortizing loan: not just the monthly payment, but the total cost you will repay over the life of the loan and how much of that is interest. It works for mortgages, car loans, personal loans, and any fixed-rate installment loan with equal monthly payments.

How to use it

Enter the loan amount (the principal you borrow), the annual interest rate as a percentage, and the term in years. The calculator converts the term to months and the annual rate to a monthly rate, computes the equal monthly installment (EMI), then multiplies it by the number of payments to get the total cost.

The formula explained

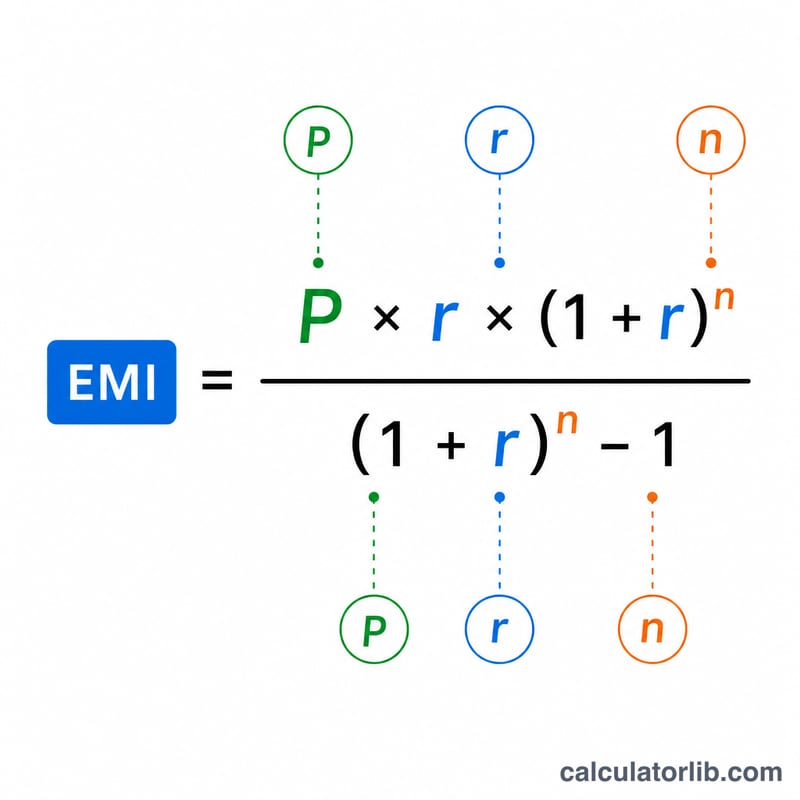

The EMI formula is $$\text{EMI} = \dfrac{P \cdot r \cdot (1+r)^n}{(1+r)^n - 1}$$ where \(P\) is the principal, \(r\) is the monthly interest rate (annual rate \(\div 12 \div 100\)), and \(n\) is the total number of monthly payments (years \(\times 12\)). Total cost \(= \text{EMI} \times n\), and total interest \(= \text{total cost} - P\). If the rate is 0%, the EMI is simply \(P \div n\).

Worked example

Borrow $200,000 at 6% annual interest over 30 years. Monthly rate \(r = 0.005\), \(n = 360\). The EMI comes to about $1,199.10. Total cost $$= 1{,}199.10 \times 360 \approx \$431{,}676$$ of which about $231,676 is interest — more than the amount originally borrowed.

Understanding Your Total Loan Cost

The total cost of a loan is simply the sum of everything you pay back over its life. Mechanically it equals the monthly payment multiplied by the number of payments, but conceptually it breaks down into two parts:

$$\text{Total Cost} = \text{Principal} + \text{Total Interest}.$$The principal is the amount you actually borrowed; the rest is interest — the lender's charge for the use of that money over time.

A longer term lowers the monthly payment but raises total interest. Stretching repayment over more months reduces each installment, which can ease monthly budgeting, but because the balance is paid down more slowly, interest accrues on a larger outstanding balance for longer. The 30-year rows above cost far more in total than the 15-year rows at the same rate, even though the monthly payment is smaller.

Interest can exceed the principal. On long-term, high-rate loans it is entirely possible to pay more in interest than you originally borrowed — the 6%/30-year and 8%/30-year examples both cross that line. This is a direct consequence of compounding over a long horizon.

This figure follows the standard amortization model: each fixed payment covers the interest due that month first, and the remainder reduces the principal. Early payments are mostly interest; later payments are mostly principal. An amortization schedule shows this split month by month and explains why total interest is front-loaded.

What this calculator does not include: the result reflects only principal and interest at the stated nominal rate. It excludes origination fees, closing costs, insurance, taxes, and other charges. Because of those, the true cost of borrowing — captured by the APR — can be higher than the rate entered here. This is general educational information, not personal financial advice.

Key Terms Explained

- Principal (P)

- The original amount borrowed, before any interest is added.

- Annual interest rate

- The nominal yearly rate charged on the outstanding balance, entered as a percentage (e.g. 6 for 6%).

- Monthly rate (r)

- The annual rate converted to a per-month decimal: \(r = \dfrac{\text{rate}}{1200}\). For a 6% annual rate, \(r = 0.005\).

- Term / number of payments (n)

- The total count of monthly installments, \(n = 12 \times \text{years}\). A 30-year loan has \(n = 360\) payments.

- EMI (Equated Monthly Installment)

- The fixed monthly payment that fully repays the loan over its term, given by \(M = P \cdot \dfrac{r(1+r)^{n}}{(1+r)^{n}-1}\).

- Total cost

- The sum of all payments over the loan: \(M \times n\). It equals principal plus total interest.

- Total interest

- The portion of total cost that is not principal: \(\text{Total Cost} - P\).

- Amortization

- The process of repaying a loan through equal periodic payments, where each payment is split between interest on the current balance and reduction of the principal.

- Fixed vs. variable rate

- A fixed rate stays constant for the life of the loan, so EMI and total cost are known in advance. A variable rate can change with market conditions, making future payments and total cost uncertain. This calculator assumes a fixed rate.

FAQ

Does this include fees or insurance? No. It covers principal and interest only. Origination fees, insurance, and taxes are extra.

What if my rate changes? This assumes a fixed rate. For variable-rate loans the result is an estimate based on the rate you enter.

Can I use months instead of years? Enter a fractional year — for example 1.5 years for 18 months.