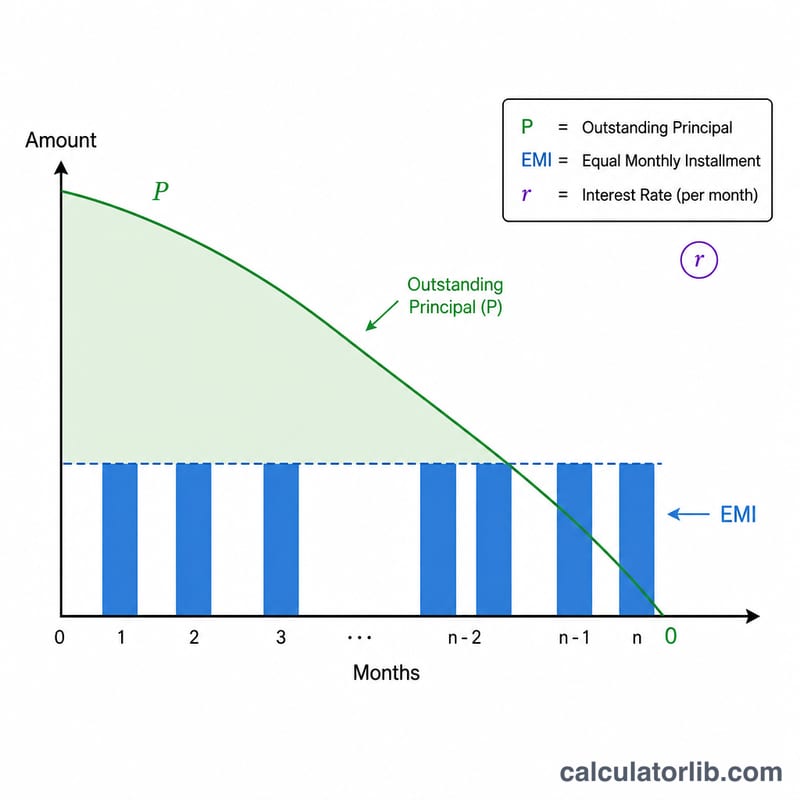

What is the ACB Loan Tenure Calculator?

The ACB Loan Tenure Calculator tells you how many months it will take to fully repay a loan given the loan amount (principal), your fixed monthly installment (EMI), and the annual interest rate. Instead of fixing the term and solving for the payment, it fixes the payment and solves for the term — useful when you already know how much you can afford to pay each month.

How to use it

Enter the outstanding principal, the monthly EMI you intend to pay, and the annual interest rate (as a percentage). The calculator converts the annual rate to a monthly rate and returns the number of months required to clear the balance, plus the equivalent years.

The formula explained

The number of months is derived from the amortization equation:

$$n = -\dfrac{\ln\left(1 - \dfrac{P \cdot r}{EMI}\right)}{\ln(1 + r)}$$

where \(P\) is the principal, \(EMI\) is the monthly payment, and \(r\) is the monthly interest rate = annual rate \(\div 12 \div 100\). For the loan to ever be repaid, the monthly EMI must exceed the first month's interest (\(P \cdot r\)); otherwise the term is infinite.

Worked example

Suppose you borrow 100,000 at 12% annual interest and pay 2,000 per month. The monthly rate \(r = 0.12 / 12 = 0.01\). Then \(P \cdot r = 1{,}000\), so \(P \cdot r / EMI = 0.5\).

$$n = -\dfrac{\ln(1 - 0.5)}{\ln(1.01)} = -\dfrac{\ln(0.5)}{\ln(1.01)} = \dfrac{0.693147}{0.00995033} = 69.66 \text{ months (about 5.8 years).}$$

Key Terms and Variables

- Principal (P)

- The original amount borrowed (the outstanding loan balance at the start). In this calculator it is entered in the principal field.

- EMI (Equated Monthly Installment)

- The fixed amount paid each month, covering both interest and principal repayment. For the loan to be repayable, the EMI must be greater than the first month's interest charge, \(P \cdot r\).

- Annual interest rate

- The nominal yearly interest rate on the loan, expressed as a percentage (the rate field). It is divided into monthly periods before being applied.

- Monthly rate (r)

- The per-month interest rate used in the formula, computed as \(r = \dfrac{\text{annual rate}}{12 \times 100} = \dfrac{\text{annual rate}}{1200}\). For example, a 12% annual rate gives \(r = 0.01\) per month.

- Tenure (n)

- The number of monthly payments required to clear the loan — the value this calculator solves for. It is generally rounded up to a whole month.

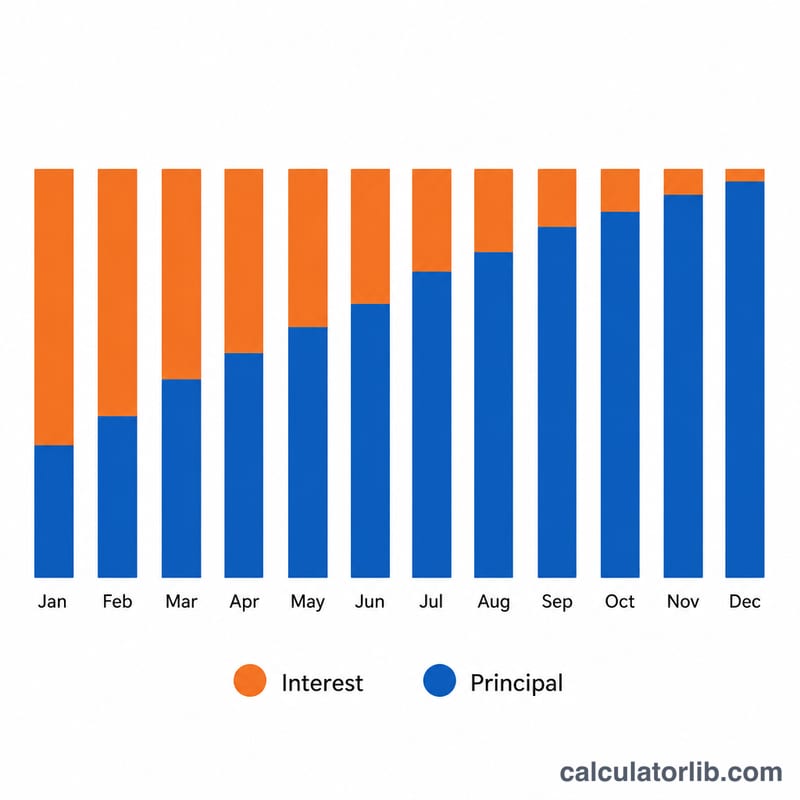

- Amortization

- The process of repaying a loan through fixed periodic payments where each payment is split between interest on the remaining balance and a reduction of the principal. Early payments are interest-heavy; later payments are principal-heavy.

Interpreting Your Result

The result \(n\) is the number of monthly installments needed to fully repay the loan at the EMI and rate you entered. Dividing by 12 converts it to years — for instance, a tenure of 93 months is \(93 \div 12 = 7.75\) years, or about 7 years and 9 months.

Rounding the final month. The formula usually produces a fractional value (e.g. 92.4 months). Because payments occur in whole monthly steps, the tenure is rounded up to the next whole number. The final installment is then typically smaller than a full EMI, since only the small remaining balance plus its last month of interest is left to pay.

Total interest paid. Once the number of payments is known, the approximate total interest over the life of the loan is the sum of all payments minus the amount borrowed:

$$\text{Total interest} = (\text{EMI} \times n) - P$$For example, paying an EMI of 2,000 for 63 months on a 100,000 loan gives total payments of \(2{,}000 \times 63 = 126{,}000\) and total interest of about \(126{,}000 - 100{,}000 = 26{,}000\) (the exact figure differs slightly because the last payment is partial).

The infinite-term flag. If the calculator reports that the loan can never be repaid, it means the chosen EMI is less than or equal to the first month's interest, \(P \cdot r\). In that case every payment is fully consumed by interest (or less), so the principal never decreases and the tenure has no finite solution. Raising the EMI above \(P \cdot r\) is required for the loan to amortize.

This page provides general information about loan mathematics and is not financial advice.

FAQ

What if my EMI is too low? If the monthly EMI is less than or equal to the monthly interest charge (\(P \cdot r\)), the loan principal never decreases and the term is infinite — the calculator will flag this.

Is the result in whole months? The raw result is a precise (fractional) number of months; in practice you would round up to the next whole month for the final smaller payment.

Does it include fees? No. It models pure interest-plus-principal amortization and excludes processing fees, insurance, or penalties.