What This Calculator Does

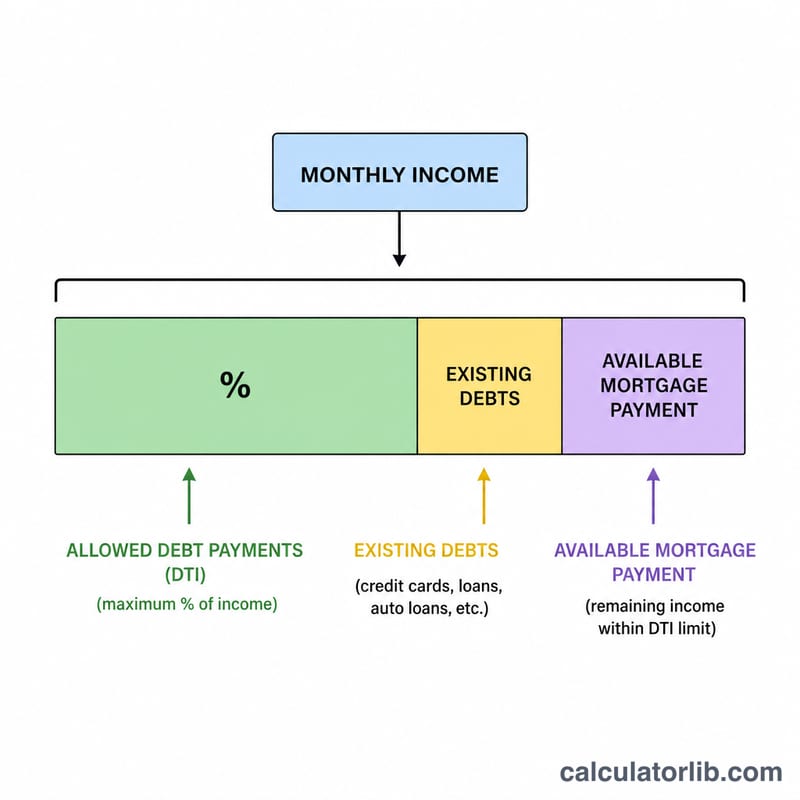

The ACB Mortgage Affordability Calculator estimates the largest home price and mortgage loan you can realistically afford. It works backwards from how much you can pay each month: it applies a debt-to-income (DTI) ratio to your gross monthly income, subtracts your existing debt payments, and converts the remaining affordable payment into a maximum loan using the standard mortgage present-value formula. Finally, it grosses the loan up by your down payment percentage to reveal the total home price.

How to Use It

Enter your gross monthly income and existing monthly debt obligations (car loans, student loans, credit card minimums). Set the maximum DTI ratio your lender allows (36% is a common conservative figure, though some programs go higher). Add the annual interest rate, the loan term in years, and your planned down payment percentage. The calculator returns your maximum affordable home price, the loan amount, the monthly payment that fits your budget, and the estimated down payment.

The Formula Explained

First, the affordable monthly payment is \(\text{EMI} = \text{Income} \times (\text{DTI}/100) - \text{Debts}\). The monthly interest rate is \(r = \text{annual rate} / 1200\) and the number of payments is \(n = \text{years} \times 12\). The maximum loan is the present value of that payment stream: $$\text{MaxLoan} = \text{EMI} \times \dfrac{(1+r)^n - 1}{r(1+r)^n}$$ Because the loan only covers part of the price, the price is $$\text{MaxPrice} = \dfrac{\text{MaxLoan}}{1 - \frac{\text{down\%}}{100}}$$

Worked Example

With $6,000 monthly income, $500 of existing debt, a 36% DTI, a 6.5% rate over 30 years and a 20% down payment: the affordable payment is $$6{,}000 \times 0.36 - 500 = \$1{,}660$$ At \(r = 0.0054167\) and \(n = 360\), the maximum loan is about $262,600, giving a home price of roughly $328,300 with a $65,700 down payment.

Key Terms Defined

- Gross monthly income

- Total income before taxes and deductions, expressed per month. Lenders qualify borrowers on gross rather than net (take-home) pay.

- Debt-to-income (DTI) ratio

- The share of gross monthly income consumed by debt payments, written as a percentage. It is the lever that sets how much of your income can go toward housing.

- EMI / affordable payment

- The Equated Monthly Installment a lender will let you devote to the mortgage. Here it equals income × DTI − existing debts, leaving room for the housing payment after other obligations.

- Principal & interest (P&I)

- The core mortgage payment: principal repays the borrowed balance and interest is the lender's charge on the outstanding amount. This calculator's payment covers P&I only.

- Present value of a payment stream

- The lump-sum loan today that a fixed series of future payments is worth, discounted at the loan's monthly rate. The factor \(\frac{(1+r)^n-1}{r(1+r)^n}\) converts an affordable monthly payment into a maximum loan.

- Down payment percentage

- The portion of the purchase price you pay up front in cash. Since the loan covers the rest, max price = max loan ÷ (1 − down% / 100).

- Loan term

- The number of years over which the mortgage is repaid (multiplied by 12 to get \(n\) monthly payments). Longer terms lower each payment but raise total interest.

Interpreting Your Result

The figure this tool returns is a pre-tax-and-insurance estimate built on principal and interest alone. A lender's qualifying calculation is stricter because it counts PITI — Principal, Interest, property Taxes and homeowner's Insurance — plus any HOA dues and mortgage insurance. Because taxes and insurance share the same monthly budget as P&I, the maximum price you actually qualify for is typically lower than the unadjusted estimate here.

It also helps to know which DTI a lender is applying:

- Front-end (housing) DTI measures only the housing payment against gross income. A 28% front-end cap is a common conventional guideline.

- Back-end (total) DTI measures all monthly debt — housing plus car loans, student loans, credit cards and the like — against gross income. The DTI you enter in this calculator behaves like a back-end figure because existing debts are subtracted from the affordable payment.

The two thresholds you will see most often are 36% and 43%. A 36% back-end ratio reflects the traditional conservative limit many conventional lenders prefer and leaves a comfortable cushion. A 43% ratio is the widely cited upper bound associated with the Qualified Mortgage standard; many loans still go higher with compensating factors, but 43% is a practical ceiling for routine approval. Pushing toward the higher cap raises your borrowing power but also your monthly risk if income drops or rates reset.

Finally, real underwriting weighs more than ratios: credit score, cash reserves (months of payments left after closing), employment stability and down payment size all influence the offer. Treat this estimate as a planning starting point, confirm the rate and term with a lender, and budget separately for closing costs and an emergency reserve. This is general educational information, not personalized financial advice.

FAQ

Is this an approval guarantee? No. It is an estimate; lenders also weigh credit score, property taxes, insurance and reserves.

Should I include taxes and insurance? This model treats EMI as principal and interest only. Reduce your DTI input to leave room for taxes and insurance.

What DTI should I use? Many lenders cap total DTI around 36–43%. A lower figure gives a safer, more sustainable budget.