What This Reverse Mortgage Calculator Does

This calculator estimates how much you could borrow against your home through a reverse mortgage — a loan product available to U.S. homeowners aged 62 and over. It uses just three inputs to project your maximum loan amount, a simplified monthly payment, total interest and the total amount you would eventually owe. It is designed for quick retirement planning, not as a formal loan offer.

The Inputs You Provide

- Home Value: The current market value of your home in dollars.

- Age: Your age in years. Reverse mortgages in the U.S. start at age 62, and older borrowers qualify for a higher percentage of their home value.

- Interest Rate (%): The annual interest rate applied to the loan, used to estimate the interest that accrues over the term.

The Formula Explained

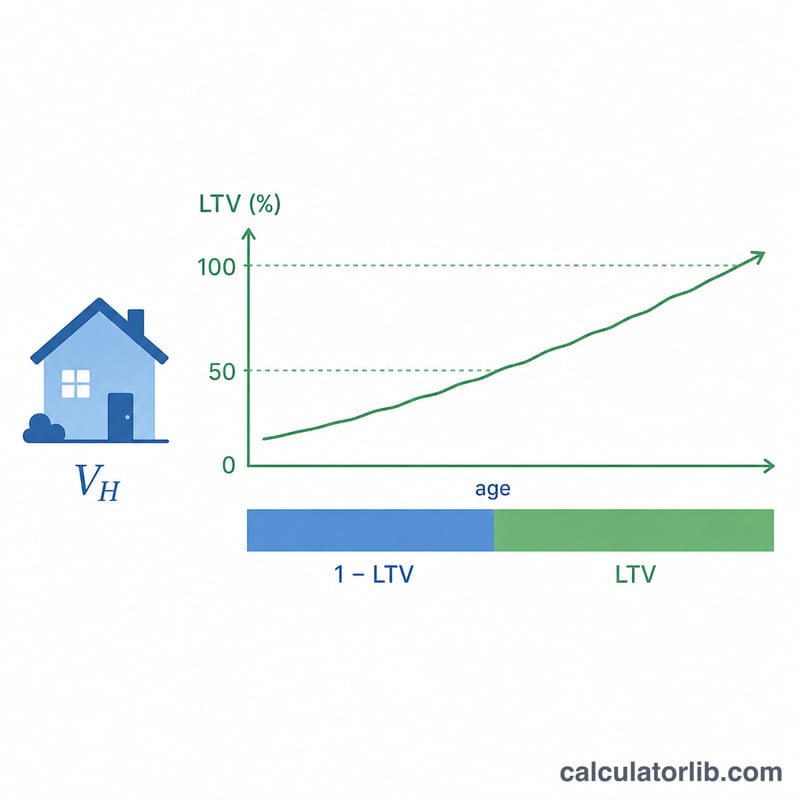

The calculator first sets a loan-to-value (LTV) ratio based on your age:

- Under 62: 0% — you don't qualify.

- Age 62 to 90: \(0.50 + (\text{age} - 62) \times 0.01\), so the ratio rises 1% per year of age.

- Over 90: capped at 75%.

It then calculates:

- Max Loan Amount $$\text{Max Loan} = \text{Home Value} \times \text{LTV}$$

- Monthly Payment $$\text{Monthly} = \frac{\text{Max Loan Amount}}{240} \quad (\text{a 20-year, 240-month term})$$

- Total Interest $$\text{Total Interest} = \text{Max Loan Amount} \times \frac{\text{Rate}}{100} \times 20 \text{ years}$$

- Total Owed $$\text{Total Owed} = \text{Max Loan Amount} + \text{Total Interest}$$

Worked Example

Suppose your home is worth $400,000, you are 70 years old, and the interest rate is 6%.

- LTV ratio $$0.50 + (70 - 62) \times 0.01 = 0.58$$

- Max Loan Amount $$\$400{,}000 \times 0.58 = \$232{,}000$$

- Monthly Payment $$\frac{\$232{,}000}{240} = \$966.67$$

- Total Interest $$\$232{,}000 \times 0.06 \times 20 = \$278{,}400$$

- Total Owed $$\$232{,}000 + \$278{,}400 = \$510{,}400$$

Frequently Asked Questions

Why does my age matter so much? Older borrowers are expected to draw on the loan for fewer years, so lenders allow a larger share of the home's value. This calculator reflects that by raising the LTV ratio 1% per year from age 62.

Do I really make monthly payments on a reverse mortgage? In a real reverse mortgage you typically do not — the balance is repaid when you sell, move out, or pass away. The "monthly payment" here is a simplified figure spreading the loan over 240 months to help you visualize the scale.

Is this an exact quote? No. Actual reverse mortgage limits depend on FHA lending caps, your specific interest rate, fees, and a HUD-approved appraisal. Use these results as a planning estimate and confirm details with a licensed lender.