What Is the Mortgage Points Calculator?

Discount points are upfront fees you pay your lender at closing to "buy down" your mortgage interest rate. One point costs 1% of the loan amount and typically lowers your rate by a fraction of a percent. This calculator (US-style fixed-rate mortgages) tells you exactly what the points cost, how much you save each month, and how many months it takes to break even.

How to Use It

Enter your loan amount, the number of discount points, the interest rate without points, the (lower) rate with points, and the loan term in years. The calculator computes the monthly principal-and-interest payment at each rate, the monthly savings, and the break-even point in months.

The Formula

The cost of points is \(\text{loan} \times (\text{points} \div 100)\). Each monthly payment uses the amortization formula

$$M = \frac{P \cdot i \cdot (1+i)^{n}}{(1+i)^{n} - 1}$$where \(i\) is the monthly rate and \(n\) the number of payments. The break-even is cost of points \(\div\) monthly savings.

Worked Example

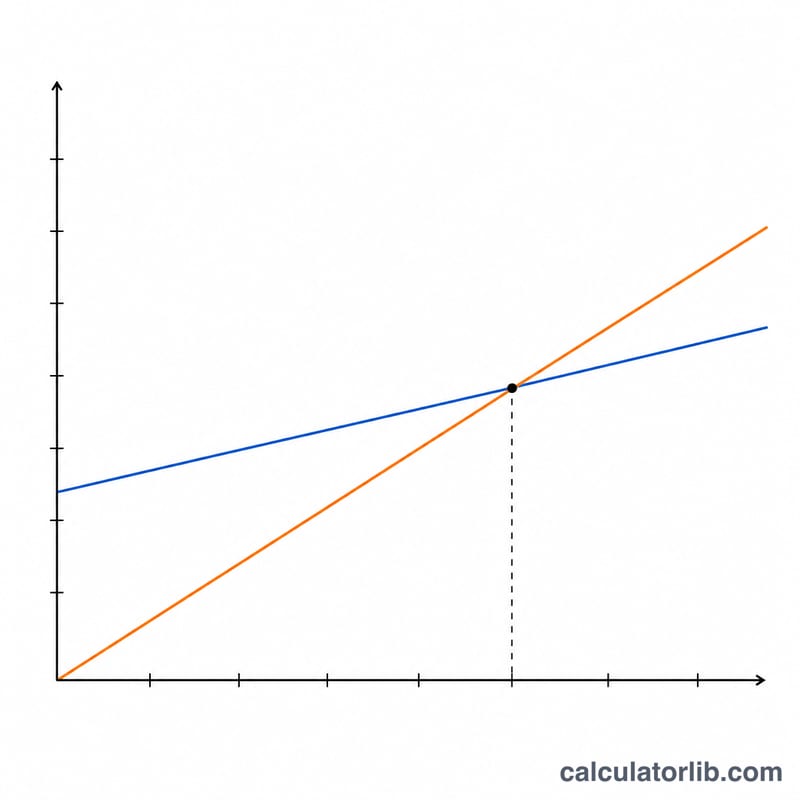

On a $300,000 loan, 1 point costs $3,000. At 7% over 30 years the payment is about $1,995.91; at 6.75% it drops to about $1,945.79 — a saving of $50.13 per month. Break-even \(= \$3{,}000 \div \$50.13 \approx 59.9\) months, roughly 5 years. If you keep the loan longer than that, the points pay off.

FAQ

Are points always worth it? Only if you keep the mortgage past the break-even point. Sell or refinance sooner and you lose money.

Is one point always 0.25% off? No — the rate reduction per point varies by lender and market conditions.

Are points tax-deductible? In the US, points on a primary-home purchase are often deductible; consult a tax professional.