What Are Mortgage Discount Points?

Discount points are an upfront fee you pay your lender to lower your mortgage interest rate. One point equals 1% of the loan amount and typically buys a rate reduction of around 0.25%. Paying points lowers your monthly payment, but it only makes financial sense if you keep the loan long enough to recover the upfront cost. This calculator (figures shown in US dollars; conventions follow common US lending practice) tells you exactly when that happens.

How to Use This Calculator

Enter your loan amount, the number of discount points purchased, the interest rate without points, the lower rate with points, and the loan term in years. The tool computes the cost of the points, both monthly payments, your monthly savings, and the number of months needed to break even.

The Formula Explained

The cost of points is \(\text{loan} \times (\text{points} \div 100)\). Each monthly payment uses the standard amortization formula

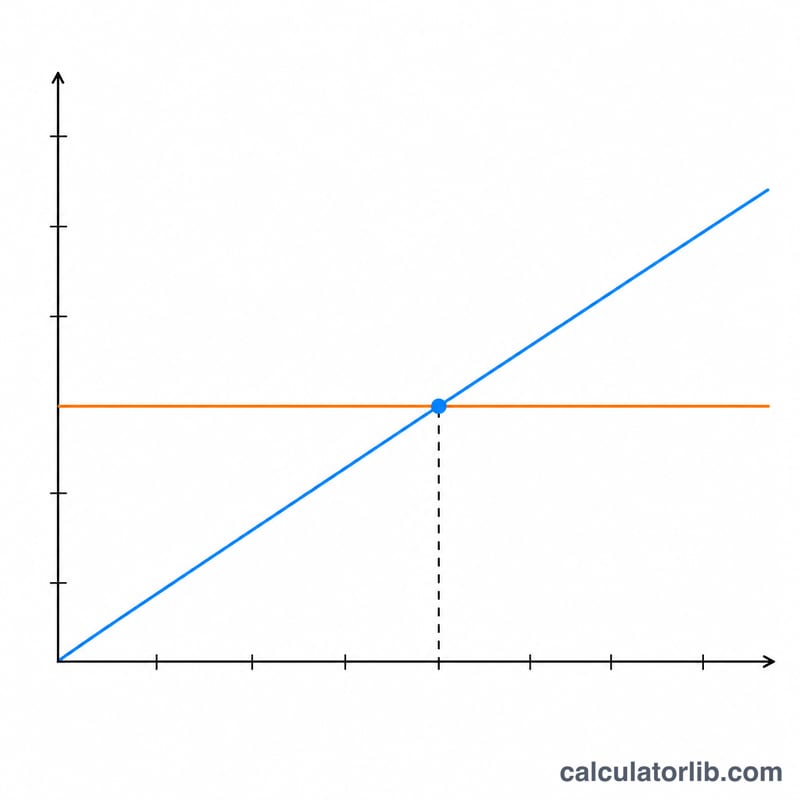

$$M = P \cdot \frac{r(1+r)^{n}}{(1+r)^{n} - 1}$$where \(r\) is the monthly rate and \(n\) is the number of months. The break-even point is simply the points cost divided by the monthly savings between the two payments.

Worked Example

On a $300,000, 30-year loan, paying 1 point ($3,000) drops the rate from 6.5% to 6.25%. The payment without points is about $1,896.20; with points it is about $1,847.15 — a monthly savings of roughly $49.05. Dividing $3,000 by $49.05 gives about

$$\frac{\$3{,}000}{\$49.05} \approx 61 \text{ months}$$or just over 5 years, to break even.

FAQ

Should I buy points? If you plan to keep the loan well beyond the break-even point, points usually save you money. If you may sell or refinance sooner, they likely won't pay off.

Is one point always 0.25%? No — the rate reduction per point varies by lender and market conditions. Always use your actual quoted rates.

Are points tax-deductible? In the US, points on a primary residence may be deductible; this calculator ignores tax effects, which would shorten the effective break-even period.