What Is the Loan Total Interest Calculator?

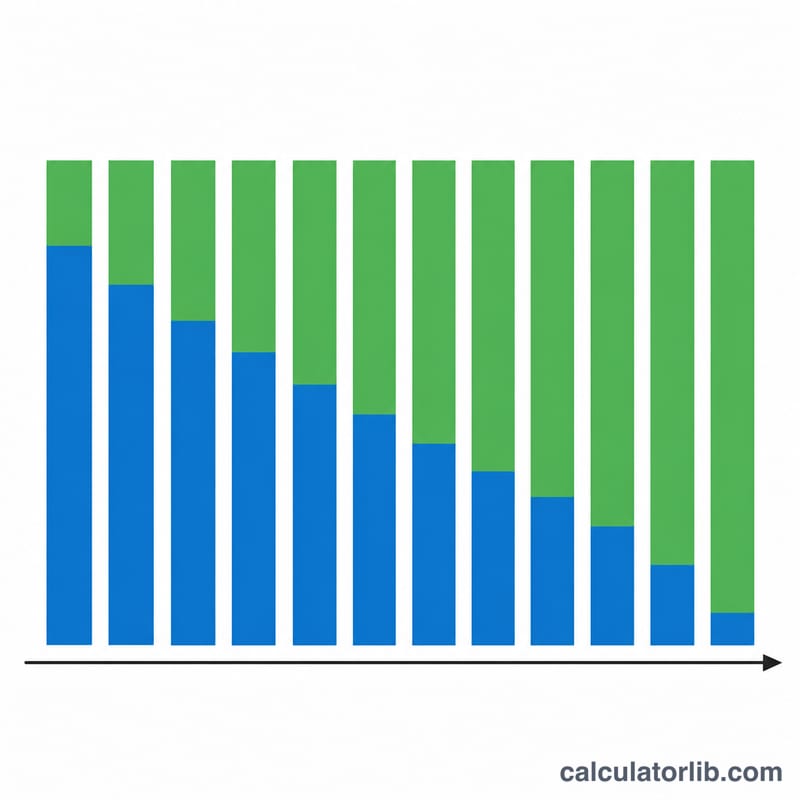

This calculator tells you how much interest you will pay over the entire life of a standard amortizing loan — such as a mortgage, auto loan, or personal loan. For an amortized loan you make equal periodic payments; early payments are mostly interest while later payments are mostly principal. The total interest is simply everything you pay minus the amount you originally borrowed.

How to Use It

Enter three values: the loan amount (principal), the annual interest rate as a percentage, and the loan term in years. The calculator converts the annual rate to a monthly rate and the term to a number of monthly payments, computes the fixed monthly payment, and then derives the total interest. Results include the monthly payment, the total of all payments, and the number of payments.

The Formula Explained

The fixed monthly payment is given by $$\text{PMT} = \frac{\text{PV} \cdot r}{1 - (1+r)^{-n}}$$ where PV is the principal, \(r\) is the monthly interest rate (annual rate ÷ 12 ÷ 100), and \(n\) is the number of months (years × 12). Multiplying the payment by \(n\) gives the total amount repaid; subtracting the original principal leaves the total interest: $$\text{Total Interest} = \text{PMT} \cdot n - \text{PV}$$ When the rate is 0%, the payment is simply \(\text{PV} \div n\) and total interest is zero.

Worked Example

Borrow $200,000 at 6% annual interest for 30 years. The monthly rate is \(r = 0.06/12 = 0.005\) and \(n = 360\). $$\text{PMT} = \frac{200000 \times 0.005}{1 - 1.005^{-360}} \approx \$1{,}199.10$$ Total paid ≈ $431,676 and total interest ≈ $231,676 — more than the original loan amount.

Key Terms & Variables

- Principal (PV)

- The loan amount — the original sum borrowed, before any interest. Denoted \(P\) in the formula above.

- Nominal annual rate

- The stated yearly interest rate on the loan (the "Rate (%)" you enter), not adjusted for compounding frequency or fees.

- Monthly rate (r)

- The nominal annual rate converted to a per-month figure: \(r = \dfrac{\text{Rate}\,(\%)}{1200}\). The 1200 divides by 100 (to a decimal) and by 12 (months per year).

- Number of payments (n)

- The total count of monthly payments over the life of the loan, \(n = 12 \times \text{Term (yr)}\). A 30-year loan has \(n = 360\).

- Monthly payment (PMT / M)

- The fixed amount paid each month, computed as \(M = P \cdot \dfrac{r}{1-(1+r)^{-n}}\). It covers both interest and principal so the loan is fully paid off at the end of the term.

- Amortization

- The process of repaying a loan through scheduled, equal payments where the interest portion declines and the principal portion grows over time, reducing the balance to zero by the final payment.

- Total of payments

- The sum of every monthly payment over the full term, \(M \times n\) — the grand total of cash paid to the lender.

- Total interest

- The cost of borrowing: the total of payments minus the principal, \((M \cdot n) - P\). This is the headline figure this calculator produces.

FAQ

Does this include taxes, insurance, or fees? No. It models pure principal-and-interest amortization only.

What if I make extra payments? Extra payments reduce both the term and total interest; this calculator assumes the scheduled payment is made each month with no prepayment.

Is the rate monthly or annual? Enter the annual nominal rate; the tool converts it to a monthly compounding rate automatically.