What Is an Interest-Only Loan?

An interest-only loan is a loan on which, for a set period, you pay only the interest that accrues each month and none of the principal. Because you are not reducing the outstanding balance, your monthly payment is lower than it would be on a fully amortizing loan — but the principal remains due in full at the end of the interest-only term. These loans are common with certain mortgages, construction financing, and bridge loans.

How to Use This Calculator

Enter your loan amount (the principal) and the annual interest rate as a percentage. The calculator instantly shows your monthly interest-only payment plus the total interest you would pay over a full year. There is no principal repayment included, so the balance never drops while you make only these payments.

The Formula Explained

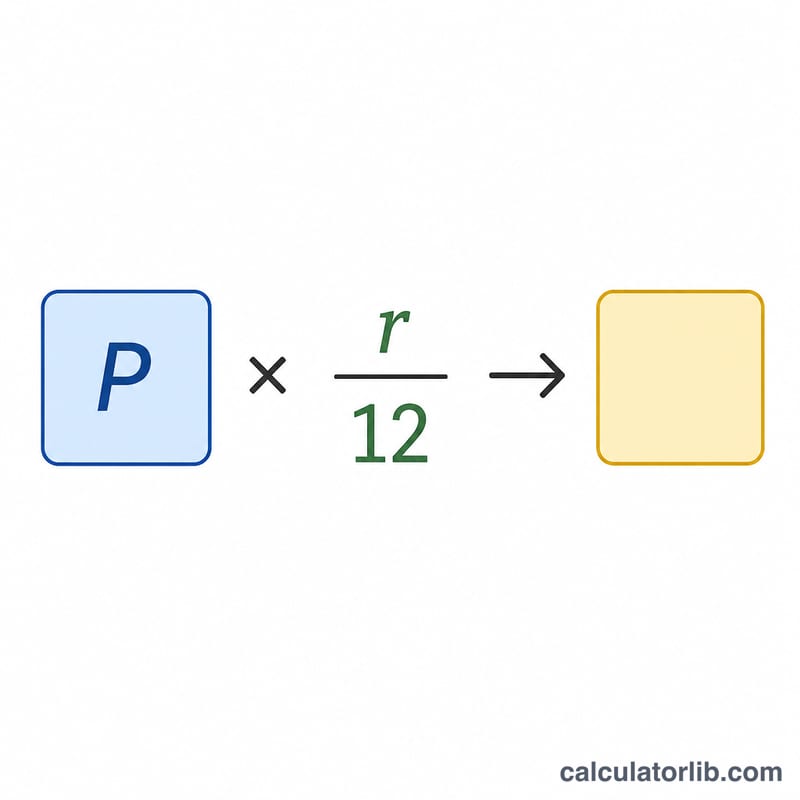

The monthly interest-only payment is the principal multiplied by the monthly interest rate. The monthly rate is the annual rate divided by 12. In symbols: $$\text{Payment} = \text{Principal} \times \left( \text{annualRate} \div 12 \right)$$, where annualRate is expressed as a decimal (e.g. \(6\% = 0.06\)). Multiplying the monthly payment by 12 gives the yearly interest cost.

Worked Example

Suppose you borrow $200,000 at a 6% annual interest rate. The monthly rate is \(0.06 \div 12 = 0.005\). Your monthly interest-only payment is $$200{,}000 \times 0.005 = \$1{,}000$$ Over a year that totals \(1{,}000 \times 12 = \$12{,}000\) in interest, with the full $200,000 principal still owed.

FAQ

Does my balance go down? No. During the interest-only period the principal stays the same because none of your payment goes toward it.

What happens when the interest-only period ends? You typically must repay the principal, refinance, or begin making higher amortizing payments that include principal.

Is an interest-only loan cheaper? The monthly payment is lower, but you pay more interest overall because you never reduce the balance during the interest-only term.