What Is a Gross-Up Interest Calculator?

A gross-up interest calculator converts a tax-free (or tax-exempt) yield into its taxable-equivalent yield (TEY) — the pre-tax interest rate a fully taxable investment would have to pay to leave you with the same after-tax return. This lets you compare apples to apples between tax-free instruments (such as municipal bonds or tax-exempt savings) and ordinary taxable accounts.

How to Use It

Enter the advertised tax-free yield as a percentage, then enter your marginal tax rate — the rate that applies to your next dollar of taxable income. The calculator returns the pre-tax equivalent yield plus the "yield pickup," which is how much extra raw yield the gross-up represents.

The Formula

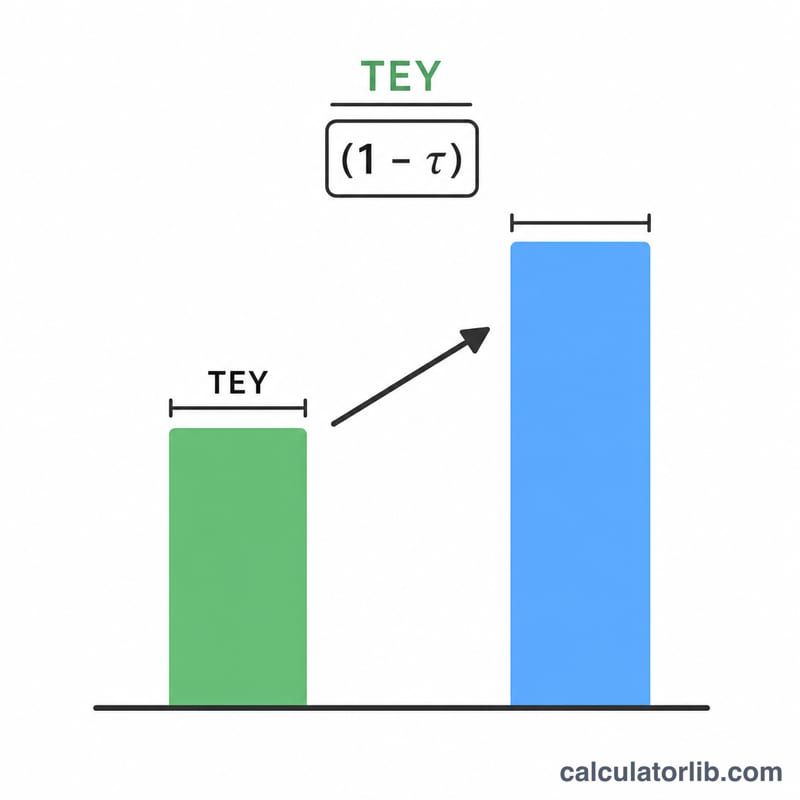

The grossed-up yield is simply the tax-free yield divided by one minus the tax rate:

$$\text{TEY} = \frac{\text{Tax-Free Yield (\%)}}{1 - \dfrac{\text{Tax Rate (\%)}}{100}}$$

Because you keep only the after-tax portion of a taxable yield, dividing by \((1 - t)\) scales the tax-free figure up to its before-tax counterpart.

Worked Example

Suppose a municipal bond offers a tax-free yield of 3.5% and your marginal tax rate is 24%. The taxable-equivalent yield is:

$$\text{TEY} = \frac{3.5\%}{1 - 0.24} = \frac{3.5\%}{0.76} = \mathbf{4.605\%}$$

So a taxable bond would need to yield about 4.61% to match the 3.5% tax-free bond. The yield pickup is \(4.605\% - 3.5\% = \) about 1.11%.

FAQ

Which tax rate should I use? Use your marginal (top-bracket) rate, since investment income is taxed at the margin. Combine federal, state and local rates if all apply.

Is a higher TEY always better? A higher TEY means the tax-free yield is more attractive relative to taxable options, especially for high earners. Compare it against the actual yields of comparable taxable investments before deciding.

Does this apply to my country? The math is universal. The concept is most common in the US (municipal bonds) but applies anywhere tax-free and taxable yields are compared. Always confirm your own jurisdiction's tax treatment.