What Is the Break-Even Quantity?

The break-even quantity (BEQ) is the number of units a business must sell so that total revenue exactly equals total cost — no profit and no loss. Every unit sold beyond this point generates profit, while selling fewer means a loss. Knowing your break-even point helps you set prices, plan production, and judge whether a product or project is financially viable.

How to Use This Calculator

Enter three numbers: your total fixed costs (rent, salaries, insurance and other costs that don't change with output), the selling price per unit, and the variable cost per unit (materials, packaging, per-unit labor). The calculator returns the break-even quantity, the revenue needed at that point, the contribution margin per unit, and the contribution margin ratio.

The Formula Explained

Break-even quantity equals fixed costs divided by the contribution margin per unit. The contribution margin is the price minus the variable cost — the amount each unit "contributes" toward covering fixed costs. Once enough units are sold to cover all fixed costs, the business breaks even.

BEQ = Fixed Costs ÷ (Price − Variable Cost)

Worked Example

Suppose fixed costs are $10,000, the price per unit is $25, and the variable cost per unit is $15. The contribution margin is $25 − $15 = $10. Break-even quantity = $10,000 ÷ $10 = 1,000 units. At $25 each, that is $25,000 in break-even revenue, and the contribution margin ratio is $10 ÷ $25 = 40%.

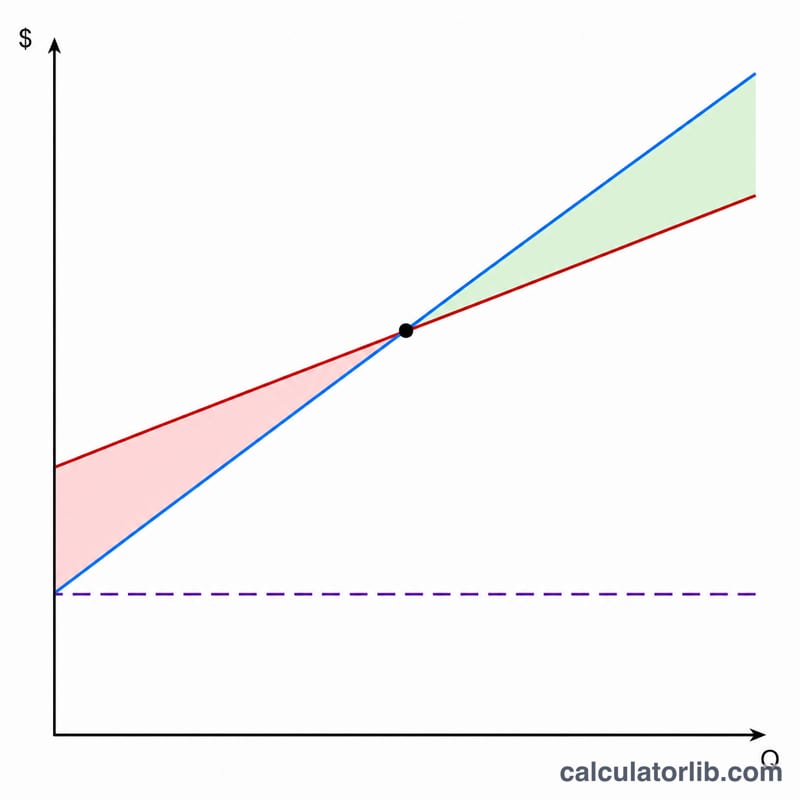

Interpreting Your Break-Even Quantity

The break-even quantity tells you the sales volume at which profit is exactly zero — every unit sold beyond that point contributes its full contribution margin to profit.

High break-even quantity. A large number of required units signals greater risk. It usually results from heavy fixed costs, a low selling price, or a high variable cost per unit (i.e. a thin contribution margin). You must capture a substantial share of the market just to avoid a loss, leaving little cushion if demand falls short.

Low break-even quantity. A small required volume means the business covers its fixed costs quickly and turns profitable sooner. This is typical of products with a wide contribution margin or low fixed overhead, giving more resilience to slow sales periods.

Margin of safety. This is the gap between your expected (or actual) sales and the break-even point, often expressed as a percentage:

$$\text{Margin of Safety} = \frac{\text{Expected Sales} - \text{Break-Even Sales}}{\text{Expected Sales}}$$If you expect to sell 2,000 units and break even at 1,334, your margin of safety is \((2000-1334)/2000 \approx 33\%\) — sales could drop by about a third before you slip into a loss. A thin margin of safety means small demand shortfalls quickly cause losses.

Contribution margin ratio. Dividing contribution margin per unit by price gives the share of each sales dollar available to cover fixed costs and profit. A ratio of 0.60 means 60 cents of every dollar goes toward fixed costs once variable costs are paid; a higher ratio lowers the break-even point and accelerates profit growth as volume rises.

Reading against realistic volume. A break-even figure is only meaningful next to attainable demand. If the result exceeds your realistic sales capacity or market size, the current price/cost structure is not viable — you would need to raise price, cut variable cost, or reduce fixed costs to bring the break-even point within reach.

Definitions & Glossary

- Fixed Costs

- Costs that do not change with the number of units produced or sold within a relevant range — for example rent, salaries, insurance, and equipment leases. They must be paid whether you sell zero units or thousands.

- Variable Costs

- Costs that rise and fall directly with output, such as raw materials, packaging, shipping, and per-unit labor or commission. Variable cost per unit is the variable cost attributable to a single unit.

- Contribution Margin per Unit

- The selling price per unit minus the variable cost per unit: \(\text{CM} = \text{Price} - \text{Variable Cost}\). It represents the amount each unit contributes toward covering fixed costs and, beyond break-even, toward profit.

- Contribution Margin Ratio

- Contribution margin per unit divided by price, expressed as a fraction or percentage: \(\text{CM Ratio} = \text{CM} / \text{Price}\). It shows the proportion of each sales dollar left after variable costs.

- Break-Even Quantity

- The number of units that must be sold for total revenue to equal total costs, leaving zero profit: \(\text{Fixed Costs} / \text{CM per Unit}\). Selling above this quantity produces a profit; selling below it produces a loss.

- Break-Even Revenue

- The sales dollars generated at the break-even quantity: break-even units multiplied by price, or equivalently \(\text{Fixed Costs} / \text{CM Ratio}\). It is the minimum revenue needed to avoid a loss.

FAQ

What if price equals variable cost? The contribution margin is zero, so you can never break even — every unit adds nothing toward fixed costs. Raise your price or cut variable costs.

Should I round up the result? Yes. Since you can't sell a fraction of a unit, round the break-even quantity up to the next whole unit to be safe.

What's the contribution margin ratio? It's the share of each sales dollar left after variable costs. A 40% ratio means 40 cents of every dollar goes toward fixed costs and profit.