What Is Future Purchasing Power?

Inflation steadily reduces what each dollar can buy. The Future Purchasing Power Calculator shows how much a sum of money today will really be worth after a chosen number of years, expressed in today's dollars. It answers the question: "If I keep $10,000 in cash, how much buying power will it have in 10 years?"

How to Use It

Enter three values: the present amount of money, the expected average annual inflation rate (as a percentage), and the number of years into the future. The calculator instantly returns the equivalent future purchasing power, the dollar amount of value lost, and the percentage of value eroded.

The Formula Explained

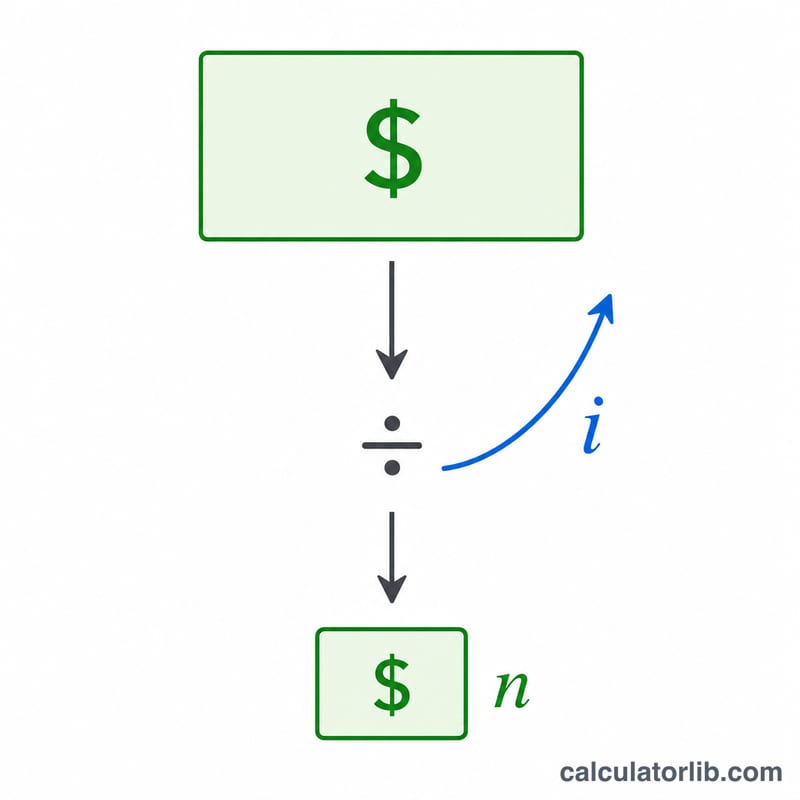

The calculation divides the present amount by a compounding inflation factor:

$$FV = \dfrac{P}{(1 + i)^{n}}$$

Here P is the present amount, i is the annual inflation rate as a decimal, and n is the number of years. Raising \((1 + i)\) to the power of \(n\) compounds inflation year over year, just as interest compounds — but in reverse, shrinking value rather than growing it.

Worked Example

Suppose you have $10,000, inflation averages 3% per year, and you wait 10 years. The inflation factor is \((1.03)^{10} \approx 1.34392\). Dividing $10,000 by 1.34392 gives about $7,440.94. That means your $10,000 will only buy what roughly $7,441 buys today — a loss of about $2,559, or 25.6% of its purchasing power.

$$FV = \dfrac{10000}{(1.03)^{10}} \approx \dfrac{10000}{1.34392} \approx 7440.94$$

FAQ

Is this the same as a present value calculation? Yes — it is a present-value discount using inflation as the discount rate, telling you the real value of future money.

What inflation rate should I use? Many people use 2–3%, near long-term historical averages, but you can model higher rates for conservative planning.

Does this account for investment growth? No. This shows pure inflation erosion on cash. If your money earns a return, compare that return to the inflation rate to find your real gain.