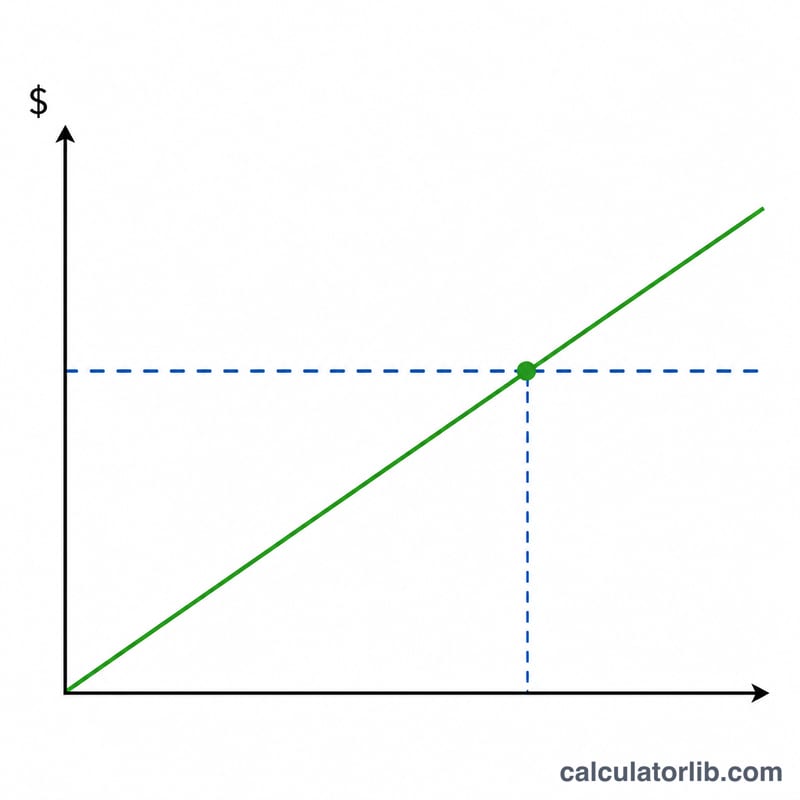

What Is a Refinance Break-Even Calculator?

When you refinance a mortgage you pay closing costs upfront, but you usually lower your monthly payment. The break-even point is the moment those monthly savings have added up to exactly cover the closing costs. After that point, every dollar of savings is money in your pocket. This calculator tells you how many months it takes to reach that point so you can decide whether a refinance makes sense for how long you plan to stay in the home.

How to Use It

Enter three numbers: your current monthly payment, your expected new monthly payment after refinancing, and the total closing costs for the new loan (lender fees, appraisal, title, points, etc.). The calculator divides the closing costs by your monthly savings to give the break-even point in months and years.

The Formula Explained

The math is simple: $$\text{Break-Even Months} = \frac{\text{Closing Costs}}{\text{Old Payment} - \text{New Payment}}$$ The denominator is your monthly savings. If your new payment is not lower than the old one, there are no savings and the refinance never breaks even on payment alone.

Worked Example

Suppose your current payment is $1,600, your new payment is $1,400, and closing costs are $4,800. Your monthly savings are \(\$1{,}600 - \$1{,}400 = \$200\). Break-even = $$\frac{\$4{,}800}{\$200} = \textbf{24 months}$$ or 2 years. If you plan to stay in the home longer than two years, refinancing likely pays off.

FAQ

Should I refinance if break-even is longer than I'll keep the home? Generally no — you'd sell or move before recouping the costs, losing money on the deal.

Does this account for the loan term resetting? No. This is a pure cash-flow break-even on payment. A longer term can lower payments while increasing total interest paid, so also compare lifetime interest.

Can I roll closing costs into the loan? Yes, but that raises your balance and payment, which lengthens the break-even period. Enter the resulting new payment to see the true effect.