What is the Break-Even Interest Rate?

The break-even interest rate — also called the taxable equivalent yield (TEY) — is the yield a fully taxable investment must earn to leave you with the same after-tax income as a tax-free investment, such as a municipal bond. Because tax-free interest escapes income tax, it can be worth more than a higher nominal taxable yield once taxes are taken out.

How to use this calculator

Enter the tax-free (municipal) yield and your marginal tax rate, both as percentages. The calculator returns the taxable yield you would need to break even. If a taxable bond yields more than this number, the taxable bond wins; if it yields less, the tax-free bond is better for you.

The formula explained

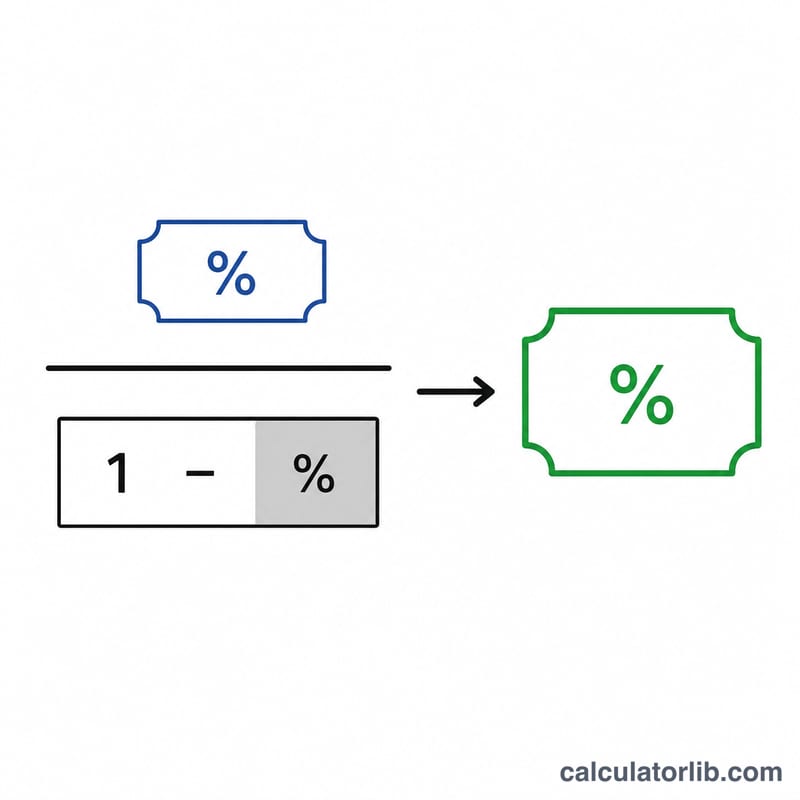

The formula is $$\text{TEY} = \frac{\text{Tax-Free Rate}}{1 - \text{Tax Rate}}$$ Dividing by (1 − tax rate) "grosses up" the tax-free yield to its pre-tax equivalent. A higher tax bracket shrinks the denominator and pushes the break-even yield higher, which makes tax-free bonds increasingly attractive.

Worked example

Suppose a municipal bond yields 4% and your marginal tax rate is 24%. Then $$\text{TEY} = 4 \div (1 - 0.24) = 4 \div 0.76 = 5.26\%.$$ A taxable bond would need to yield at least 5.26% to match the after-tax return of the 4% tax-free bond.

U.S. Federal Marginal Tax Brackets

The tax rate you enter should normally be your marginal federal ordinary-income rate — the rate applied to your next dollar of taxable income. The U.S. federal system uses seven statutory tiers. The rates themselves are fixed in law; only the dollar thresholds for each bracket adjust for inflation each year.

| Marginal Rate | Applies to |

|---|---|

| 10% | Ordinary income (lowest tier) |

| 12% | Ordinary income |

| 22% | Ordinary income |

| 24% | Ordinary income |

| 32% | Ordinary income |

| 35% | Ordinary income |

| 37% | Ordinary income (highest tier) |

These are federal ordinary-income rates only. If you also pay state income tax — and the taxable bond's interest is subject to it while the municipal bond is exempt — your effective rate for this comparison is higher than the federal figure alone. Investors near a bracket boundary should use the rate that applies to the income the bond interest would add. To confirm which bracket your income falls in, use a marginal-rate lookup.

Interpreting Your Break-Even Result

The calculator's output is the break-even taxable yield — the point at which a taxable bond and the tax-free bond leave you with the same after-tax income at your stated tax rate.

- Taxable yield above the break-even: the taxable bond delivers more after-tax income. For instance, if the break-even is 5.26% and a comparable taxable bond yields 5.75%, the taxable bond wins on a yield basis.

- Taxable yield below the break-even: the tax-free municipal bond delivers more after-tax income. A taxable bond yielding 4.90% loses to a tax-free bond when the break-even is 5.26%.

- Taxable yield equal to the break-even: the two are equivalent on an after-tax yield basis.

This comparison reflects yield only. It does not account for differences in credit quality, default risk, call features, liquidity, or maturity between the two bonds. A higher-yielding taxable bond may carry more credit or interest-rate risk than an investment-grade municipal bond, and two bonds with the same yield are not necessarily comparable investments. State and local tax treatment, the alternative minimum tax on certain private-activity municipal bonds, and the timing of taxation can also shift the real after-tax outcome away from this simple yield figure.

This is general information, not investment or tax advice. The break-even figure is a mathematical comparison of stated yields at a single tax rate and does not constitute a recommendation about any specific security.

FAQ

Which tax rate should I use? Use your marginal (top) tax rate — the rate applied to your last dollar of income — since investment income stacks on top of your other earnings.

Does this include state taxes? Not directly. For in-state munis that are also state-tax-free, you can add your state rate to your federal rate for a combined marginal rate.

What if my tax rate is 0%? At 0% the break-even equals the tax-free rate itself, since there is no tax advantage to gross up for.