What This Calculator Does

The Max Loan from DTI Ratio Calculator estimates the largest loan you could realistically afford based on your debt-to-income (DTI) ratio. Lenders use DTI to cap how much of your gross monthly income can go toward debt payments. This tool works backward from that limit to tell you the maximum principal a lender's payment cap can support.

How to Use It

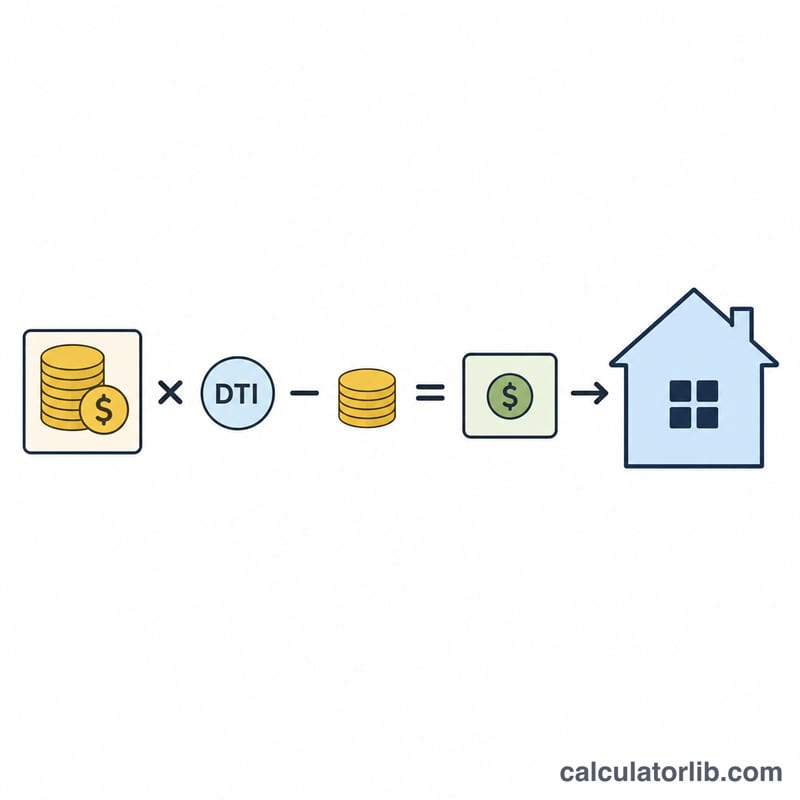

Enter your gross monthly income, the maximum DTI ratio you (or your lender) want to allow, your existing monthly debt payments (cards, auto loans, etc.), the annual interest rate, and the loan term in years. The calculator subtracts existing debts from your DTI-allowed payment to find the room left for a new loan, then converts that monthly payment into a maximum loan amount.

The Formula Explained

First we compute the payment available for the new loan: \(\text{AvailPayment} = \text{Income} \times \text{DTI} - \text{OtherDebts}\). Then we treat that payment as an ordinary annuity and find its present value: \(\text{MaxLoan} = \text{AvailPayment} \times \dfrac{1 - (1 + r)^{-n}}{r}\), where \(r\) is the monthly interest rate (annual rate \(\div 12 \div 100\)) and \(n\) is the number of monthly payments (years \(\times 12\)). When the rate is zero, MaxLoan simply equals \(\text{AvailPayment} \times n\).

$$\text{MaxLoan} = \text{AvailPayment} \cdot \frac{1-(1+r)^{-n}}{r}$$

Worked Example

Suppose your gross income is $5,000/month, your DTI limit is 36%, you already pay $500 in other debts, the interest rate is 6%, and the term is 30 years. Allowed payments = \(5{,}000 \times 0.36 = \$1{,}800\); minus $500 leaves $1,300 available. With \(r = 0.005\) and \(n = 360\),

$$\text{MaxLoan} \approx \$1{,}300 \times 166.7916 \approx \$216{,}829$$FAQ

Is this the same as a pre-approval? No. It's an estimate. Lenders consider credit score, down payment, and other factors.

What DTI should I use? Many mortgage lenders cap total DTI near 36–43%. Lower ratios leave more financial cushion.

Does it include taxes and insurance? No. For a mortgage, set aside part of your available payment for property taxes and insurance before applying this figure.