What Is the Loan-to-Value (LTV) Ratio?

The loan-to-value (LTV) ratio is a key figure lenders use to assess the risk of a mortgage or secured loan. It expresses the loan amount as a percentage of the property's value. A lower LTV means you have more equity and represent less risk to the lender, often unlocking better interest rates. A higher LTV typically means you'll need mortgage insurance (such as PMI in the US) or face stricter approval terms.

How to Use This Calculator

Enter the total loan amount you are borrowing and the appraised or purchase value of the property. The calculator instantly returns your LTV percentage, plus your home equity in money terms and as a percentage. Use the lower of the appraised value and purchase price for the most conservative, lender-accurate result.

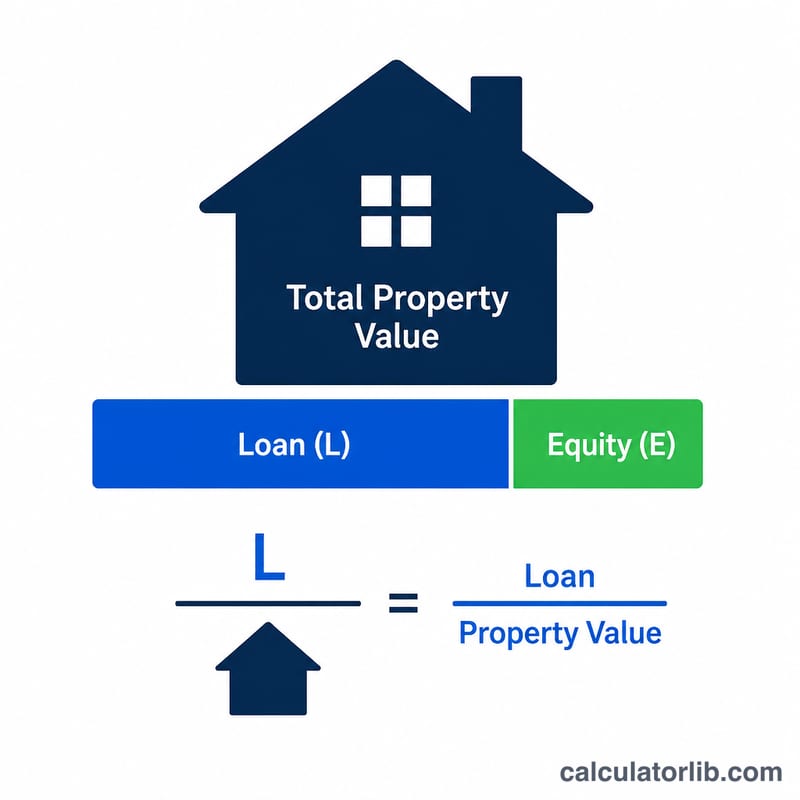

The Formula Explained

The calculation is simple: $$\text{LTV} = \frac{\text{Loan Amount}}{\text{Property Value}} \times 100\%$$. Equity is the portion of the property not covered by the loan, calculated as \(\text{Property Value} - \text{Loan Amount}\), and Equity % is \(100 - \text{LTV}\).

Worked Example

Suppose you take a $200,000 mortgage on a home valued at $250,000. Your LTV is $$200{,}000 \div 250{,}000 \times 100 = \textbf{80\%}$$ Your equity is \(\$250{,}000 - \$200{,}000 = \$50{,}000\), or 20% of the property's value. An 80% LTV is a common threshold below which many lenders waive private mortgage insurance.

FAQ

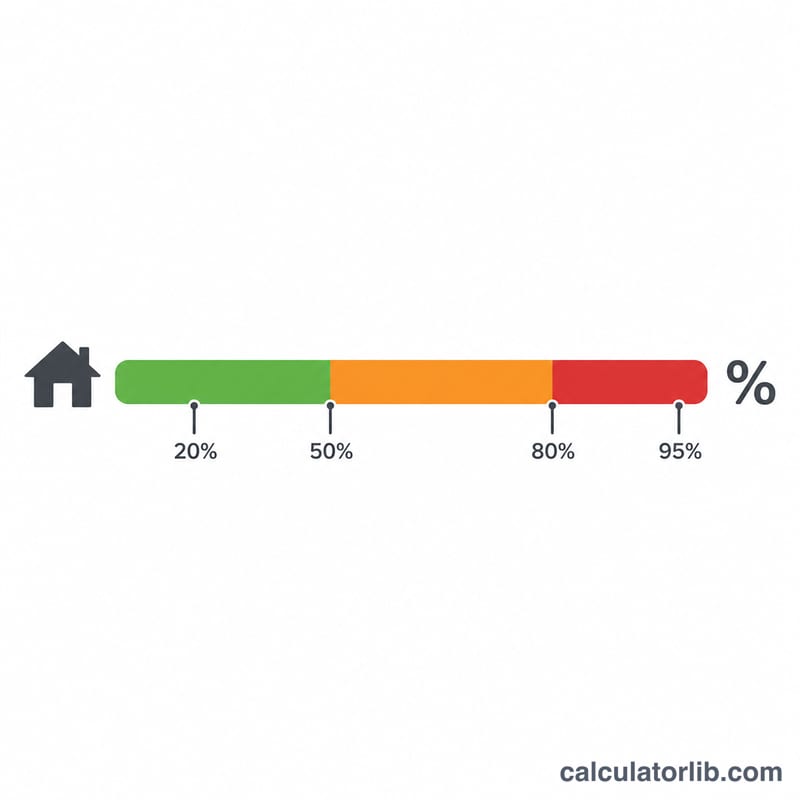

What is a good LTV ratio? An LTV of 80% or lower is generally considered favorable and may help you avoid mortgage insurance and secure lower rates.

Can my LTV change over time? Yes. As you pay down the loan or as property values rise, your LTV decreases and your equity grows.

Does a high LTV mean rejection? Not necessarily, but high-LTV loans (90%+) often carry higher rates and may require additional insurance or a larger down payment.