What is the real (inflation-adjusted) return?

The real return measures how much your investment actually grows in purchasing power after stripping out the effect of inflation. A 7% nominal gain feels great, but if prices rose 3% during the same period, you are not 7% richer — you can only buy a little more than 3.8% extra stuff. This calculator turns a headline (nominal) return into the figure that really matters for your wealth.

How to use it

Enter your nominal return (the raw percentage your investment earned) and the inflation rate over the same period. Click calculate to see your exact real return from the Fisher equation, plus the common quick approximation for comparison.

The formula explained

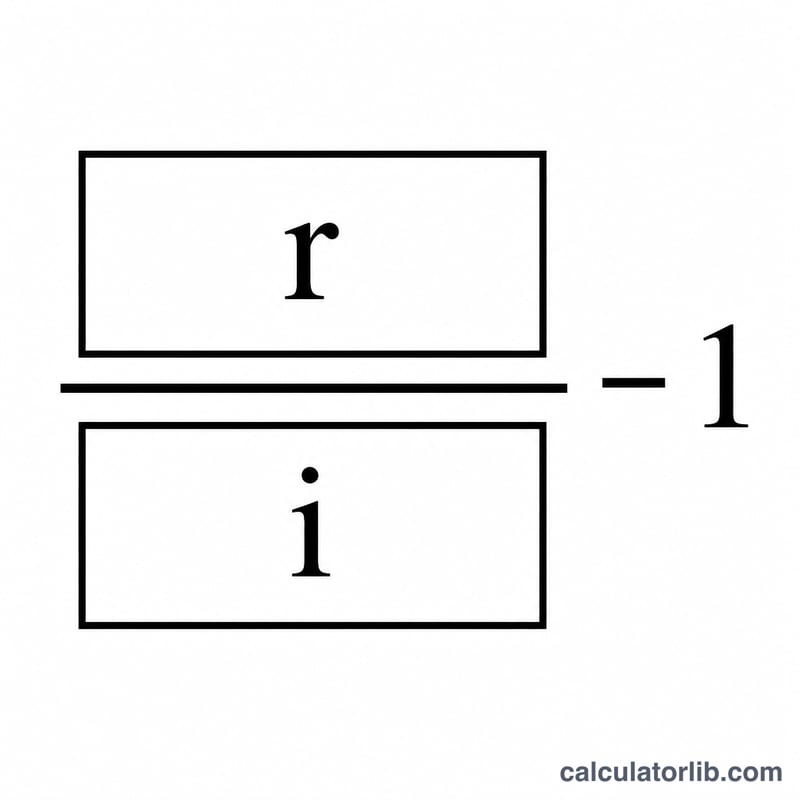

The precise relationship is the Fisher equation:

$$\text{Real Return} = \left(\frac{1 + \dfrac{\text{Nominal (\%)}}{100}}{1 + \dfrac{\text{Inflation (\%)}}{100}} - 1\right) \times 100$$

Working in decimals, divide one plus the nominal rate by one plus the inflation rate, then subtract one. Many people use the shortcut \(\text{real} \approx \text{nominal} - \text{inflation}\), which is close enough for small rates but overstates the true real return as rates climb.

Worked example

Suppose your portfolio returned 7% while inflation ran at 3%. The exact real return is $$\left(\frac{1.07}{1.03}\right) - 1 = 0.038835$$ or about 3.88%. The quick approximation gives \(7 - 3 = 4\%\), slightly too high — illustrating why the exact formula is preferred.

FAQ

Why isn't it just nominal minus inflation? Subtraction ignores that inflation also erodes the gains themselves. Dividing properly compounds the adjustment, giving a marginally lower, more accurate figure.

Can the real return be negative? Yes. If inflation exceeds your nominal return, your purchasing power shrinks and the real return is negative — common with cash savings during high-inflation periods.

Which inflation rate should I use? Typically the consumer price index (CPI) change over the same holding period as your investment return.