What This Calculator Does

Inflation quietly erodes the value of money over time. An income that comfortably covers your lifestyle today will buy noticeably less in 10, 20 or 30 years. This Inflation-Adjusted Retirement Income Calculator shows how much annual income you'll need in the future to maintain the exact same purchasing power you enjoy now. It is a universal financial tool and applies to any currency — simply enter amounts in your own.

How to Use It

Enter three values: the annual income you need today, your assumed average annual inflation rate (a long-run figure of 2–3% is common in many developed economies), and the number of years until — or into — your retirement. The calculator returns the equivalent income required in the future, the inflation multiplier, and the extra income needed beyond today's figure.

The Formula Explained

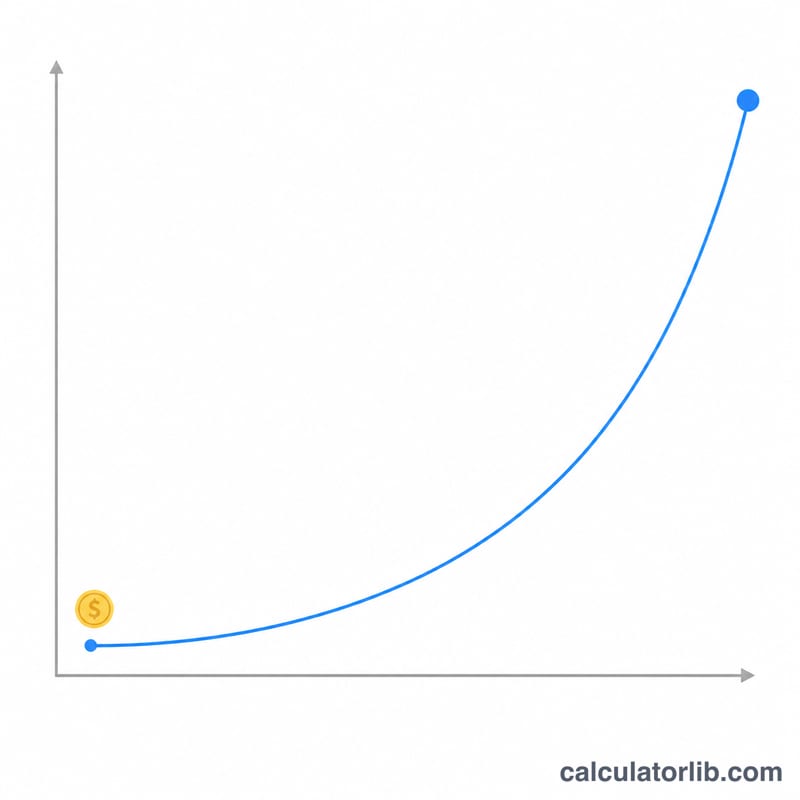

The math is compound growth applied to prices:

$$\text{Future Need} = \text{Current Income} \times (1 + i)^{n}$$

where \(i\) is the inflation rate written as a decimal (3% = 0.03) and \(n\) is the number of years. Each year prices rise by the rate \(i\), and that growth compounds on the previous year's total, just like compound interest in reverse for your buying power.

Worked Example

Suppose you need $50,000 a year today, expect 3% average inflation, and are 20 years from retirement. The multiplier is \((1.03)^{20} \approx 1.8061\). Multiplying gives $$50{,}000 \times 1.8061 \approx \textbf{90{,}306}$$ per year. That means you'll need about $40,306 more each year just to stand still — a powerful reminder to plan ahead.

FAQ

What inflation rate should I use? Many planners use 2–3% as a long-term average, but check your country's historical CPI. Higher rates dramatically increase future needs.

Does this account for investment growth? No — it only adjusts your income target for inflation. Compare this figure against your projected savings and returns separately.

Can I use it for any currency? Yes. The formula is currency-agnostic; just keep your income and results in the same currency.