What Is the Retirement Income Gap?

Your retirement income gap is the difference between the annual income you expect to need in retirement and the income you can reliably count on from sources such as a pension, Social Security, annuities, rental income or part-time work. A positive gap means you will need to draw on savings or investments to fill the shortfall; a negative gap means your guaranteed income exceeds your spending needs.

How to Use This Calculator

Enter the total annual income you expect to need in retirement, then list your expected annual income from each source: pension, Social Security, and any other income. The calculator subtracts your total expected income from the income you need and shows the yearly gap, the equivalent monthly gap, and what percentage of your needs are already covered.

The Formula Explained

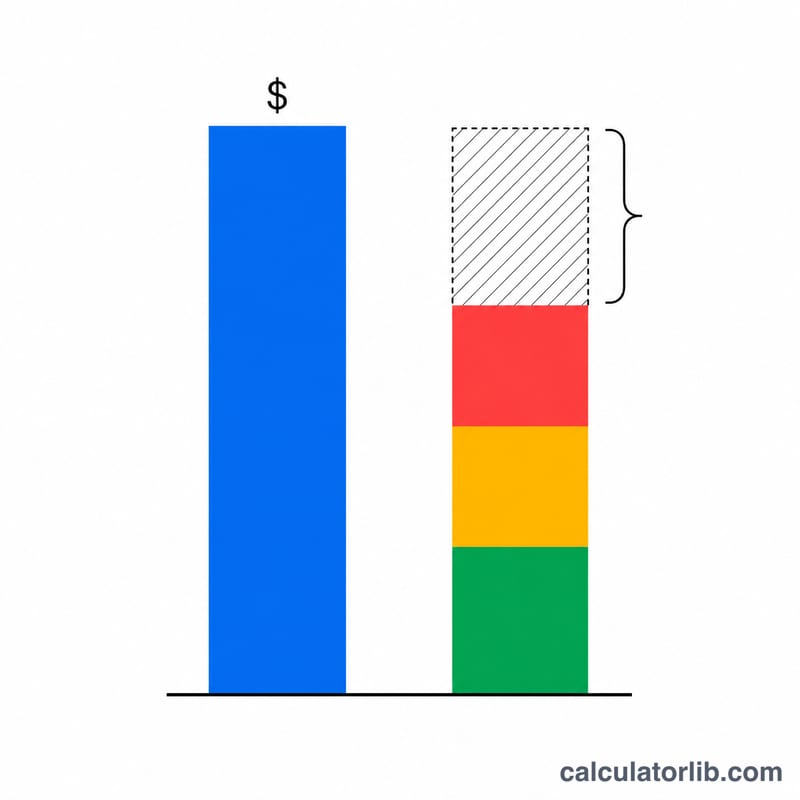

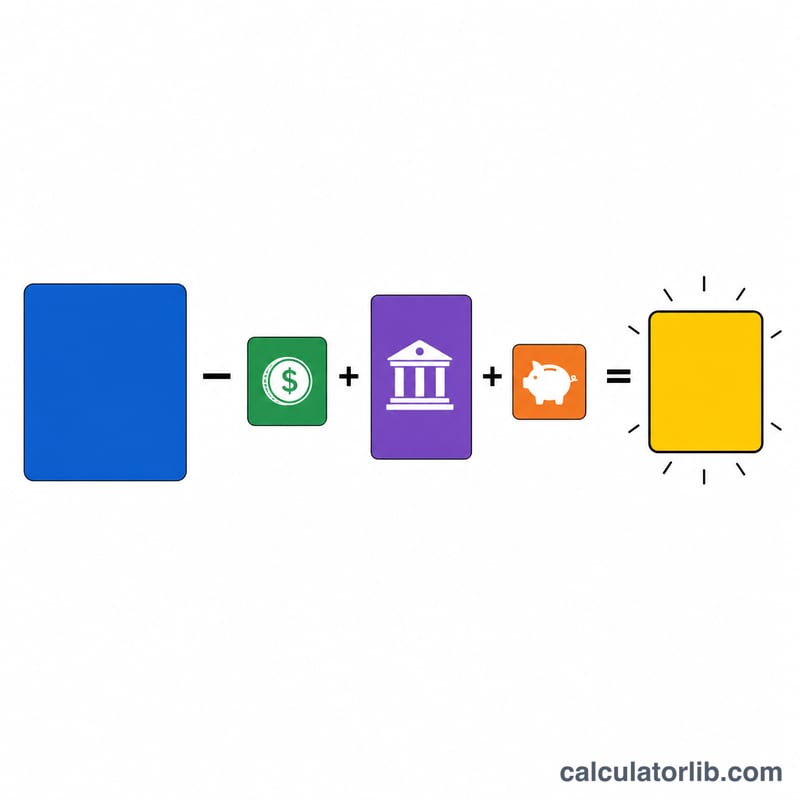

The core calculation is simple: $$\text{Gap} = \text{Needed Income} - \left( \text{Pension} + \text{Social Security} + \text{Other Income} \right)$$. The monthly gap is the annual gap divided by 12. Income coverage is the total expected income divided by the needed income, expressed as a percentage. Currency amounts shown use US dollars, but the math works for any single currency.

Worked Example

Suppose you need $60,000 per year. You expect $12,000 from a pension, $24,000 from Social Security, and $0 from other sources. Total expected income is $36,000. Your annual gap is $$\$60{,}000 - \$36{,}000 = \mathbf{\$24{,}000}$$, or $2,000 per month. Your income coverage is \(\$36{,}000 \div \$60{,}000 = 60\%\). You would need to generate $24,000 a year from savings or investments to fully fund your lifestyle.

FAQ

What if the gap is negative? A negative gap means your guaranteed income exceeds your needs — you have a surplus and may be able to save more, spend more, or retire earlier.

How much savings do I need to close the gap? A common rule of thumb is the 4% rule: multiply your annual gap by 25 to estimate the nest egg required. A $24,000 gap suggests roughly $600,000 in savings.

Should I include taxes? For accuracy, enter after-tax figures consistently, or estimate gross needs and gross income so both sides match.