What this calculator does

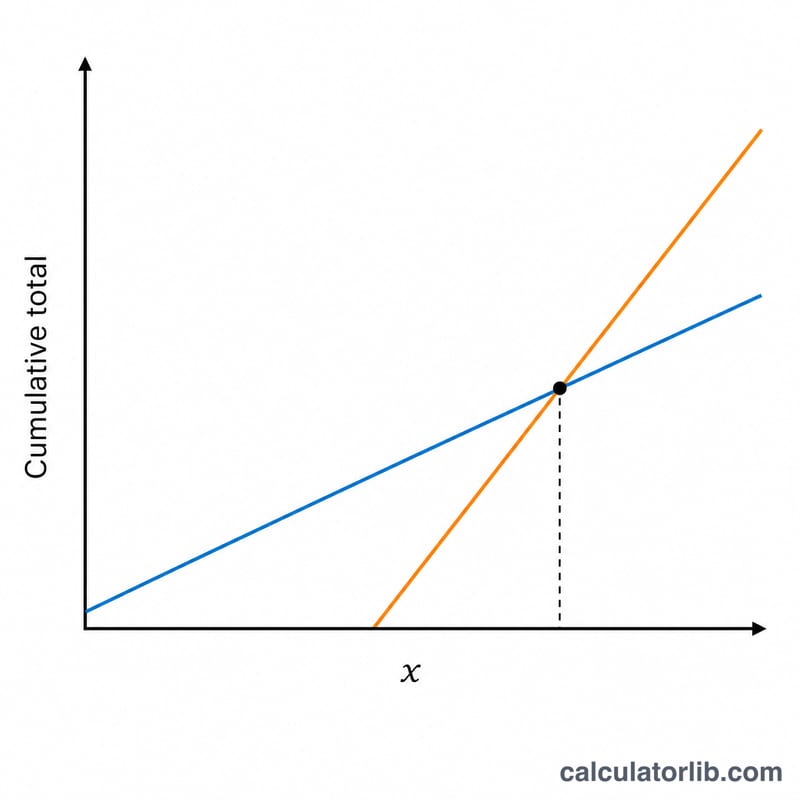

This tool applies to the United States Social Security retirement program. Choosing when to claim benefits — as early as age 62 or as late as age 70 — is one of the biggest retirement decisions you'll make. Claiming early gives you smaller checks for more months; delaying gives you larger checks but you forgo years of income. The break-even age is the age at which the total dollars received from delaying finally equal — and then surpass — the total from claiming early.

How to use it

Enter the age you would claim early (commonly 62) and the estimated monthly benefit at that age. Then enter the later claiming age (commonly your Full Retirement Age of 66–67, or 70 for maximum credits) and the higher monthly benefit. The calculator returns the break-even age plus the supporting numbers. You can pull both benefit estimates from your my Social Security account at ssa.gov.

The formula explained

The early claimer banks a "head start": the monthly early benefit multiplied by the number of months before the late claim begins. The delayed claimer earns an extra amount each month equal to the difference between the two benefits. Dividing the head-start total by that monthly difference gives the number of months past the delayed-claim age needed to catch up. Add those months to the delayed age and you have the break-even age.

$$\begin{gathered} \text{Break-Even Age} = \text{Late Age} + \frac{H}{12 \cdot D} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} H &= \text{Early Benefit} \cdot 12 \cdot \left(\text{Late Age} - \text{Early Age}\right) \\ D &= \text{Late Benefit} - \text{Early Benefit} \end{aligned} \right. \end{gathered}$$

Worked example

Suppose you'd get $1,400/month at 62 or $2,000/month at 67. The head start is \($1{,}400 \times 60 \text{ months} = $84{,}000\). The delayed benefit is $600/month higher. \($84{,}000 \div $600 = 140 \text{ months} \approx 11.67 \text{ years}\). Break-even age \(= 67 + 11.67 \approx\) 78.7 years old. If you expect to live well past 79, delaying wins.

FAQ

Does this account for COLA or taxes? No — it uses level nominal benefits and ignores cost-of-living adjustments, taxes, and investment of the early checks, so treat it as a baseline comparison.

What if the early benefit is higher? Then delaying never breaks even and the result is zero; you should re-check your inputs.

Which ages can I enter? Social Security benefits can be claimed from 62 to 70, so keep your ages within that range.