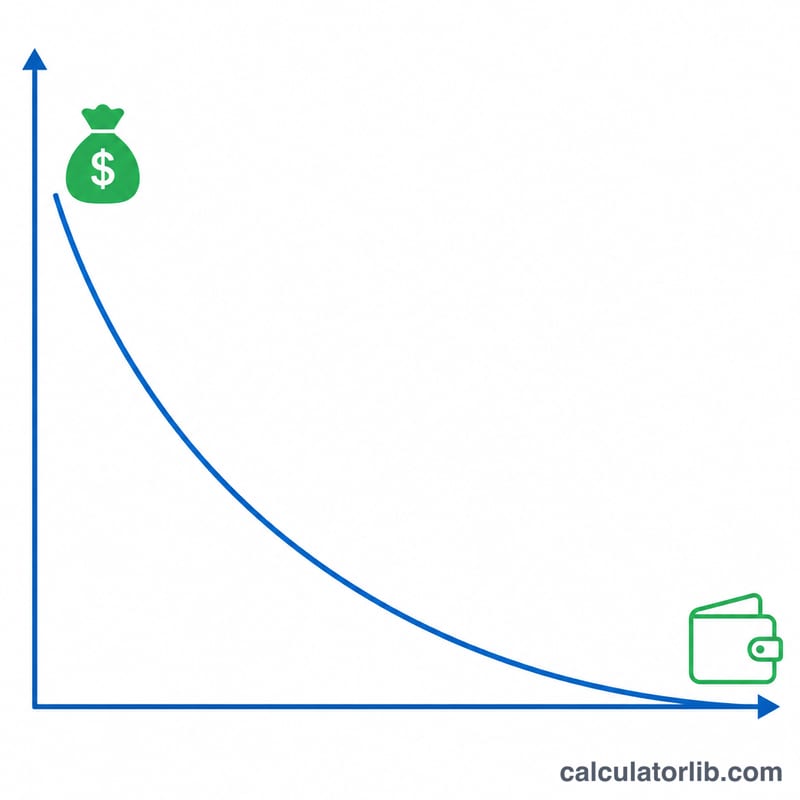

What is portfolio longevity?

Portfolio longevity is the number of years your savings can sustain a fixed annual withdrawal before the balance reaches zero. It is one of the most important questions in retirement planning: will my money outlast me? This calculator answers it using a closed-form annuity formula that accounts for both your withdrawals and the compound growth your remaining balance earns each year.

How to use it

Enter your current portfolio balance, the fixed dollar amount you plan to withdraw each year, and the average annual return you expect your investments to earn. The calculator returns the approximate number of years the portfolio will last. If your expected growth equals or exceeds your withdrawal, the result shows "Indefinite" — the portfolio is self-sustaining and never runs out.

The formula explained

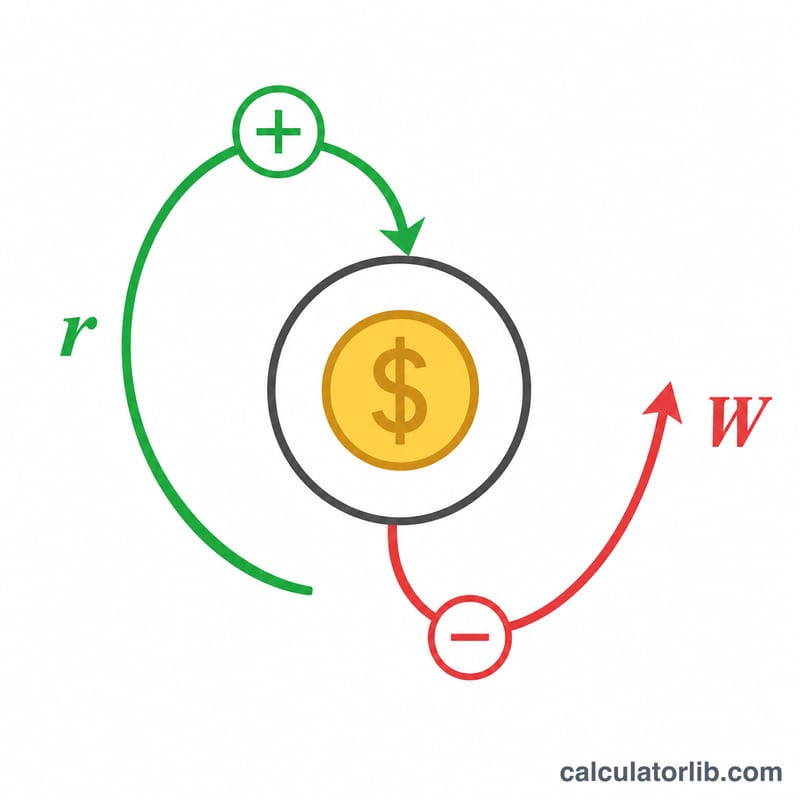

The depletion year count is $$n = \dfrac{-\ln\!\left(1 - \dfrac{P\cdot r}{W}\right)}{\ln(1+r)},$$ where \(P\) is the starting principal, \(W\) is the annual withdrawal, and \(r\) is the annual return as a decimal. The term \(P\cdot r\) is the first year's investment growth; when \(W\) is larger than this, the balance slowly erodes and the logarithm produces a finite \(n\). When \(r\) is zero, growth disappears and the formula simplifies to $$n = \dfrac{P}{W}.$$

Worked example

Suppose you have $500,000, withdraw $40,000 per year, and earn 5% annually. First-year growth is $25,000, which is less than your $40,000 withdrawal, so the balance declines. Plugging in: $$1 - \frac{500000 \times 0.05}{40000} = 1 - 0.625 = 0.375.$$ Then $$n = \frac{-\ln(0.375)}{\ln(1.05)} = \frac{0.9808}{0.04879} \approx 20.1 \text{ years}.$$

FAQ

Does this account for inflation? No — it assumes a flat dollar withdrawal. To approximate inflation, subtract your inflation rate from your expected return to use a "real" return.

What does "Indefinite" mean? Your annual investment growth covers the full withdrawal, so the principal is never touched and lasts forever in this model.

Is this guaranteed? No. Real markets are volatile and a poor sequence of early returns can deplete a portfolio faster than this smooth-return estimate suggests.