What This Calculator Does

The Retirement Savings Calculator projects how much your nest egg could grow by the time you retire. It combines two effects of compound interest: the growth of money you already have saved, and the steady growth of new contributions you add each year. The result is an estimate of your total balance at retirement, broken down so you can see how much comes from your contributions versus investment earnings.

How to Use It

Enter your current savings, the annual contribution you plan to add each year, your expected annual return rate (a long-run stock/bond mix often averages 5–8%), and the number of years until retirement. The calculator returns your projected balance plus a breakdown of principal growth, contribution growth, total contributions, and total interest earned.

The Formula Explained

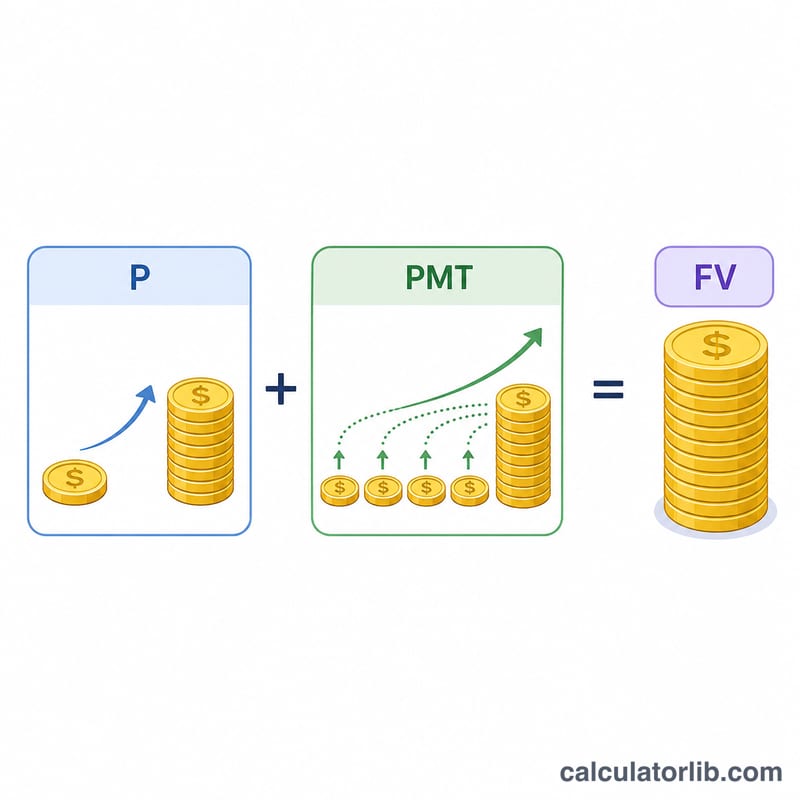

The projection uses the future-value equation:

$$FV = P(1+r)^n + PMT \cdot \frac{(1+r)^n - 1}{r}$$

Here P is your starting balance, PMT is the yearly contribution, r is the annual return as a decimal, and n is the number of years. The first term compounds your existing savings; the second is the future value of an ordinary annuity, summing the growth of each yearly deposit.

Worked Example

Suppose you start with $10,000, add $6,000 per year, earn 7% annually, and have 30 years to go. With \((1.07)^{30} \approx 7.6123\), your current savings grow to about $76,123. Your contributions grow to $$6{,}000 \times \frac{7.6123 - 1}{0.07} \approx \$566{,}765.$$ Total projected balance ≈ $642,888, of which $190,000 is contributed and roughly $452,888 is investment earnings.

FAQ

Are contributions added at the start or end of the year? This model treats contributions as end-of-year deposits (an ordinary annuity), a conservative standard assumption.

Does it account for inflation or taxes? No. Results are nominal pre-tax estimates. To gauge purchasing power, use a real (inflation-adjusted) return rate, such as 4% instead of 7%.

What return rate should I use? Returns vary, but many planners model a diversified portfolio at 5–8% long term. Lowering the rate gives a more cautious projection.