What This Calculator Does

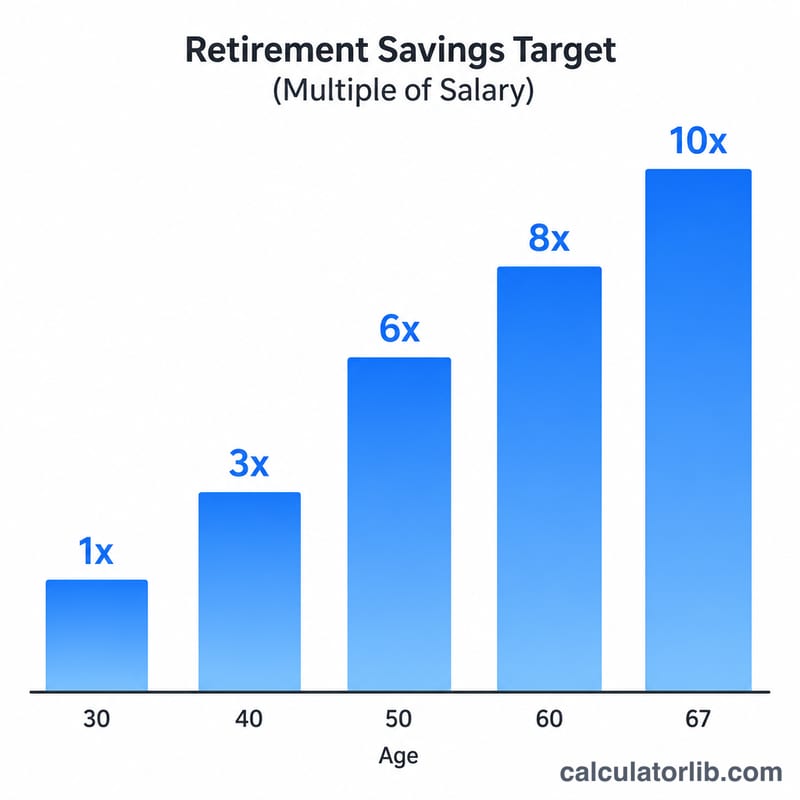

This calculator uses popular US savings benchmarks (Fidelity-style salary multiples) to estimate how much you should ideally have saved for retirement at your current age. It then compares your actual balance to that target so you can see whether you are on track. These guidelines are general rules of thumb for the United States and assume retirement around age 67; your personal needs may differ.

How to Use It

Enter your current age, your annual salary, and your total current retirement savings (401(k), IRA, and other accounts). The calculator picks the salary multiple for your age, multiplies it by your salary to get a target, and shows your surplus or shortfall plus a progress percentage.

The Formula Explained

The core formula is simply $$\text{Target} = \text{Salary} \times \text{AgeMultiple}$$ The multiples rise as you age: roughly \(1\times\) salary by 30, \(3\times\) by 40, \(6\times\) by 50, and \(8\times\) by 60. Progress is your savings divided by the target, expressed as a percentage.

Worked Example

Suppose you are 40 years old, earn $60,000, and have $100,000 saved. The multiple for age 40 is \(3\times\), so your target is $$60{,}000 \times 3 = \$180{,}000.$$ Your shortfall is $$100{,}000 - 180{,}000 = -\$80{,}000,$$ and your progress is $$100{,}000 / 180{,}000 \approx 55.6\%.$$

FAQ

Are these targets exact? No. They are widely used benchmarks, not personalized advice. Factors like expected retirement age, pensions, and spending change the right number for you.

What savings should I include? Include all retirement accounts — 401(k), 403(b), Traditional/Roth IRA, and similar — but typically not your emergency fund or home equity.

What if I'm behind? Increasing your contribution rate, capturing the full employer match, and delaying retirement can all help close a shortfall over time.