What this calculator does

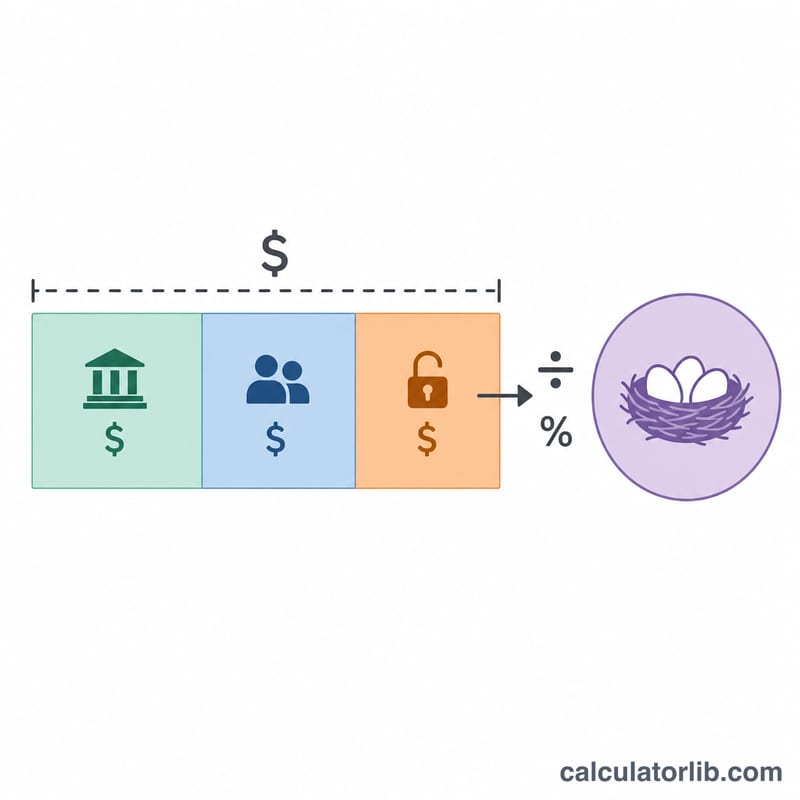

This tool is designed for US retirement planning. It estimates the total nest egg you'll need at the start of retirement to cover the gap between your desired annual spending and the income you'll already receive from a pension and Social Security. It applies the popular "4% rule" framework, where a safe withdrawal rate determines how much capital you must accumulate.

How to use it

Enter your desired annual retirement income, any expected annual pension, your expected annual Social Security benefit, and a safe withdrawal rate (commonly 3.5%–4%). The calculator subtracts guaranteed income from your target to find the income gap, then divides that gap by the withdrawal rate to give the lump sum your savings must provide.

The formula explained

First the income gap is computed as \(\text{Gap} = \text{Income} - \text{Pension} - \text{Social Security}\). If guaranteed income already covers your needs, the gap is zero. The required nest egg is then $$\text{Nest} = \frac{\text{Gap}}{\text{Rate} / 100}$$ A 4% withdrawal rate means every $1 of annual gap requires $25 of savings (\(1 \div 0.04\)).

Worked example

Suppose you want $60,000 a year, expect $20,000 from Social Security, no pension, and use a 4% rate. The gap is \(\$60{,}000 - \$20{,}000 = \$40{,}000\). Dividing by 0.04 gives a required nest egg of $1,000,000.

$$\text{Nest} = \frac{\$40{,}000}{0.04} = \$1{,}000{,}000$$FAQ

What is the 4% rule? It's a guideline suggesting you can withdraw about 4% of your initial portfolio each year, adjusted for inflation, with a low risk of running out over 30 years.

Should I use a lower rate? Many planners now favor 3.0%–3.5% for longer retirements or conservative assumptions, which increases the required nest egg.

Does this account for inflation or taxes? No. It's a simplified estimate in today's dollars and ignores taxes; treat the result as a planning starting point, not advice.