What Is a Retirement Savings Rate?

Your retirement savings rate is the share of your gross (pre-tax) income that you set aside for the future each year — including your own contributions and, if you count them, employer matches. It is one of the single most important numbers in personal finance because how much you save matters more than market returns in the early years. This calculator is currency-neutral and works for any country: just enter amounts in your own currency.

How to Use This Calculator

Enter your gross annual income (total earnings before tax) and the annual amount you save toward retirement. The tool returns your savings rate as a percentage, plus the equivalent monthly contribution so you can sanity-check your budget.

The Formula Explained

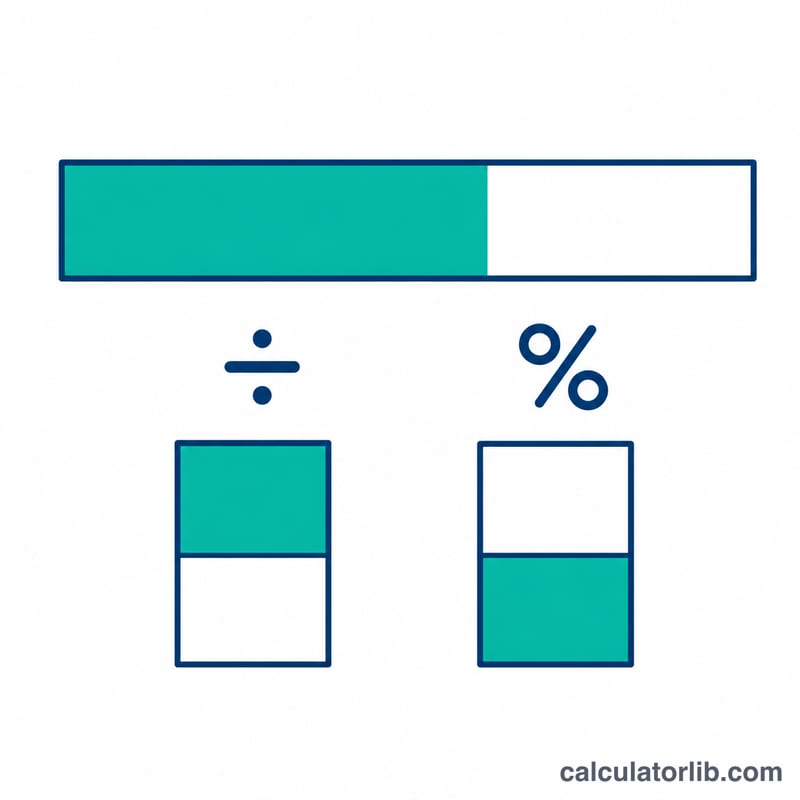

The math is simple division turned into a percentage:

$$\text{Savings Rate} = \frac{\text{Annual Savings}}{\text{Gross Annual Income}} \times 100$$

Many planners suggest a rate of 15% or more (including employer match) to stay on track for a comfortable retirement, though the right number depends on your age, target retirement date, and existing nest egg.

Worked Example

Suppose you earn 60,000 per year and save 9,000. Your savings rate is

$$9{,}000 \div 60{,}000 \times 100 = 15\%$$

That equals \(9{,}000 \div 12 = 750\) saved per month.

FAQ

Should I include employer match? Yes — including the match shows your total savings effort. To measure only your own discipline, exclude it.

Gross or net income? The conventional savings-rate figure uses gross (pre-tax) income, which is what this calculator expects.

What is a good savings rate? A common rule of thumb is 15%+, but higher rates (20–30%) can let you retire earlier or build a larger cushion.