What This Calculator Does

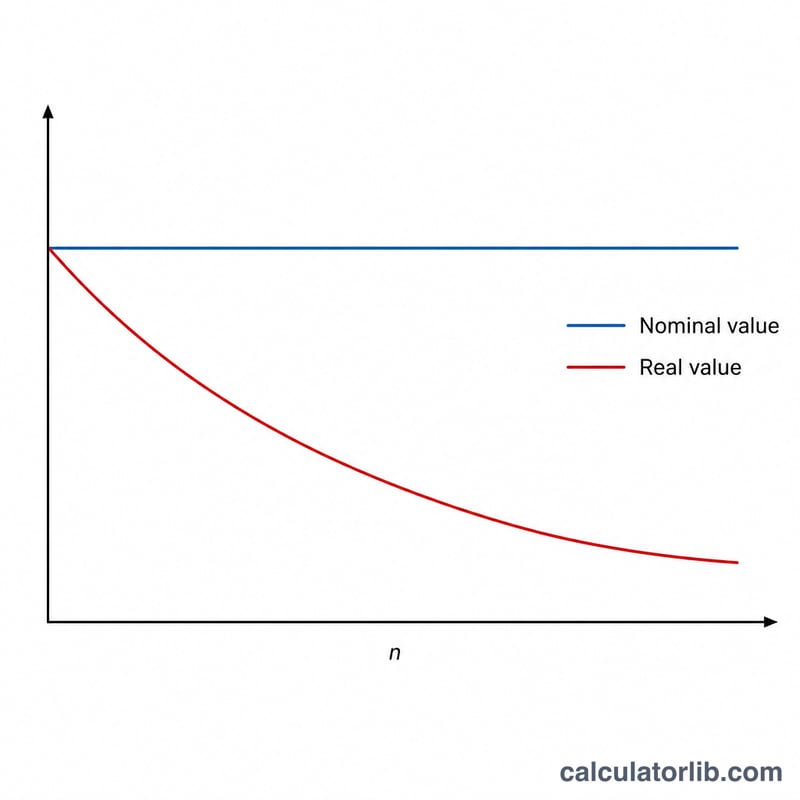

The Inflation Impact on Retirement Savings Calculator shows what a future pile of money will actually be worth in today's purchasing power. A retirement balance that looks large in 25 years may buy far less than the same figure today, because inflation steadily erodes the value of money. This tool translates a future nominal amount into its real equivalent so you can plan with realistic expectations. The math is universal and applies in any country or currency.

How to Use It

Enter three values: the future savings amount you expect to have (the nominal figure), the average annual inflation rate you want to assume, and the number of years until you reach that amount. The calculator returns the real value in today's money, the total purchasing power lost, and the percentage of value eroded.

The Formula Explained

The core equation is $$\text{Real Value} = \frac{\text{Nominal Value}}{(1 + i)^{n}}$$ where i is the annual inflation rate expressed as a decimal (3% = 0.03) and n is the number of years. The denominator \((1 + i)^{n}\) is the compound inflation factor — it grows each year, shrinking the real value. This is simply the present-value discounting formula applied to inflation instead of interest.

Worked Example

Suppose you expect to have $1,000,000 saved in 25 years, and you assume 3% average annual inflation. The inflation factor is \((1.03)^{25} \approx 2.0938\). So the real value is $$\frac{1{,}000{,}000}{2.0938} \approx \$477{,}606$$ in today's money. That means roughly $522,394 of purchasing power — about 52% — is eroded by inflation over the period.

FAQ

What inflation rate should I use? A long-run average of 2–3% is common for developed economies, but you can use a higher figure to be conservative.

Is this the same as investment returns? No. This tool isolates the effect of inflation only. Your investments may grow faster than inflation, which is why real (after-inflation) returns matter most.

Why does the percentage lost not depend on the amount? The erosion percentage depends only on the rate and number of years, so a larger balance loses the same proportion of value.