What This Calculator Does

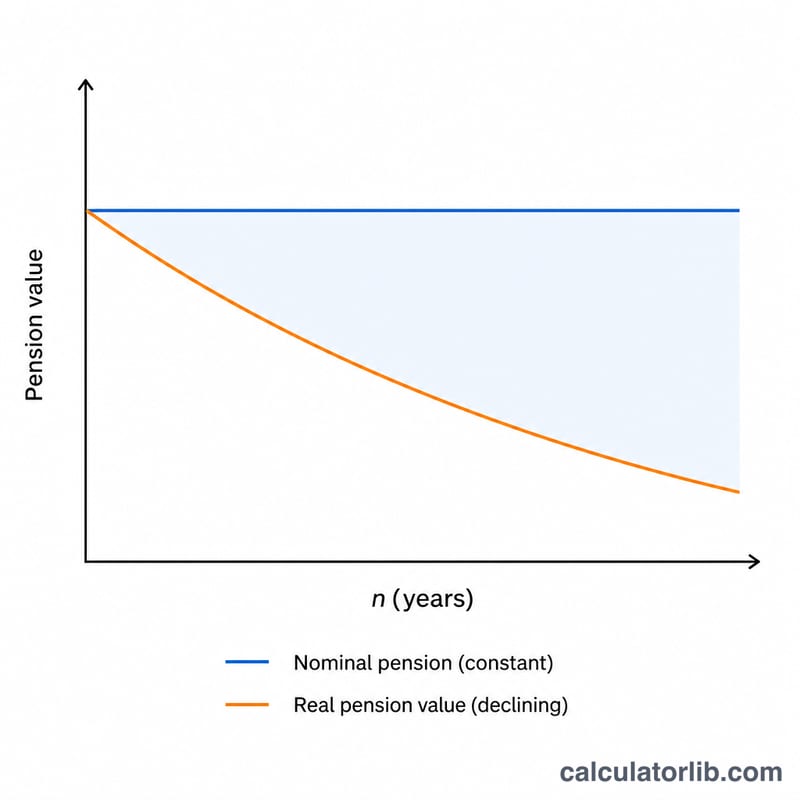

A fixed pension that pays the same amount every year slowly loses spending power as prices rise. This Inflation-Adjusted Pension Calculator converts a future nominal pension figure into its real value — what that money will actually buy in today's terms after a chosen number of years of inflation. It works with any currency, so it is useful worldwide.

How to Use It

Enter the nominal pension amount (the headline figure you expect to receive), the expected average annual inflation rate as a percentage, and the number of years into the future. The calculator returns the real, inflation-adjusted value plus how much purchasing power has been eroded.

The Formula Explained

The core equation is:

$$\text{Real Pension} = \frac{\text{Nominal Pension}}{(1 + r)^{n}}$$

where \(r\) is the annual inflation rate written as a decimal (3% = 0.03) and \(n\) is the number of years. The denominator \((1 + r)^{n}\) is the cumulative inflation factor — it grows the longer money is held and the higher inflation runs, shrinking the real value accordingly.

Worked Example

Suppose your pension pays $30,000 a year and average inflation is 3% over 20 years. The inflation factor is \((1.03)^{20} \approx 1.80611\). So the real value is $$30{,}000 \div 1.80611 \approx \$16{,}609.30$$ That means your $30,000 will buy roughly what $16,609 buys today — about 44.6% of its purchasing power has been lost.

FAQ

Is this the same as a real annuity? No. This shows the eroding value of a fixed (nominal) pension. An index-linked pension that rises with inflation would keep its real value roughly constant.

What inflation rate should I use? Many planners use a long-run average of 2–3%, but you can model higher rates to stress-test your retirement income.

Does it account for taxes or fees? No — it isolates the effect of inflation only. Apply tax and fee adjustments separately.