What Is a Balance Transfer Break-Even Calculator?

Moving a credit card balance to a card with a lower (or 0%) APR can save real money — but most issuers charge a one-time transfer fee, typically 3% to 5% of the amount moved. This calculator tells you how many months of interest savings it takes to cancel out that upfront fee. After the break-even point, every additional month is pure savings.

How to Use It

Enter the balance you plan to transfer, your current card's APR, the new card's APR (use 0 for a 0% intro offer), and the transfer fee percentage. The tool returns the break-even point in months, the dollar amount of the transfer fee, and how much interest you save each month.

The Formula Explained

First we find the one-time fee: \(\text{Fee} = \text{Balance} \times \text{Fee\%} \div 100\). Then the monthly interest saved: \(\text{Balance} \times (\text{oldAPR} - \text{newAPR}) \div 100 \div 12\). Dividing the fee by the monthly savings gives the number of months to break even. If the new APR is the same or higher, there are no savings and the transfer never pays off.

$$\begin{gathered} \text{Break-Even} = \frac{\text{Fee}}{\text{Monthly Savings}} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} \text{Fee} &= \text{Balance} \times \frac{\text{Fee \%}}{100} \\ \text{Monthly Savings} &= \text{Balance} \times \frac{\text{Old APR} - \text{New APR}}{100 \times 12} \end{aligned} \right. \end{gathered}$$

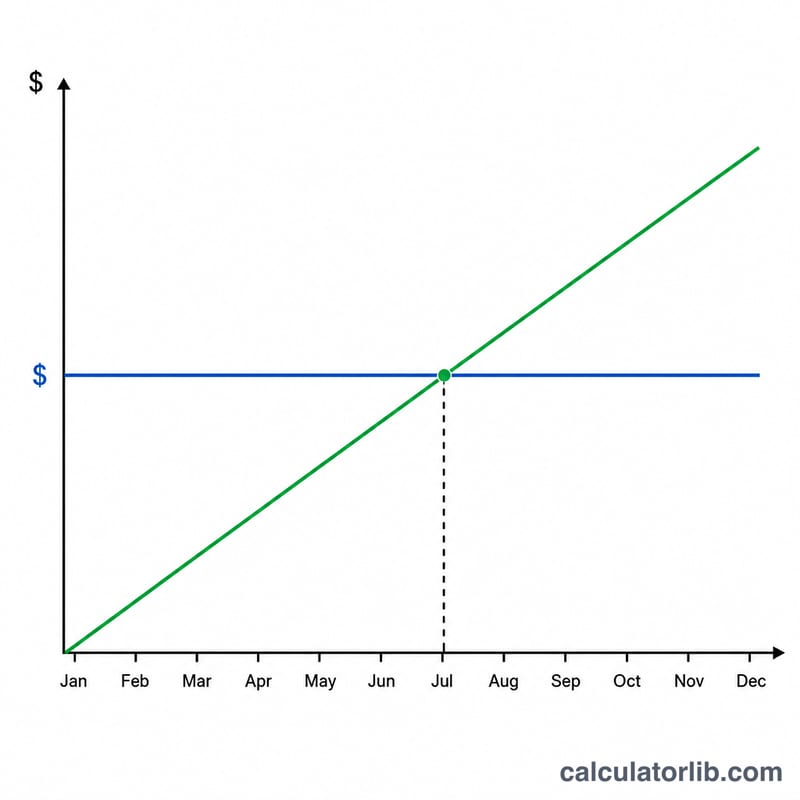

Worked Example

Suppose you transfer $5,000 from a card at 22% APR to a 0% intro card with a 3% fee. The fee is \(\$5{,}000 \times 0.03 = \$150\). Monthly interest saved is \(\$5{,}000 \times (22 - 0) \div 100 \div 12 \approx \$91.67\). Break-even:

$$\text{Break-Even} = \frac{\$150}{\$91.67} \approx 1.64 \text{ months}$$You recoup the fee in under two months, then save about $91.67 every month after.

FAQ

What if the intro APR expires? Make sure you pay off the balance before the promotional period ends, or compare the post-intro APR to your current rate.

Does this include minimum payments? No — it isolates the interest impact of the rate difference. Paying down principal speeds up real savings.

Is a transfer worth it? Generally yes if the break-even is well within the 0% promo window and you avoid new charges on the card.