What this calculator does

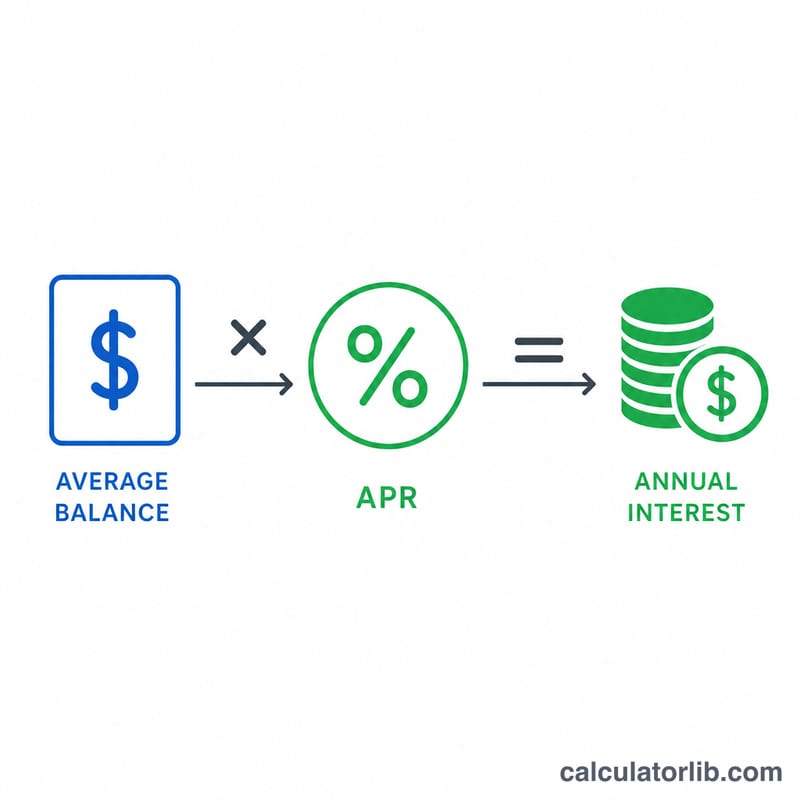

The Annual Interest Cost Calculator estimates how much interest you pay in a year for carrying a balance on a credit card or revolving line of credit. By multiplying your average outstanding balance by the annual percentage rate (APR), you get a clear dollar figure for the cost of borrowing — money that does nothing to reduce what you owe.

How to use it

Enter the average balance you typically carry over the year and your card's APR (found on your statement). The calculator returns the estimated annual interest, plus simple monthly and daily breakdowns so you can see the running cost. Use your average balance, not your highest single statement, for the most realistic yearly figure.

The formula explained

The core equation is $$\text{Annual Interest} = \text{Average Balance} \times \frac{\text{APR (\%)}}{100}$$ The APR is divided by 100 to convert the percentage into a decimal rate. Monthly interest is approximated as the annual amount divided by 12, and daily interest as the annual amount divided by 365: $$\text{Monthly} = \frac{\text{Annual Interest}}{12} \qquad \text{Daily} = \frac{\text{Annual Interest}}{365}$$ This is a straightforward, non-compounding estimate — actual card interest is usually compounded daily, so your real cost can be slightly higher.

Worked example

Suppose you carry an average balance of $3,000 on a card with a 22.5% APR. $$\text{Annual Interest} = 3{,}000 \times \frac{22.5}{100} = 3{,}000 \times 0.225 = \$675 \text{ per year}$$ That works out to roughly $56.25 per month and about $1.85 per day — all spent simply to keep the debt in place.

FAQ

Is this exact? No. It is a simple-interest estimate. Cards typically compound interest daily, so your actual cost may be a few percent higher than shown.

What balance should I enter? Use your average daily or monthly balance over the year, not a one-off peak, for a realistic annual figure.

How can I reduce this cost? Pay more than the minimum, transfer to a lower-APR card, or pay off the balance entirely — every dollar of principal you clear reduces future interest.