What This Calculator Does

Many credit card issuers calculate the monthly minimum payment as a small percentage of your statement balance plus the interest accrued that month — and they apply a fixed dollar floor (often $25 or $35) when that amount comes out very low. This calculator reproduces that common method so you can estimate what you might owe before your statement arrives.

How to Use It

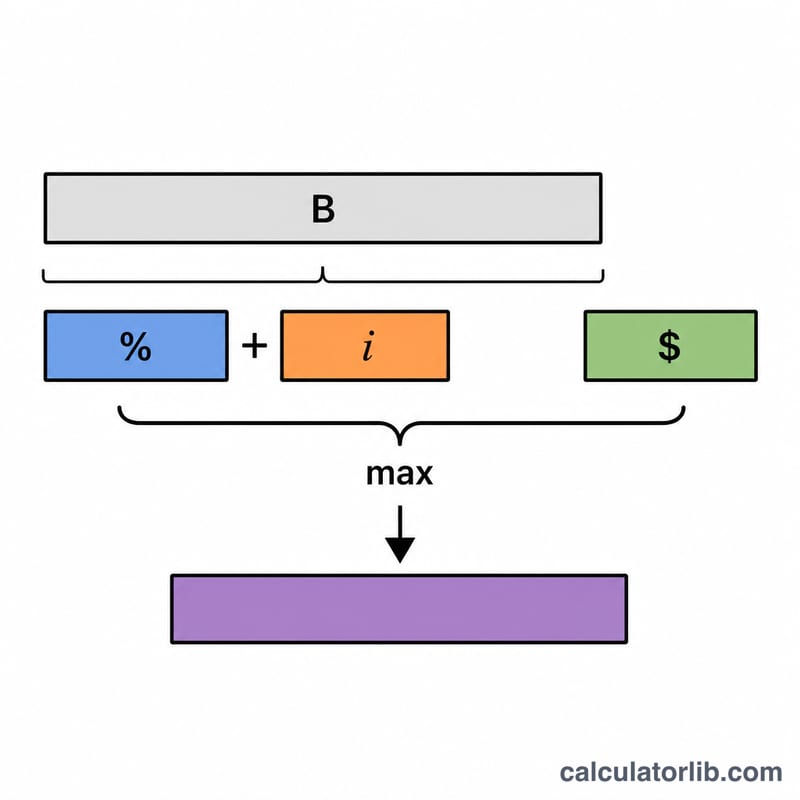

Enter your current balance, the minimum payment percentage your card uses (often around 1%–3%), your card's APR, and the minimum dollar floor from your cardholder agreement. The calculator returns the estimated minimum payment, broken down into the principal portion, the interest portion, and which figure won — the calculated amount or the floor.

The Formula Explained

The principal portion is balance × percent ÷ 100. The interest portion is balance × (APR ÷ 100 ÷ 12), representing one month of interest. These are added together, and the result is compared against the floor with max() so you always pay at least the minimum dollar amount.

$$\text{Min Payment} = \max\left(\text{Floor},\; \text{Balance}\times\frac{\text{Percent}}{100} + \text{Balance}\times\frac{\text{APR}}{1200}\right)$$

Worked Example

Suppose your balance is $3,000, the percent is 1%, the APR is 19.99%, and the floor is $25. Principal = \(3000 \times 0.01 = \$30\). Interest = \(3000 \times (0.1999 \div 12) = \$49.975\). Total = \(\$79.975\). Since that is above the $25 floor, your estimated minimum payment is about $79.98.

FAQ

Why is paying only the minimum so expensive? Because a large share of each minimum payment goes to interest, the principal barely moves — stretching repayment over years and multiplying total interest.

Does every issuer use this formula? No. Methods vary (some use flat percentages, others percent-plus-fees). This is a widely used approximation; check your cardholder agreement for exact terms.

Should I always pay the minimum? Paying more than the minimum dramatically reduces interest and payoff time. Treat the minimum as the floor, not the goal.