What This Calculator Does

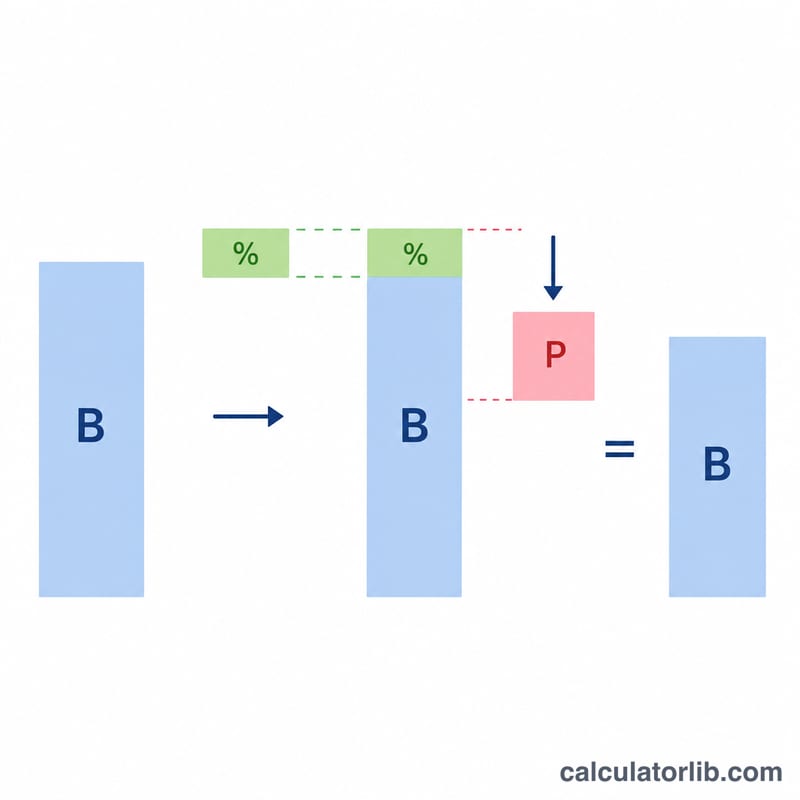

The Credit Card Balance After Payment Calculator shows how much you'll still owe after making a payment, including the interest that accrues during the billing cycle. Many people assume a $300 payment simply reduces a $2,000 balance to $1,700 — but interest is added first, so the real remaining balance is slightly higher. This tool reveals that true figure.

How to Use It

Enter your current statement balance, your card's APR (annual percentage rate), and the payment you plan to make this cycle. The calculator converts the APR to a monthly rate, applies one month of interest to your balance, then subtracts your payment to show what carries into the next cycle.

The Formula Explained

The core equation is $$\text{Remaining} = \max\!\left(0,\; \text{Balance}\left(1 + \frac{\text{APR}}{1200}\right) - \text{Payment}\right)$$ First, the monthly periodic rate is \(\text{APR} \div 12\). Multiplying your balance by this rate gives the interest for the cycle. That interest is added to your balance, and your payment is then subtracted. If your payment fully clears the balance, the result is shown as $0 (it never goes negative).

Worked Example

Suppose you owe $2,000 at a 19.99% APR and pay $300. The monthly rate is \(19.99\% \div 12 = 1.6658\%\). $$\text{Interest} = \$2{,}000 \times 0.016658 = \$33.32$$ Balance with interest = $2,033.32. After your $300 payment, you still owe $1,733.32 — about $33 more than the naive $1,700 estimate.

FAQ

Does this account for new purchases? No. It assumes no new charges during the cycle — only existing balance, interest, and your payment.

Is interest charged before or after my payment? This model adds interest to the full balance first, then applies the payment, which is the conservative (typical) approach for revolving balances without a grace period.

Why is my remaining balance higher than expected? Because interest accrues each cycle. The longer you carry a balance, the more interest compounds, which is why paying more than the minimum saves money.