What Is Credit Utilization?

Credit utilization is the percentage of your available revolving credit that you are currently using. It is one of the most influential factors in your credit score, typically accounting for roughly 30% of the calculation. Lenders view a lower utilization ratio as a sign that you manage credit responsibly. This calculator shows exactly what your utilization will be after you make a payment, so you can plan a payment that hits a target ratio.

How to Use This Calculator

Enter your current statement or card balance, the payment amount you plan to make, and your total credit limit. The tool subtracts the payment from the balance, divides the remaining balance by your credit limit, and multiplies by 100 to give your new utilization percentage. It also shows your utilization before the payment and how many percentage points you removed.

The Formula Explained

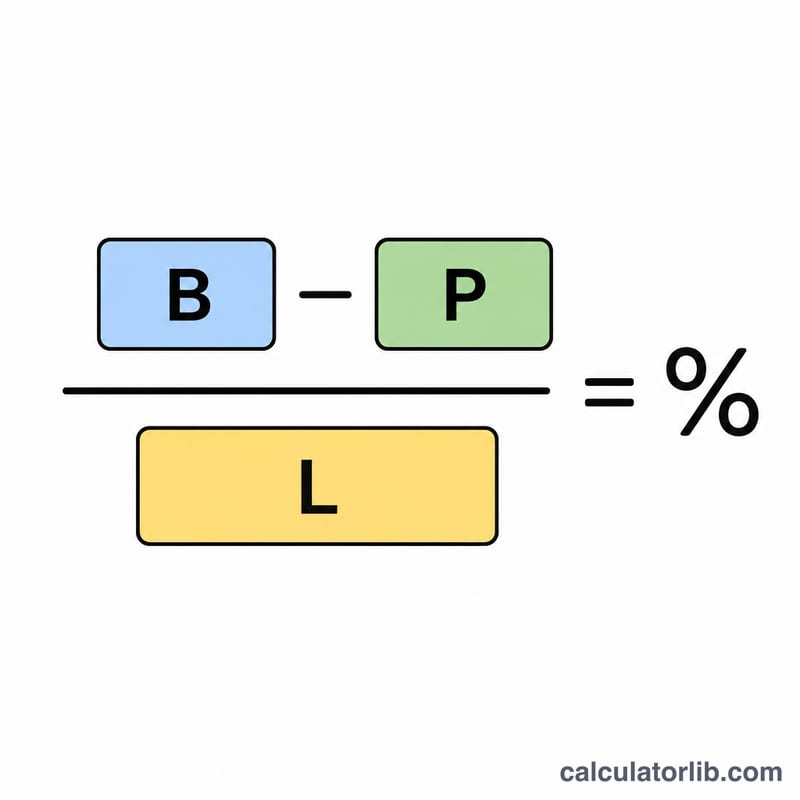

The core formula is $$\text{New Utilization \%} = \frac{\text{Balance} - \text{Payment}}{\text{Credit Limit}} \times 100$$. The numerator is your remaining balance after paying, and the credit limit is your spending ceiling. If your payment is larger than the balance, the remaining balance is treated as zero (you cannot have negative utilization on a single card).

Worked Example

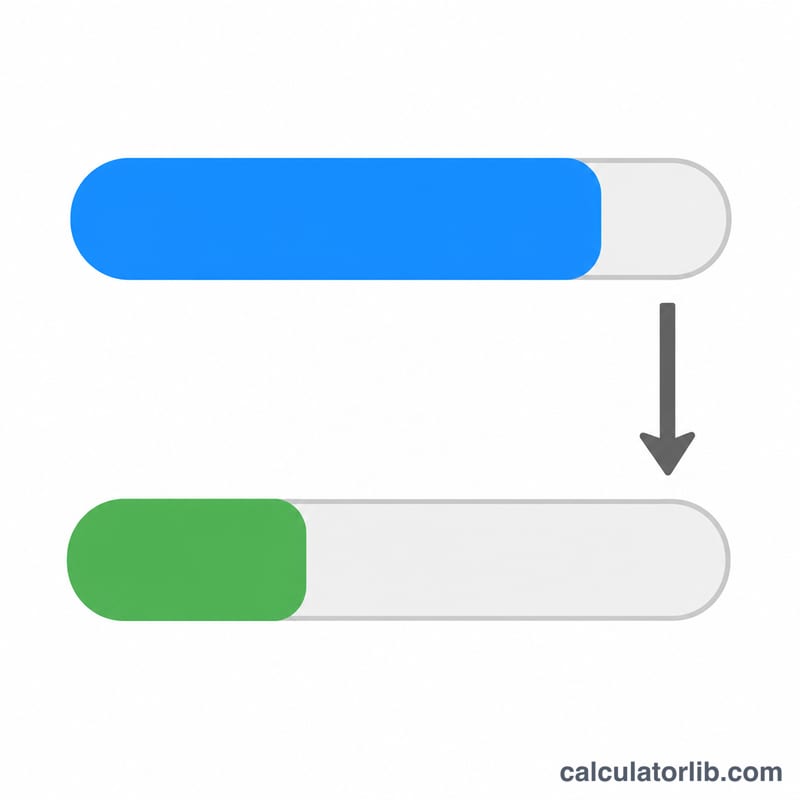

Suppose your balance is $3,000, you make a $1,000 payment, and your credit limit is $10,000. Your new balance is $$\$3{,}000 - \$1{,}000 = \$2{,}000$$. Dividing by $10,000 gives 0.20, or 20% utilization. Before the payment you were at \(\$3{,}000 \div \$10{,}000 = 30\%\), so the payment reduced your utilization by 10 percentage points.

FAQ

What utilization should I aim for? Many experts suggest keeping utilization under 30%, and below 10% for the best scoring impact.

Should I use my total limit across all cards? This calculator covers one card or limit at a time. For your overall ratio, total all balances and all limits across your revolving accounts.

Does paying before the statement date help? Yes. Card issuers usually report the balance on your statement date, so paying down before that date lowers the utilization that gets reported to the bureaus.