What this calculator does (US Army / BRS)

This tool applies to United States uniformed service members under the Blended Retirement System (BRS). It estimates how much goes into your Thrift Savings Plan (TSP) each month and year from both your own pay deferrals and your agency's matching contributions. Figures are based on monthly basic pay and the standard BRS matching schedule; it does not model the annual IRS elective deferral limit or special/incentive pay.

How to use it

Enter your monthly basic pay, the percentage of base pay you contribute, and whether to include the automatic 1% agency contribution. The calculator returns your monthly and annual deferral, the agency match, and the combined total going into your TSP.

The formula explained

Under BRS, the government adds an automatic 1% of base pay even if you contribute nothing. On top of that, it matches dollar-for-dollar on the first 3% you contribute and 50 cents on the dollar for the next 2%. So contributing 5% earns the maximum 4% match — combined with the automatic 1%, that's a total 5% agency contribution. Contributing more than 5% does not increase the match.

$$\begin{gathered} \text{Total}_{\text{monthly}} = B \cdot c + A + B \cdot m \\[1.5em] \text{where}\quad \left\{ \begin{aligned} B &= \text{Base Pay (\$)} \\ c &= \dfrac{\text{Contribution \%}}{100} \\ A &= \text{Auto 1\%} \cdot 0.01 \cdot B \\ m &= \min(c,\,0.03) + 0.5\cdot\min(\max(c-0.03,\,0),\,0.02) \end{aligned} \right. \end{gathered}$$

Worked example

Suppose your monthly base pay is $5,000 and you contribute 10% with the automatic 1% included. You defer $500/month. The agency adds 1% ($50) automatically, 3% ($150) dollar-for-dollar, and half of the next 2% ($50), for $250 total match each month — $3,000 per year. Your annual deferral is $6,000, so the total annual TSP contribution is $9,000.

$$\$5{,}000 \cdot 0.10 = \$500 \;\text{per month}$$$$\$50 + \$150 + \$50 = \$250 \;\text{match per month} = \$3{,}000 \;\text{per year}$$$$\$6{,}000 + \$3{,}000 = \$9{,}000 \;\text{total annual TSP contribution}$$

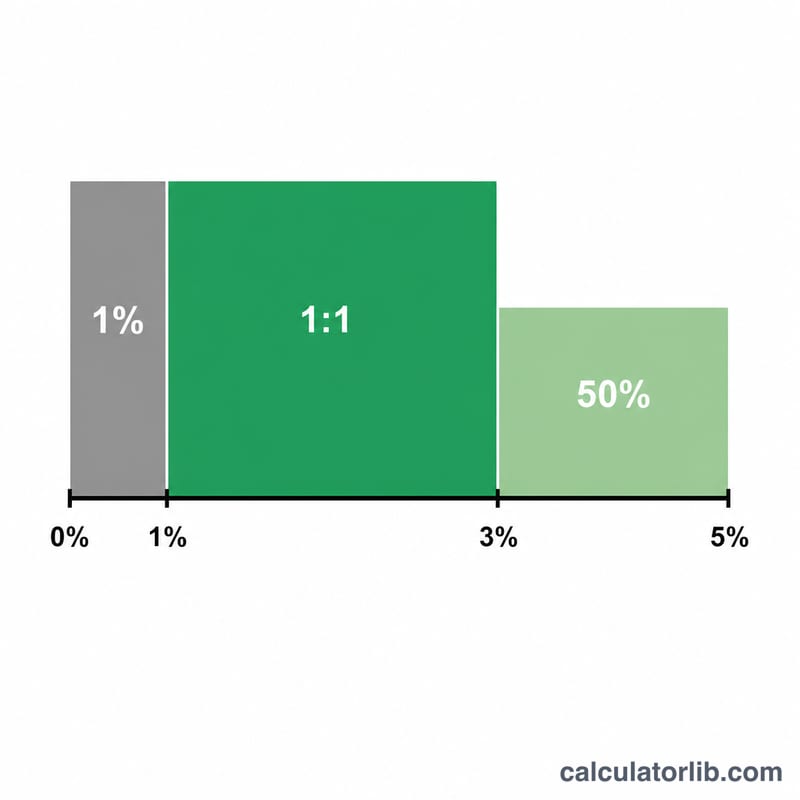

BRS Matching Schedule

Under the Blended Retirement System (BRS), the government contributes to your TSP in two ways: a flat automatic 1% of base pay (paid even if you contribute nothing) plus matching on your own contributions. The matching is dollar-for-dollar on the first 3% and 50 cents per dollar on the next 2%.

| Your contribution tier | Automatic contribution | Match on that tier | Cumulative agency contribution |

|---|---|---|---|

| 0% | 1% of base pay | None | 1% |

| 1% – 3% | 1% of base pay | Dollar-for-dollar (100%) | up to 4% |

| 3% – 5% | 1% of base pay | 50 cents per dollar (50%) | up to 5% |

| 5%+ | 1% of base pay | No additional match | 5% (maximum) |

The maximum agency contribution is 5% of base pay, reached when you contribute at least 5% yourself: 1% automatic + 3% dollar-for-dollar + 1% (half of the 3%–5% tier) = 5%.

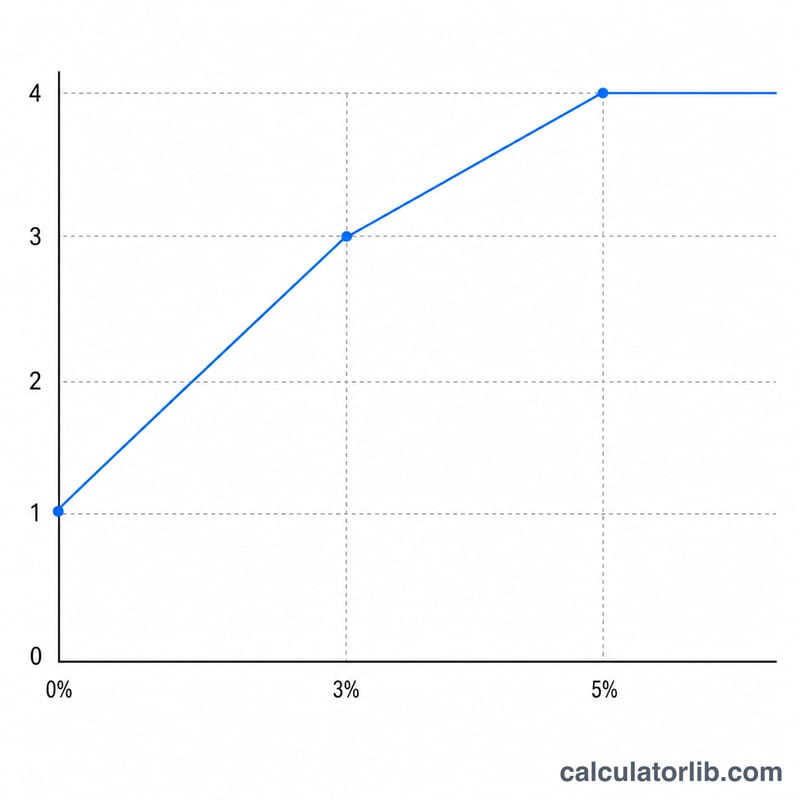

What Your Result Means

The combined monthly total shown by this calculator is the sum of three parts: your own deferral (\(B\cdot c\)), the automatic 1% (\(A\)), and the agency match (\(B\cdot m\)). The single most important threshold is 5%: contributing at least 5% of your base pay captures the full agency contribution of 5% (1% automatic plus 4% matching).

Contributing above 5% does not increase the agency match — the match plateaus at 5% of base pay. Amounts you defer beyond 5% are still your money growing in your account, but they receive no additional government contribution.

A few limitations of this estimate: it is based on monthly base pay only and does not include special pay, incentive pay, or bonus contributions, which the agency does not match the same way. It also does not apply the annual IRS elective deferral limit, which caps how much you can personally contribute across the year. Verify current limits and your eligibility with the official TSP and your finance office.

This is general informational content, not personal financial advice. For decisions about your own contributions and retirement strategy, consult a qualified financial professional or your military personal financial counselor.

FAQ

Does contributing more than 5% increase the match? No. The match caps at 5% of base pay (1% automatic + 4% matched). Extra contributions still grow your account but earn no additional match.

Is the automatic 1% always included? Under BRS, yes, after the required service waiting period. You can uncheck it here for "what-if" scenarios.

Does this include the IRS annual limit? No — this is a rate-based estimate and does not cap at the elective deferral limit.