What Is the ACB Loan Eligibility Calculator?

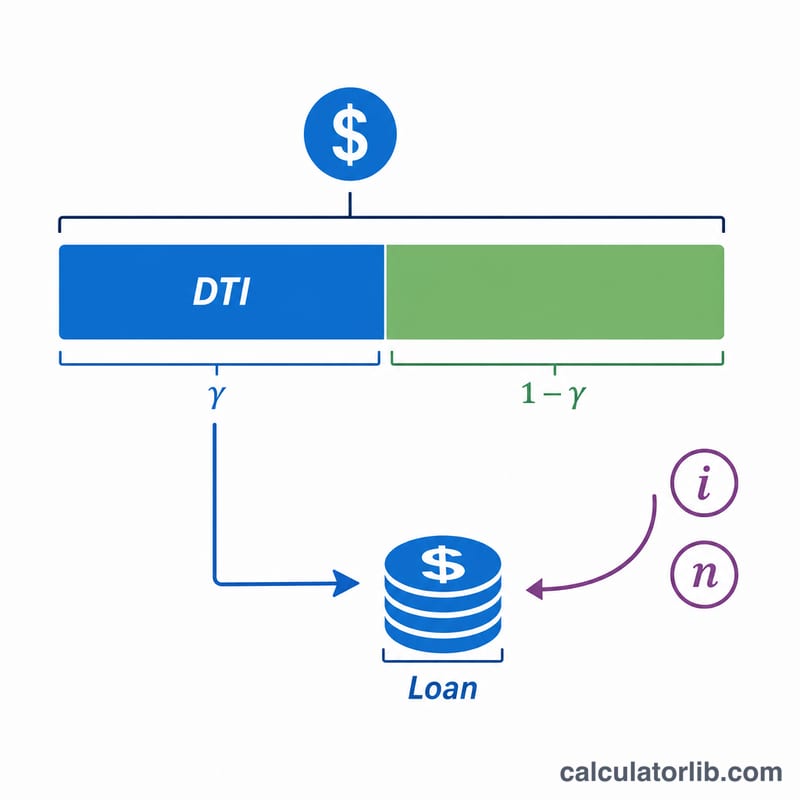

This calculator estimates the maximum loan amount you could be eligible to borrow based on your monthly income, a lender's debt-to-income (DTI) limit, the interest rate, and the loan term. It works by first determining the largest monthly payment your income can support, then converting that payment into a present-value loan amount using the standard amortization formula. The tool is currency-agnostic — enter all amounts in the same currency.

How to Use It

Enter your gross monthly income, the maximum DTI ratio your lender applies (commonly 36–43%), the annual interest rate, and the loan term in years. The result shows your maximum eligible loan, the corresponding monthly payment, total repayment over the term, and total interest.

The Formula Explained

First, the maximum monthly payment is $$\text{MaxEMI} = \text{Income} \times \text{DTI}\%$$. Then the borrowable principal is the present value of that payment stream: $$\text{MaxLoan} = \text{MaxEMI} \times \dfrac{1-(1+i)^{-n}}{i}$$, where \(i\) is the monthly interest rate (annual rate ÷ 12 ÷ 100) and \(n\) is the number of monthly payments (years × 12).

Worked Example

Suppose your monthly income is 5,000, the DTI limit is 40%, the annual rate is 7%, and the term is 20 years. $$\text{MaxEMI} = 5{,}000 \times 0.40 = 2{,}000$$ The monthly rate \(i = 0.07 \div 12 \approx 0.0058333\) and \(n = 240\). $$\text{MaxLoan} = 2{,}000 \times \frac{1-(1.0058333)^{-240}}{0.0058333} \approx 257{,}952$$ Total repayment \(= 2{,}000 \times 240 = 480{,}000\), so total interest \(\approx 222{,}048\).

Typical DTI Limits and Rate Ranges

Lenders express affordability through the debt-to-income (DTI) ratio — the share of gross monthly income consumed by debt payments. Two versions are commonly used:

- Front-end (housing) DTI: only housing costs (mortgage principal, interest, taxes, insurance). A common guideline is 28%.

- Back-end (total) DTI: all recurring debt payments (housing plus car loans, student loans, credit cards, personal loans). The traditional conventional benchmark is 36%.

This is often summarized as the 28/36 rule. Other widely referenced thresholds:

| Guideline | DTI Threshold | Context |

|---|---|---|

| Conventional comfort limit | 36% back-end | Conservative lending standard for total debt |

| Qualified Mortgage (QM) limit | 43% back-end | Long-standing U.S. ability-to-repay reference point |

| Expanded / automated underwriting | up to ~45–50% | Possible with strong credit, reserves, or compensating factors |

Typical unsecured personal loan rates generally run higher than secured mortgage or auto rates because there is no collateral. When estimating eligibility, use a DTI you are comfortable servicing rather than the maximum a lender might technically permit — staying near the 36% back-end figure leaves room for emergencies and rate changes. Always check current rate ranges with the specific lender, as pricing depends on credit profile, loan size, and term.

FAQ

What is a DTI ratio? Debt-to-income ratio is the share of your monthly income a lender allows toward loan payments. Lower DTI limits mean a smaller eligible loan.

Is the result a guaranteed approval? No. It is an estimate. Actual approval depends on credit history, existing debts, and lender policy.

Does it include existing debt? Not directly. If you already have debt payments, reduce your effective DTI input to reflect the remaining capacity.