What Is the Effective Annual Yield?

The effective annual yield (EAY), also called the annual percentage yield (APY) or effective annual rate (EAR), is the true return earned on an investment or paid on a loan once the effect of compounding is included. A stated (nominal) rate looks the same whether interest compounds once a year or daily, but more frequent compounding produces a higher actual yield. The EAY converts any nominal rate into a single comparable annual figure.

How to Use This Calculator

Enter the nominal annual interest rate as a percentage and the number of times interest compounds per year — 1 for annual, 2 for semi-annual, 4 for quarterly, 12 for monthly, 365 for daily. The calculator returns the effective annual yield as a percentage. Use it to compare savings accounts, CDs, or loans that quote the same nominal rate but compound differently.

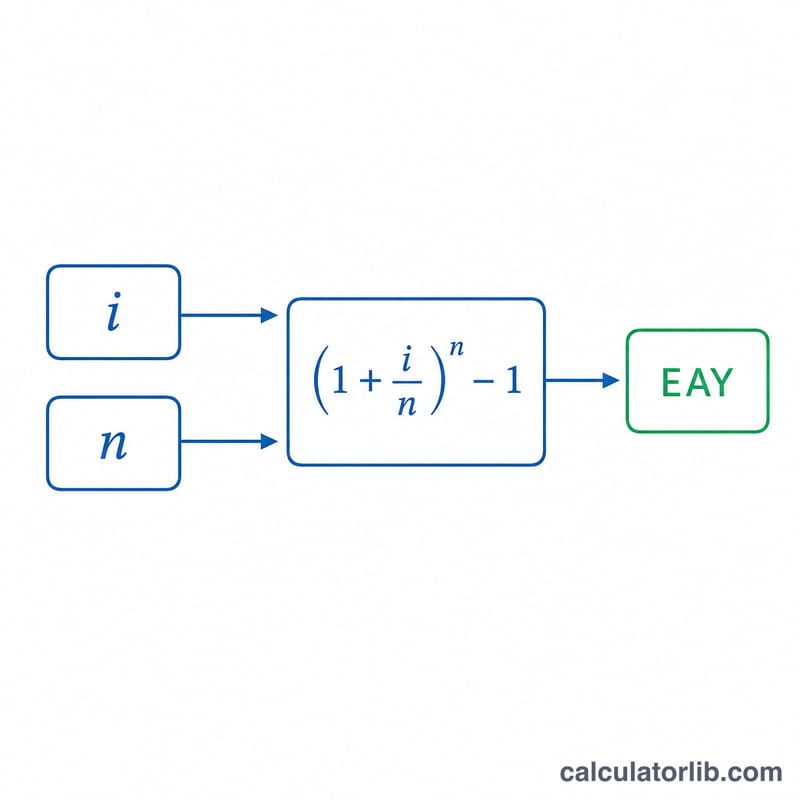

The Formula Explained

The formula is $$\text{EAY} = \left(1 + \frac{i}{n}\right)^{n} - 1$$ where i is the nominal annual rate expressed as a decimal and n is the number of compounding periods per year. Dividing i by n gives the rate per period; raising the growth factor to the power of n compounds it across the whole year; subtracting 1 isolates the gain.

Worked Example

Suppose a savings account quotes a 5% nominal rate compounded monthly (\(n = 12\)). Then $$\text{EAY} = \left(1 + \frac{0.05}{12}\right)^{12} - 1 = (1.0041667)^{12} - 1 \approx 1.05116 - 1 = 0.05116$$ or about 5.116%. The extra 0.116 percentage points over the nominal 5% comes purely from monthly compounding.

FAQ

What's the difference between nominal rate and EAY? The nominal rate ignores compounding frequency; the EAY reflects it, giving the real yearly return.

Is EAY the same as APY? Yes — APY (annual percentage yield) is the same concept used by US banks for deposit accounts.

What if interest compounds annually? With \(n = 1\), the EAY equals the nominal rate exactly, since there is no intra-year compounding.