What is the Effective Annual Rate?

The Effective Annual Rate (EAR), also called the annual equivalent rate or effective interest rate, is the true rate of interest earned or paid on an investment or loan once the effect of compounding is taken into account. A nominal rate of 12% sounds simple, but if interest compounds monthly you actually pay or earn more than 12% over a year. The EAR captures that difference so you can compare products on an apples-to-apples basis.

How to use this calculator

Enter the nominal annual interest rate as a percentage and the number of times interest compounds per year (12 for monthly, 4 for quarterly, 365 for daily, 1 for annually). The calculator returns the effective annual rate, restates your nominal rate, and shows the extra percentage points added purely by compounding.

The formula explained

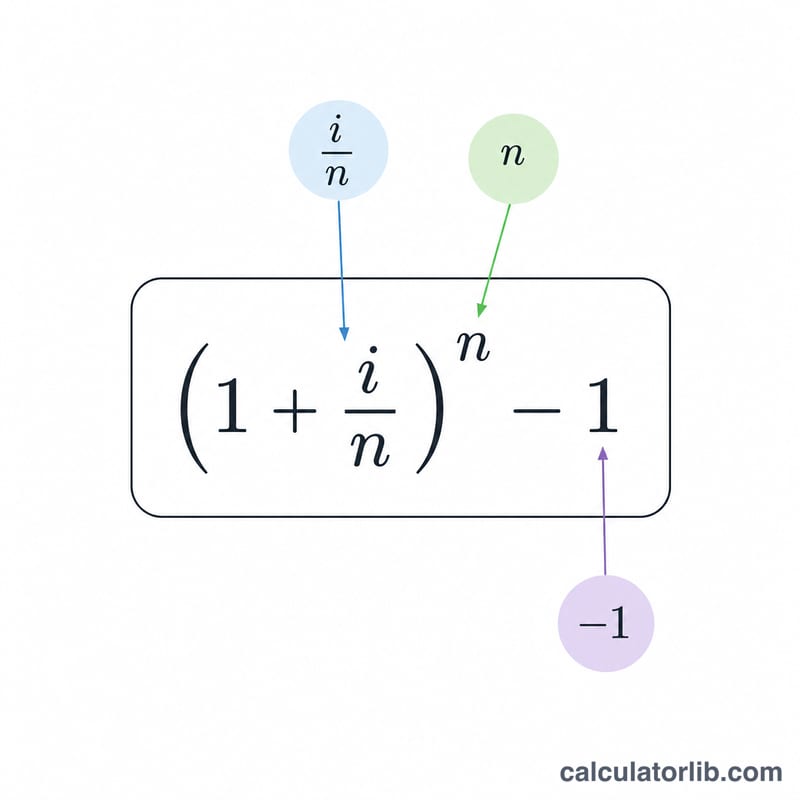

The EAR is given by $$\text{EAR} = \left(1 + \frac{i}{n}\right)^{n} - 1$$ where \(i\) is the nominal annual rate expressed as a decimal and \(n\) is the number of compounding periods per year. Each period earns \(i/n\), and compounding those \(n\) times over the year produces the effective figure. As \(n\) grows, EAR approaches the continuously compounded limit \(e^{i} - 1\).

Worked example

Suppose a credit card charges a 12% nominal annual rate compounded monthly. Here \(i = 0.12\) and \(n = 12\). So $$\text{EAR} = \left(1 + \frac{0.12}{12}\right)^{12} - 1 = (1.01)^{12} - 1 \approx 0.126825,$$ or about 12.68%. The extra 0.68 percentage points is the hidden cost of monthly compounding.

FAQ

Is EAR the same as APR? Not exactly. APR is typically a nominal rate that may exclude compounding effects, while EAR always includes them, making EAR the better comparison tool.

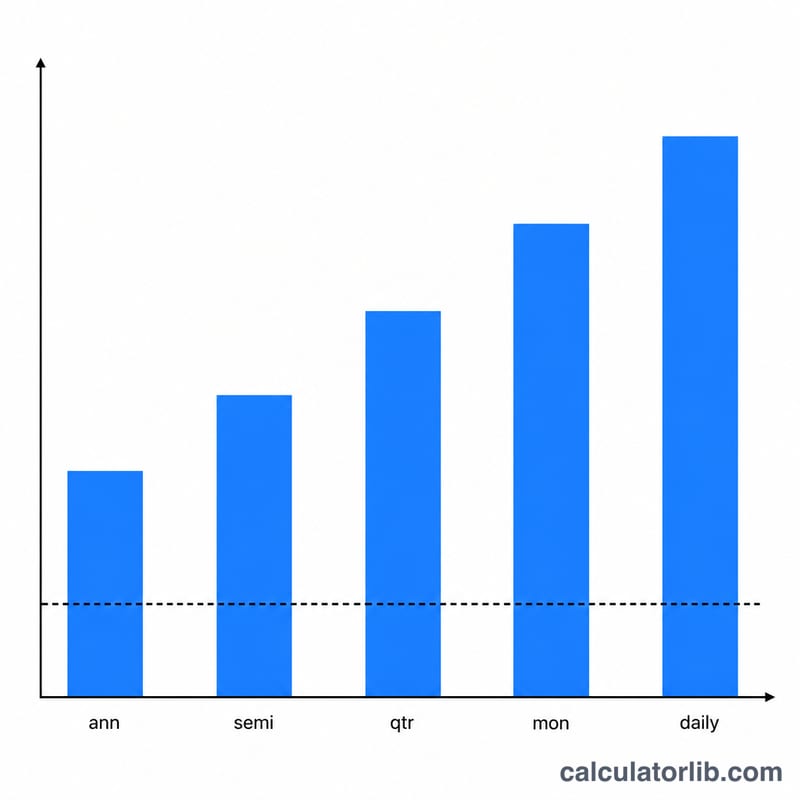

What if interest compounds daily? Use \(n = 365\) (or 360 for some bank conventions). Daily compounding pushes the EAR slightly higher than monthly.

Does a higher compounding frequency always mean a higher EAR? Yes — for the same nominal rate, more frequent compounding produces a higher effective rate, up to the continuous-compounding ceiling.