What Is the Effective Annual Rate (APY)?

The Effective Annual Rate, often shown as APY (Annual Percentage Yield), is the true yearly return on an investment or the true cost of a loan once compounding is taken into account. A nominal rate alone is misleading: 5% compounded monthly actually grows your money faster than 5% compounded once a year. This calculator converts any nominal annual rate into its effective equivalent so you can compare offers on equal footing.

How to Use It

Enter the nominal annual rate as a percentage (for example, 5 for 5%) and the number of compounding periods per year — 1 for annual, 4 for quarterly, 12 for monthly, 365 for daily. The calculator returns the effective annual rate and shows how much extra yield the compounding adds compared with the plain nominal figure.

The Formula Explained

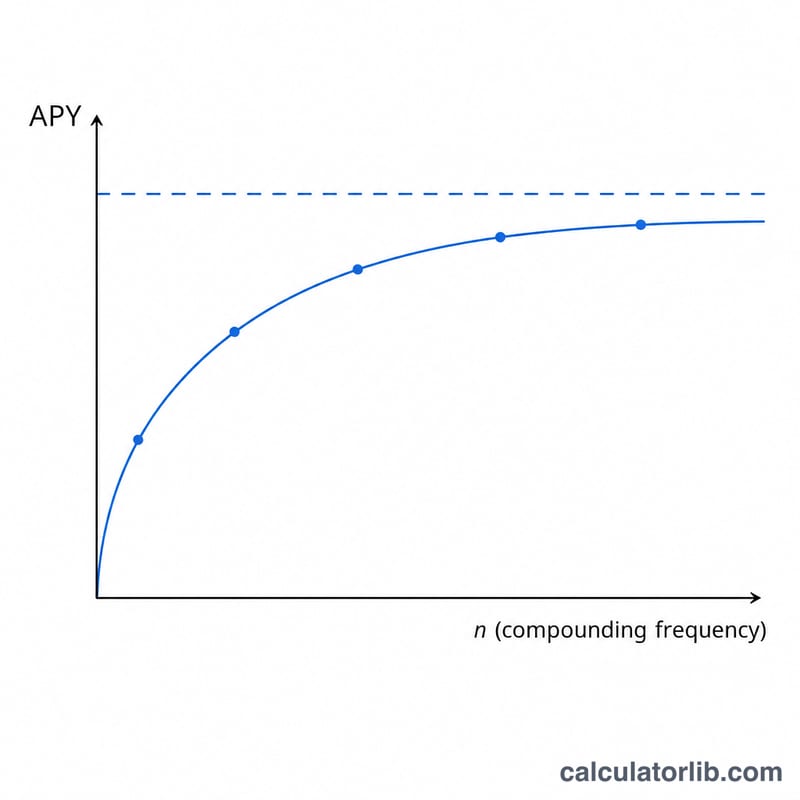

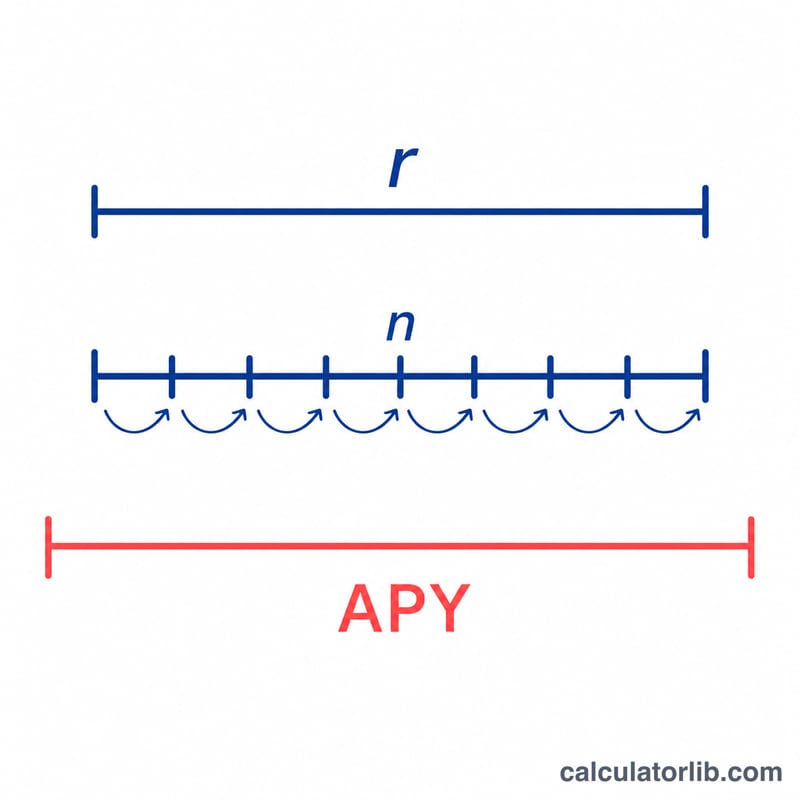

The relationship is $$\text{APY} = \left(1 + \frac{r}{n}\right)^{n} - 1$$ where r is the nominal annual rate written as a decimal and n is the number of compounding periods per year. Each period earns \(r/n\) of interest, and that interest itself earns interest in later periods — the heart of compounding. As \(n\) grows toward infinity, the APY approaches the continuous-compounding limit \(e^{r} - 1\).

Worked Example

Suppose a savings account advertises a 5% nominal rate compounded monthly (n = 12). Then \(r = 0.05\) and $$\text{APY} = \left(1 + \frac{0.05}{12}\right)^{12} - 1 = (1.0041667)^{12} - 1 \approx 0.051162$$ or about 5.1162%. So your money actually grows by roughly 5.12% per year, about 0.12% more than the stated 5%.

FAQ

Is APR the same as APY? No. APR (Annual Percentage Rate) is the nominal rate and ignores intra-year compounding, while APY includes it. APY is always greater than or equal to APR when the rate is positive.

What value of n should I use? Use the frequency stated by the institution: monthly = 12, quarterly = 4, daily = 365, annually = 1.

Why does APY matter? It lets you compare two products with different compounding schedules fairly — the one with the higher APY genuinely pays more.