What Is the Future Value Calculator?

This calculator tells you how much a single lump sum of money will be worth in the future once it has earned compound interest. You enter how much you have today (the present value), the annual interest rate, how long you will invest, and how often interest is compounded. The tool returns the future value (FV) and the Future Value Interest Factor (FVIF) — the multiplier that turns today's dollars into tomorrow's.

How to Use It

Enter the Present Value (your investment amount), the annual Interest Rate as a percent (e.g. 5.25 for 5.25%), the Number of Years (decimals like 3.5 are allowed), and pick a compounding frequency — Daily, Monthly, Quarterly, or Yearly. More frequent compounding produces a slightly higher future value for the same nominal rate.

The Formula Explained

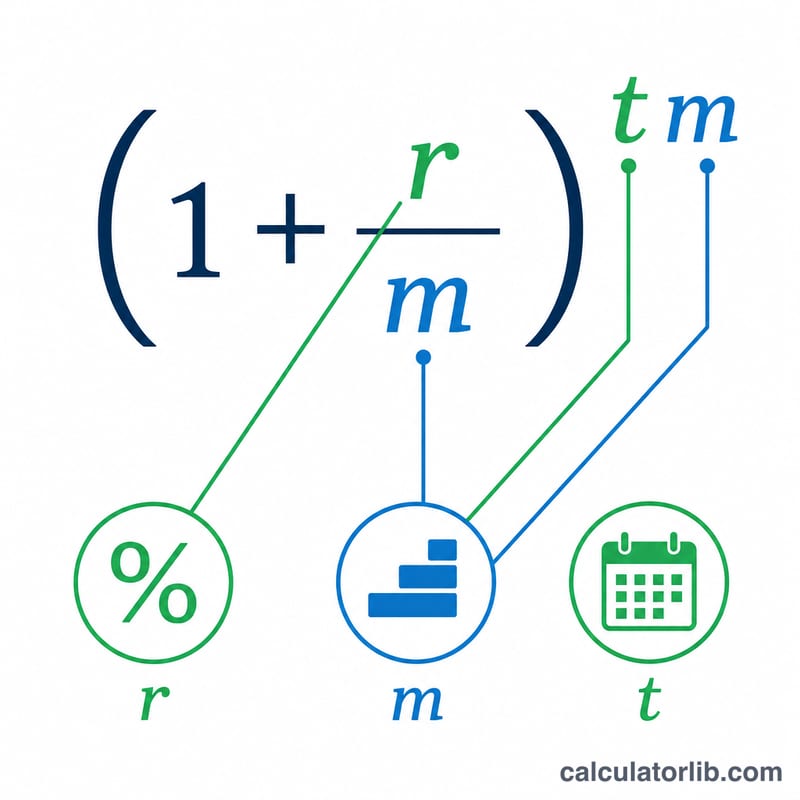

The general compound interest formula is $$FV = PV \times (1 + i)^{n}$$. To use annual inputs we convert: the periodic rate is \(i = (r/100) / m\) and the total number of periods is \(n = t \times m\), where \(m\) is the number of compounding periods per year. The FVIF is simply \((1 + i)^{n}\) — the part that multiplies PV. Because it is computed directly as the multiplier, it stays valid even when PV is zero.

Worked Example

Suppose you invest $12,487.16 for 3.5 years at 5.25% compounded Monthly (\(m = 12\)). Then $$i = 0.0525 / 12 = 0.004375$$ and $$n = 3.5 \times 12 = 42.$$ The $$FVIF = (1.004375)^{42} \approx 1.20123,$$ so $$FV = 12{,}487.16 \times 1.20123 \approx \textbf{15{,}000.00}.$$

Key Terms Defined

- Present Value (PV)

- The amount of money available or invested today — the starting lump sum before any interest is earned.

- Future Value (FV)

- The value of the present sum at a specified future date after compounding, computed as \(FV = PV \times (1+i)^n\).

- FVIF (Future Value Interest Factor)

- The multiplier \((1+i)^n\) that turns a present value into its future value for a given periodic rate and number of periods. \(FV = PV \times FVIF\).

- Nominal annual rate (r)

- The stated yearly interest rate, expressed as a percentage, before accounting for how often interest is compounded within the year.

- Periodic rate (i)

- The interest rate applied in each compounding period, found by dividing the nominal annual rate by the compounding frequency: \(i = \dfrac{r/100}{m}\).

- Compounding frequency (m)

- The number of times per year interest is calculated and added to the balance — for example 1 (annual), 4 (quarterly), 12 (monthly), or 365 (daily).

- Number of periods (n)

- The total count of compounding periods over the investment horizon: \(n = t \cdot m\).

- Term (t)

- The length of time the money is invested, expressed in years.

FAQ

What is FVIF? The Future Value Interest Factor is the growth multiplier: multiply any present value by it to get the future value at the chosen rate, term and compounding.

Does compounding frequency matter? Yes. For a fixed nominal rate, more frequent compounding (Daily > Monthly > Quarterly > Yearly) gives a higher future value because interest earns interest sooner.

Can I use fractional years? Yes. A value like 3.5 years works fine; the math uses a fractional exponent, so the result is precise.