What This Calculator Does

This calculator tells you how large a nest egg you need to invest to generate a chosen amount of passive income every month. It uses the popular "safe withdrawal rate" concept from retirement planning: if you withdraw only a small percentage of your portfolio each year, the balance can — in theory — last indefinitely while still paying you an income.

How to Use It

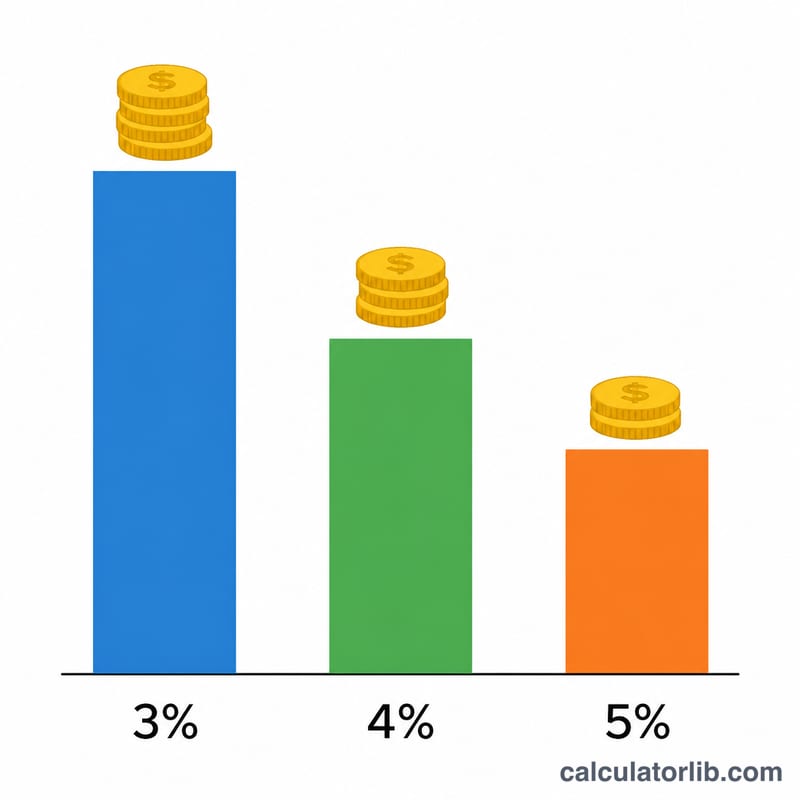

Enter the monthly income you want your investments to produce, then choose a safe withdrawal rate. The classic figure from the Trinity Study is 4% per year, but conservative planners use 3% to 3.5% and more aggressive ones use up to 5%. The calculator converts your monthly target to an annual figure and divides by the rate to show the lump sum you need.

The Formula Explained

First, your desired annual income is your monthly target times 12. Then the required principal is that annual income divided by the withdrawal rate expressed as a decimal: Nest Egg = (Monthly × 12) ÷ Rate.

$$\text{Nest Egg} = \dfrac{\text{Monthly Income} \times 12}{\text{Withdrawal Rate}}$$

A lower withdrawal rate means more safety but a bigger required nest egg, because each dollar of income must be supported by more invested capital.

Worked Example

Suppose you want $4,000 per month and use a 4% withdrawal rate. Annual income is \(\$4{,}000 \times 12 = \$48{,}000\). Divide by 0.04 and you get $1,200,000.

$$\dfrac{\$4{,}000 \times 12}{0.04} = \dfrac{\$48{,}000}{0.04} = \$1{,}200{,}000$$

So you would need a $1.2 million portfolio to safely draw $4,000 a month at 4%.

FAQ

Is 4% really safe? The 4% rule is a historical rule of thumb for a 30-year retirement using a balanced stock/bond portfolio. It is not guaranteed; market crashes, inflation, and longer time horizons can require a lower rate.

Does this account for inflation or taxes? No. The withdrawal-rate model implicitly assumes inflation-adjusted withdrawals, but this tool does not model taxes. Your spendable income after tax may be lower, so budget accordingly.

What rate should I use? Use 3% to 3.5% for a very long or conservative plan, 4% as the classic baseline, and up to 5% only if you accept higher risk of depleting the portfolio.