What This Calculator Does

The Savings Balance After Regular Withdrawals Calculator shows how much money will remain in an interest-bearing account when you take out a fixed amount every period. It models a classic "drawdown" scenario — for example, living off savings in retirement, funding tuition from a college fund, or spending down an inheritance — while the remaining balance keeps earning compound interest.

How to Use It

Enter your starting balance, the amount you plan to withdraw each period, your annual interest rate, the number of years, and how often interest compounds and withdrawals occur (monthly, quarterly, or annually). The calculator converts the annual rate into a periodic rate and projects the balance forward, returning the ending balance, the total amount withdrawn, and the interest earned along the way.

The Formula Explained

The core equation is

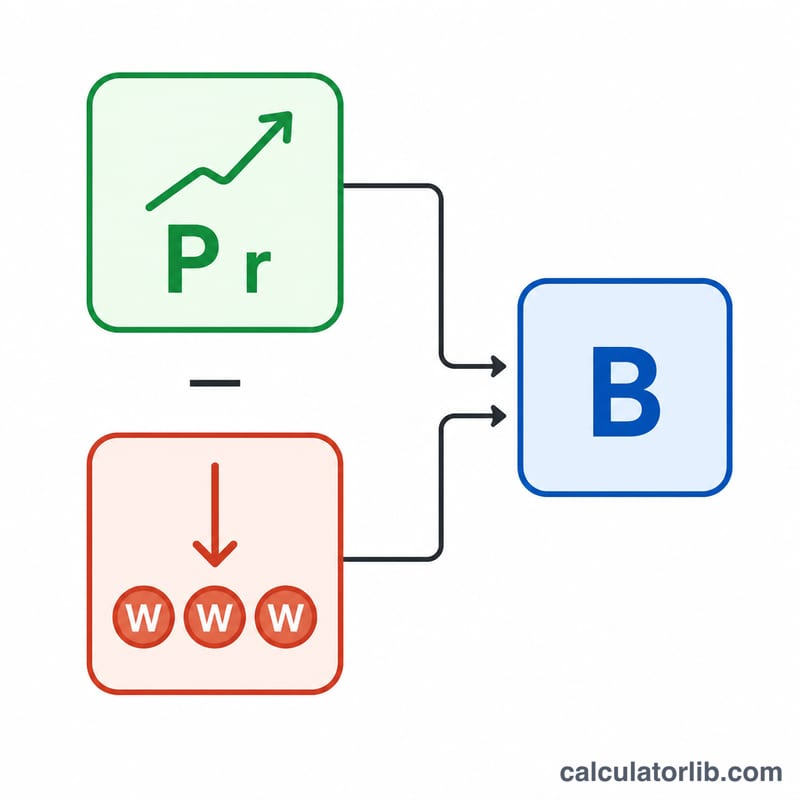

$$B = P(1+r)^n - W\cdot\frac{(1+r)^n - 1}{r}$$where \(P\) is the starting principal, \(r\) is the periodic interest rate (annual rate ÷ frequency), \(n\) is the total number of periods (years × frequency), and \(W\) is the withdrawal per period. The first term grows your principal; the second term is the future value of an annuity representing all the withdrawals. If the rate is zero, the formula reduces to

$$B = P - W\cdot n$$

Worked Example

Suppose you start with $100,000, withdraw $500 per month, earn 5% annually compounded monthly, for 10 years. Here \(r = 0.05/12 \approx 0.0041667\) and \(n = 120\). The growth factor \((1+r)^{120} \approx 1.647009\), so

$$P\cdot\text{growth} \approx \$164{,}700.95$$and the withdrawal term

$$\approx \$500\cdot\frac{0.647009}{0.0041667} \approx \$77{,}641.14$$The ending balance is about $87,059.81, with $60,000 withdrawn over the decade.

FAQ

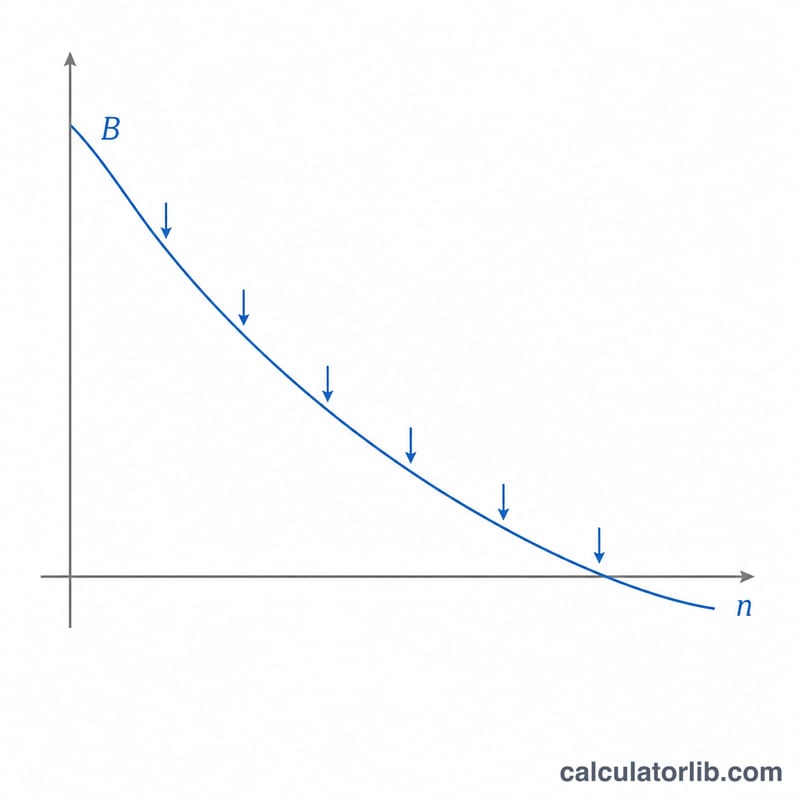

What if my balance runs out? If withdrawals exceed what interest plus principal can sustain, the result will turn negative, signaling the account would be depleted before the term ends.

Are withdrawals taken at the start or end of each period? This calculator assumes withdrawals occur at the end of each period (an ordinary annuity).

Does it account for taxes or inflation? No. Results are nominal pre-tax figures; adjust your inputs if you want real (inflation-adjusted) values.