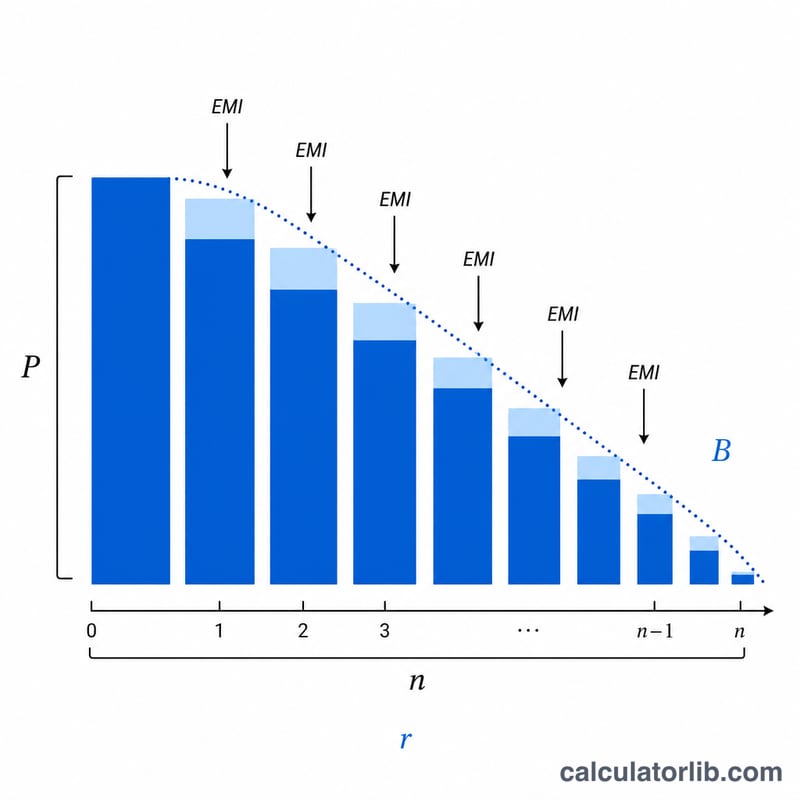

What Is the Loan Balance After Payments Calculator?

This calculator tells you how much you still owe on an amortizing loan (mortgage, auto loan, or personal loan) after a given number of monthly payments. It uses the original loan amount, the annual interest rate, the full term, and the number of payments you have already made to compute the remaining principal balance.

How to Use It

Enter the original loan amount, the annual interest rate as a percentage, the loan term in years, and how many monthly payments you have made so far. The tool returns your outstanding balance plus the fixed monthly payment (EMI), how much principal and interest you have paid to date, and the number of payments remaining.

The Formula Explained

First the fixed monthly payment is found with the standard amortization formula, then the remaining balance after n payments is computed:

$$\text{EMI} = \frac{P\,r\,(1+r)^N}{(1+r)^N - 1}$$

$$B = P(1+r)^n - \text{EMI}\cdot\frac{(1+r)^n - 1}{r}$$

Here \(P\) is the original principal, \(r\) is the monthly rate (annual rate \(\div\) 12 \(\div\) 100), \(N\) is the total number of payments (years \(\times\) 12), and \(n\) is the number of payments already made.

Worked Example

For a $200,000 loan at 6% annual interest over 30 years, \(r = 0.005\) and \(N = 360\). The monthly payment works out to about $1,199.10. After 12 payments, the outstanding balance is approximately $197,543.98 — only a small dent, because early payments are mostly interest.

Remaining Balance Across Different Scenarios

The table below shows how the outstanding principal on a $200,000 loan evolves under different interest rates, terms, and number of payments already made. The monthly payment (EMI) is computed with \(M = P\cdot\dfrac{r(1+r)^{n}}{(1+r)^{n}-1}\), and the remaining balance with \(B = P(1+r)^{p} - M\cdot\dfrac{(1+r)^{p}-1}{r}\), where \(r\) is the monthly rate and \(n\) the total number of payments.

| Rate | Term | EMI | Balance after 12 | Balance after 60 | Balance after 120 |

|---|---|---|---|---|---|

| 4% | 30 yr | $954.83 | $196,449 | $181,461 | $157,597 |

| 4% | 15 yr | $1,479.38 | $190,236 | $148,567 | $83,121 |

| 6% | 30 yr | $1,199.10 | $197,581 | $185,991 | $167,371 |

| 6% | 15 yr | $1,687.71 | $191,684 | $153,232 | $89,648 |

| 8% | 30 yr | $1,467.53 | $198,654 | $190,210 | $176,135 |

| 8% | 15 yr | $1,911.30 | $193,116 | $157,975 | $96,569 |

Notice that after 120 payments the 15-year loans have repaid roughly half the principal, while the 30-year loans — only one-third of the way through their schedule — still owe well over 80% of the original amount. Higher rates also leave a higher balance at every milestone because more of each payment is consumed by interest.

Key Terms Explained

- Principal (P) — the original amount borrowed, before any interest is added. In the formula this is the starting loan balance.

- Monthly rate (r) — the annual interest rate converted to a per-month decimal: \(r = \dfrac{\text{Rate \%}}{1200}\). For example, 6% per year gives \(r = 0.005\) per month.

- Total payments (N) — the full number of scheduled monthly payments over the life of the loan, \(N = 12 \times \text{Term in years}\). A 30-year loan has \(N = 360\).

- Payments made (n or p) — how many monthly payments have already been completed at the point you want the balance for.

- EMI (Equated Monthly Installment, M) — the fixed monthly payment that fully repays the loan over its term, combining both interest and principal in each installment.

- Outstanding / remaining balance (B) — the principal still owed after \(p\) payments. Paying this amount in full would close the loan (excluding any fees).

- Amortization — the process of gradually paying off a loan through scheduled equal payments, where the split between interest and principal shifts over time.

- Principal-vs-interest split — each EMI is divided into an interest portion (rate times the current balance) and a principal portion (the remainder). Early in the loan the interest portion dominates; later the principal portion grows.

Interpreting Your Outstanding Balance

The outstanding balance is what you would need to pay today to settle the loan, ignoring prepayment fees. It equals the original principal grown by interest, minus the accumulated value of all payments you have made so far.

Principal paid to date is simply the original loan amount minus the current outstanding balance. Interest paid to date is the total of all EMIs made so far minus the principal paid — i.e. \(\text{Interest} = p \cdot M - (P - B)\). The number of payments remaining is the total payments \(N\) minus the payments made \(p\).

A key feature of amortizing loans is that early balances fall slowly. Because interest is charged on the full outstanding balance, the first payments are weighted heavily toward interest and only a small slice goes to principal. For example, on a $200,000 loan at 6% over 30 years, after the first 12 payments the balance has dropped only about $2,400 — even though over $14,000 in payments were made. The principal portion grows steadily as the balance shrinks, so progress accelerates in the later years.

The outstanding balance also drives your loan-to-value (LTV) ratio for a secured loan such as a mortgage: \(\text{LTV} = \dfrac{\text{outstanding balance}}{\text{property value}}\). As the balance falls (and if the asset value holds or rises), the LTV improves, which can matter for refinancing or removing mortgage insurance. For a $167,371 balance against a $250,000 property, the LTV would be about 66.9%.

This is general information for understanding loan mechanics, not personal financial advice. Confirm exact figures and payoff amounts with your lender.

FAQ

Why does the balance barely drop early on? In an amortizing loan, early payments go mostly toward interest, so principal reduces slowly at first and faster later.

Does this assume fixed payments? Yes. It models a standard fixed-rate, fully amortizing loan with equal monthly payments and no extra principal payments.

What if my rate is 0%? With a 0% rate, the payment is simply the principal divided by the number of payments, and the balance decreases linearly.