What This Calculator Does

The Loan Principal Remaining Balance Calculator tells you exactly how much you still owe on an amortizing loan after a given number of monthly payments. This is useful for mortgages, auto loans, and personal loans when you want to know your payoff amount, build equity estimates, or plan a refinance. It works for any currency since it deals purely with numbers and percentages.

How to Use It

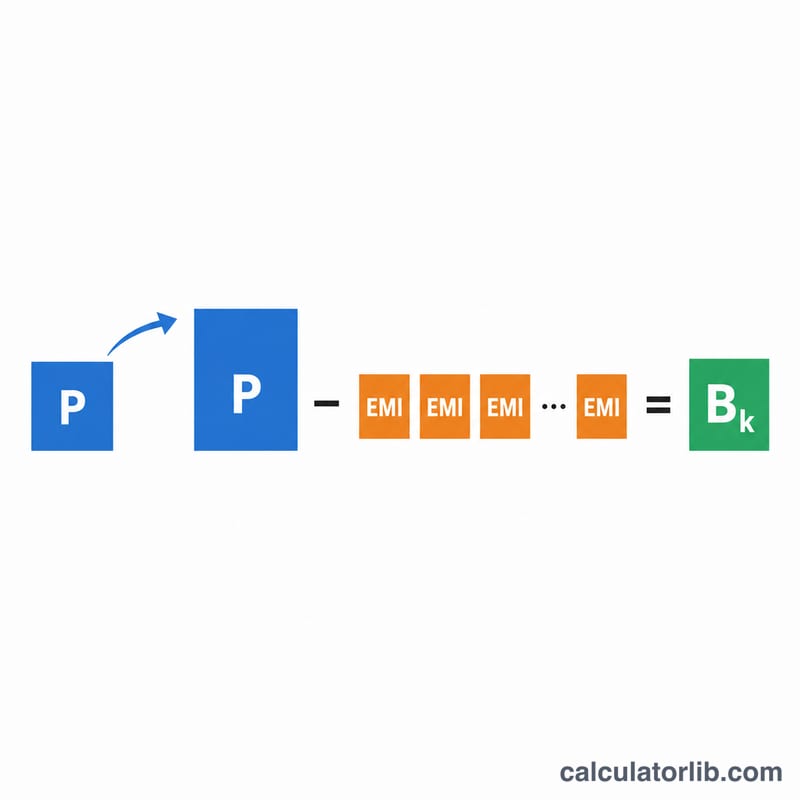

Enter the original loan amount, the annual interest rate, the loan term in years, and the number of monthly payments you have already made. The calculator first derives your fixed monthly payment (EMI), then applies the amortization formula to find the outstanding principal, the amount of principal already paid off, and the total cash paid so far.

The Formula Explained

The remaining balance after k payments is $$B_k = P(1+r)^k - \text{EMI}\cdot\frac{(1+r)^k - 1}{r}$$ where P is the original principal and r is the monthly interest rate (annual rate \(\div\) 12 \(\div\) 100). The EMI itself is $$\text{EMI} = \frac{P\cdot r\cdot(1+r)^n}{(1+r)^n - 1}$$ with n the total number of months. If the rate is zero, the loan amortizes linearly and \(\text{EMI} = P / n\).

Worked Example

For a $200,000 loan at 6% annual interest over 30 years (360 months), the monthly rate \(r = 0.005\). The EMI is about $1,199.10. After 60 payments, \((1.005)^{60} \approx 1.34885\), so the balance $$\approx 200000\cdot 1.34885 - 1199.10\cdot\frac{1.34885 - 1}{0.005} \approx \$186{,}108.71$$ You have paid off roughly $13,891 of principal while paying $71,946 in total.

FAQ

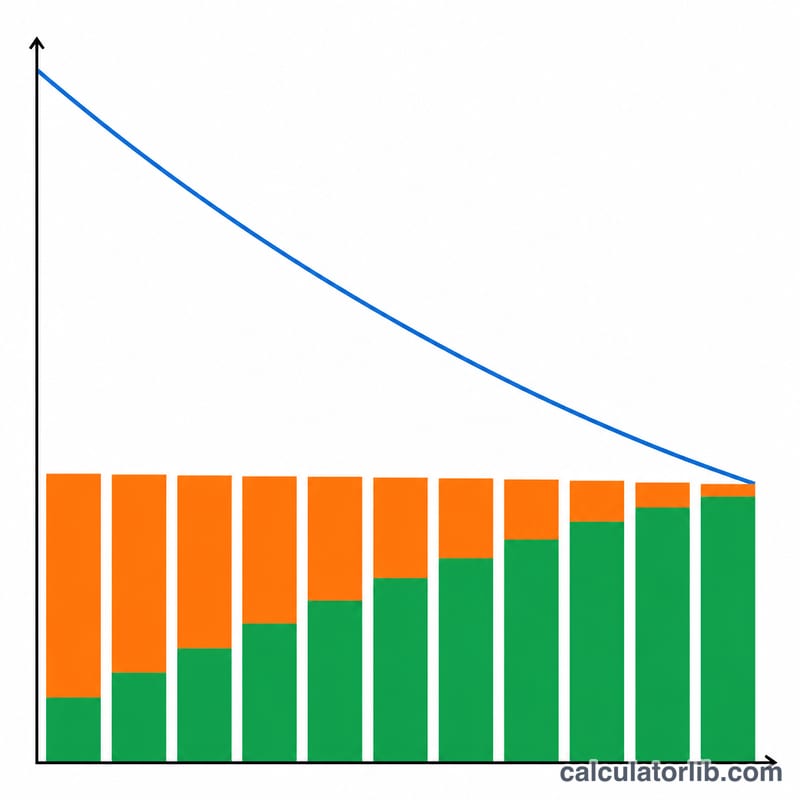

Why is the balance higher than I expect early on? Early payments are mostly interest, so principal drops slowly at first and faster later.

Does this include taxes or insurance? No, it models only the loan's principal and interest.

What if I made extra payments? This formula assumes equal scheduled payments; extra principal payments would lower the balance further.