What This Calculator Does

This tool estimates the federal capital gains tax and depreciation recapture you may owe when selling a rental or investment property in the United States. Figures are estimates only and assume long-term ownership; consult a tax professional for your exact situation. State taxes, the 3.8% Net Investment Income Tax, and Section 121 exclusions are not included.

How to Use It

Enter your sale price and selling costs (agent commissions, closing fees), your original purchase price, the cost of any capital improvements, and the total depreciation you have claimed over the years. Choose your long-term capital gains rate (commonly 0%, 15%, or 20% depending on income). The calculator returns your adjusted basis, total taxable gain, and the tax broken into its two parts.

The Formula Explained

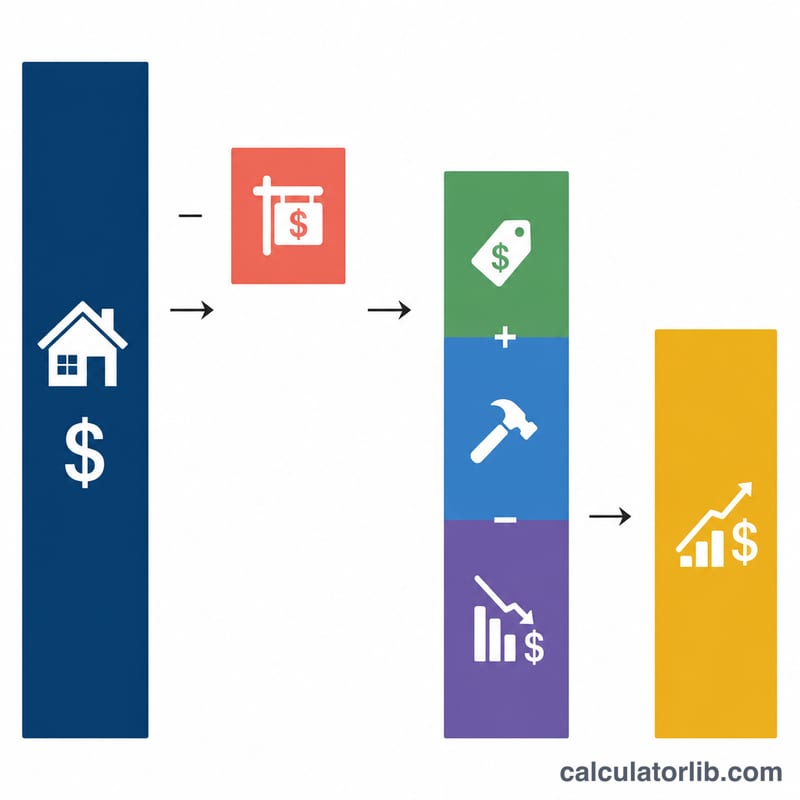

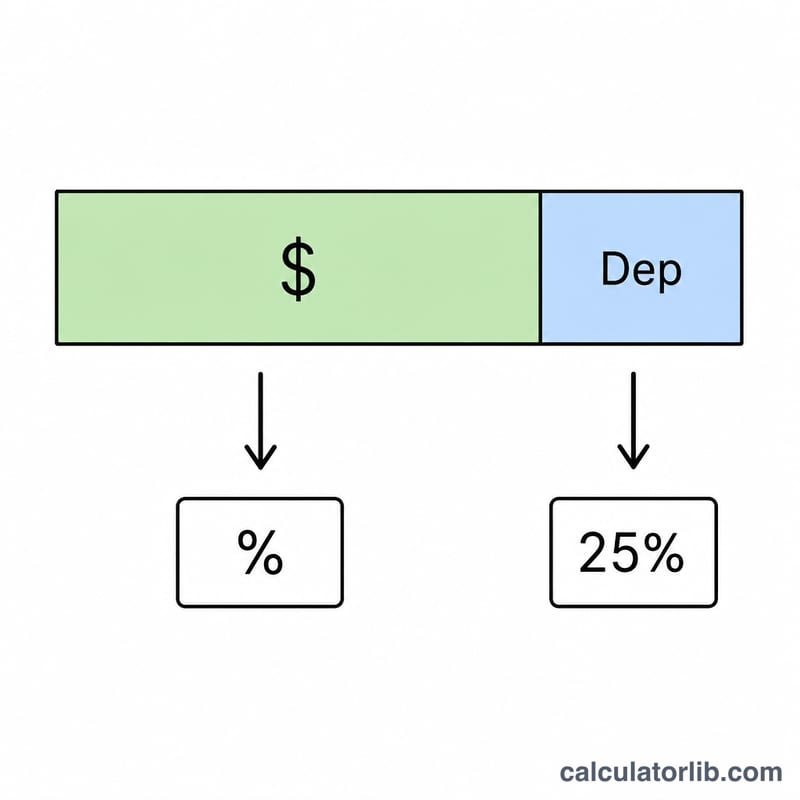

First, the adjusted cost basis equals purchase price + improvements − depreciation. The total taxable gain is net proceeds (sale price − selling costs) minus that basis. Because the IRS taxes the depreciation you previously deducted at up to 25%, that portion is separated out. The remaining capital gain is taxed at your chosen rate. Total tax = capital gain × rate + depreciation × 25%.

$$\begin{gathered} \text{Total Tax} = C \cdot \dfrac{\text{Rate \%}}{100} + 0.25 \cdot \text{Depreciation} \\[1.5em] \text{where}\quad \left\{ \begin{aligned} C &= \max\!\left(0,\; G - \text{Depreciation}\right) \\ G &= \left(\text{Sale} - \text{Costs}\right) - B \\ B &= \text{Purchase} + \text{Improvements} - \text{Depreciation} \end{aligned} \right. \end{gathered}$$

Worked Example

Sell for $500,000 with $30,000 selling costs → net proceeds $470,000. Bought for $300,000, added $20,000 improvements, took $50,000 depreciation → adjusted basis $270,000. Total gain = $200,000. Recapture = $50,000 taxed at 25% = $12,500. Remaining $150,000 capital gain at 15% = $22,500. Total tax = $35,000.

$$\text{Net proceeds} = 500{,}000 - 30{,}000 = 470{,}000$$$$B = 300{,}000 + 20{,}000 - 50{,}000 = 270{,}000$$$$G = 470{,}000 - 270{,}000 = 200{,}000$$$$\text{Recapture} = 50{,}000 \cdot 0.25 = 12{,}500$$$$\text{Capital gain tax} = 150{,}000 \cdot 0.15 = 22{,}500$$$$\text{Total Tax} = 22{,}500 + 12{,}500 = 35{,}000$$FAQ

Why is depreciation taxed separately? Depreciation lowered your taxable income while you owned the property, so the IRS "recaptures" it at sale, capped at a 25% rate.

Does this include the 3.8% NIIT? No. High earners may owe an additional 3.8% Net Investment Income Tax not modeled here.

What rate should I pick? Most filers use 15%; use 20% for high income or 0% for low income, based on your total taxable income.