What the Repayment Calculator does

This Repayment Calculator works out the fixed periodic payment needed to clear a loan over a set term, and breaks that payment down into interest and principal for every period. It is currency-neutral, so it works for mortgages, car loans, personal loans and business debt in any country. You enter the loan details once and the tool returns both the repayment amount and a full amortisation schedule.

The inputs you provide

- Loan amount (\(P\)) – the principal you borrow.

- Interest rate – the annual (nominal) rate as a percentage.

- Compounding frequency – how many times per year interest is applied (e.g. 12 for monthly), used to convert the annual rate into a per-period rate.

- Term – years and months, which set the loan length.

- Payment schedule – how often you pay: every day, week, two weeks, half month, month, quarter, etc. This determines the total number of payments (\(n\)).

The formula explained

The calculator uses the standard amortising-loan payment formula:

$$R = P \cdot \frac{r(1+r)^{n}}{(1+r)^{n} - 1}$$Here \(r\) is the periodic interest rate, found by dividing the annual rate by the compounding number and by 100 (so 6% with monthly compounding gives \(r = 0.06 / 12 = 0.005\)). \(n\) is the total number of payments, derived from your term and payment frequency. The result \(R\) is your equal payment each period. The schedule then takes each period's interest as \(\text{balance} \times r\), treats the rest of \(R\) as principal, and subtracts that principal from the balance.

Worked example

Borrow 20,000 at 6% annual interest, compounded monthly, repaid monthly over 5 years (\(n = 60\), \(r = 0.005\)):

- $$R = 20{,}000 \times \frac{0.005 \times 1.005^{60}}{1.005^{60} - 1} \approx 386.66 \text{ per month.}$$

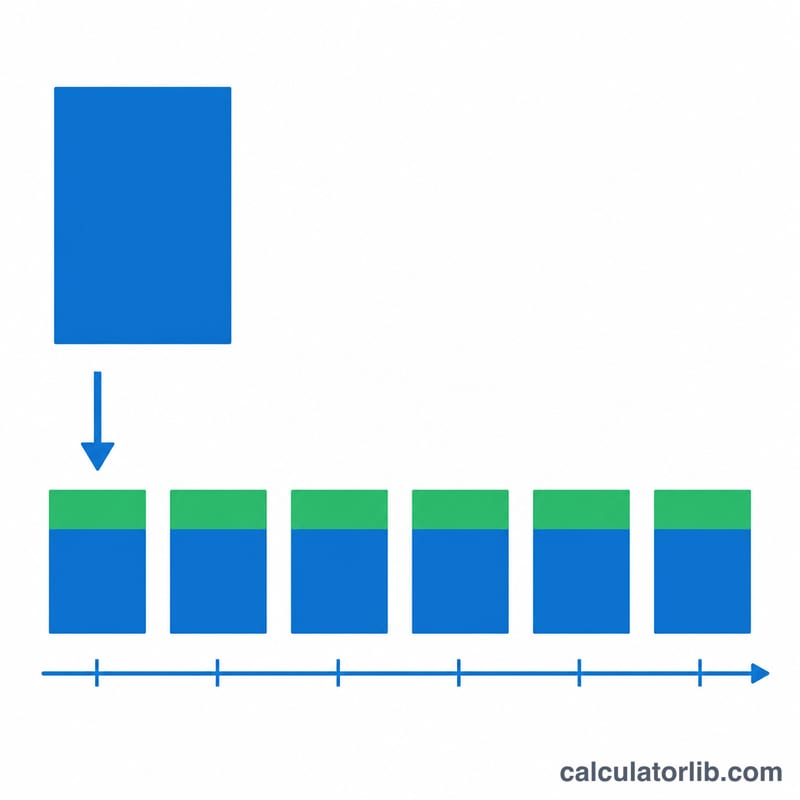

- First payment interest = \(20{,}000 \times 0.005 = 100\); principal = \(286.66\); balance falls to \(19{,}713.34\).

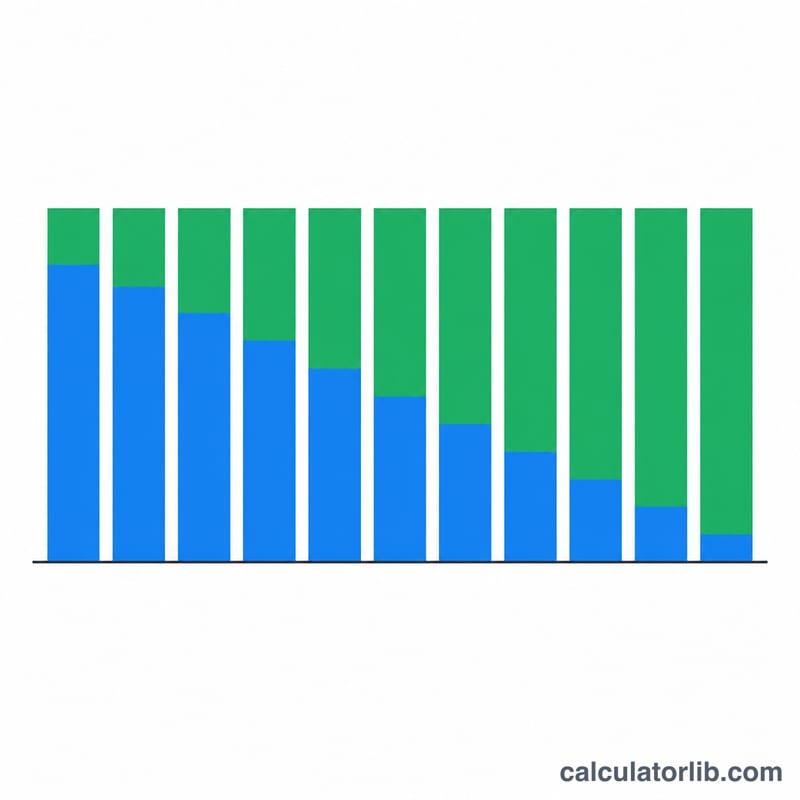

- Over time interest shrinks and principal grows, until the balance reaches zero at payment 60.

FAQ

Why does my early payment go mostly to interest? Interest is charged on the outstanding balance, which is highest at the start. As the balance drops, the interest portion of each fixed payment falls and more goes to principal.

How does changing the payment frequency affect things? Paying more often (e.g. fortnightly) increases the number of payments \(n\) and applies the per-period rate more frequently, which usually lowers each instalment and total interest.

Is the interest rate I enter the annual rate? Yes. The tool divides it by your chosen compounding frequency to get the true per-period rate, so always enter the headline annual percentage.