What this calculator does

The Loan Repayment Calculator estimates your regular payment, the number of payments per year, the total interest you will pay, and the total cost of any loan. Unlike basic tools, it lets you choose how interest compounds and how often you pay separately, then mathematically reconciles the two so the result is accurate even when those frequencies differ. It works for any currency and any country.

The inputs you enter

- Loan Amount – the principal you borrow.

- Loan Term (years) – how long you take to repay.

- Annual Interest Rate (%) – the nominal yearly rate.

- Compound Frequency – Daily, Weekly, Monthly, Quarterly, or Annually (how often interest is added).

- Payment Frequency – Weekly, Bi-weekly, Monthly, Quarterly (how often you make a payment).

The formula explained

The calculator first turns the nominal rate into an Effective Annual Rate (EAR) based on your compounding choice:

EAR = (1 + rate / n)n − 1, where n = compoundings per year.

It then converts the EAR into a rate that matches your payment frequency (p payments per year):

payment rate i = (1 + EAR)1/p − 1.

Finally it applies the standard amortising payment formula over the total number of payments (N = years × p):

Payment = P × [ i (1 + i)N ] / [ (1 + i)N − 1 ].

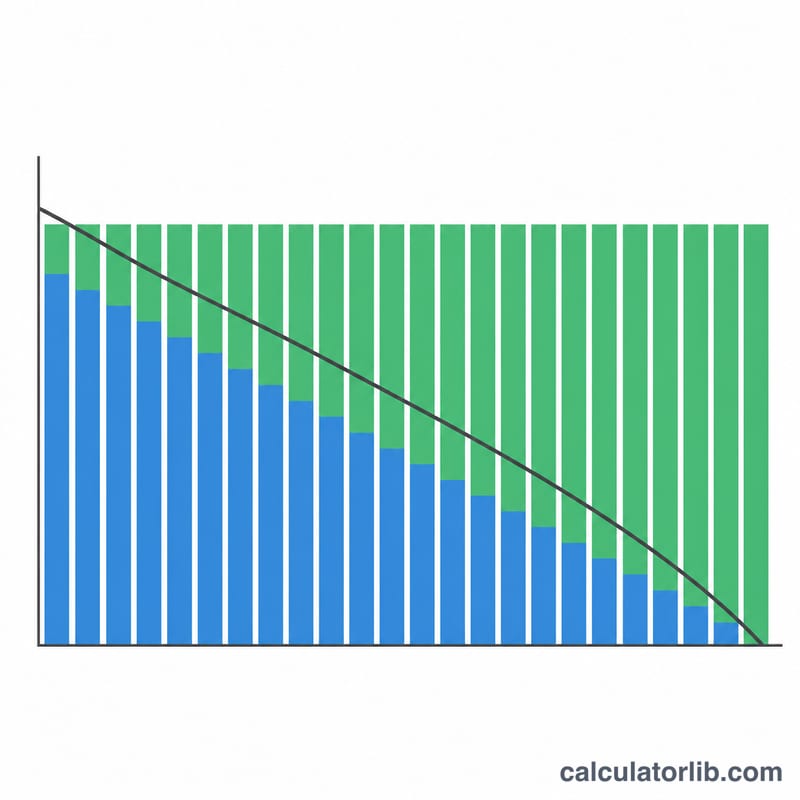

If the rate is zero, the payment is simply principal ÷ total payments. Total interest = (Payment × N) − Principal, and total cost = Payment × N.

Worked example

Borrow $20,000 over 5 years at 6% interest, compounded monthly, paid monthly. EAR = (1 + 0.06/12)12 − 1 ≈ 6.168%. The monthly payment rate ≈ 0.5%, with N = 60 payments. The payment works out to roughly $386.66 per month. Over 60 payments that is about $23,200 total cost and around $3,200 in interest.

FAQ

Why separate compounding and payment frequency? Lenders may compound interest more often than you pay. Converting through the EAR ensures your payment reflects the true cost rather than ignoring the mismatch.

Does paying bi-weekly save money? Bi-weekly (26 payments a year) splits the cost into smaller, more frequent chunks and slightly reduces total interest versus monthly because principal falls faster.

Is this an exact quote? No. It is an estimate. Real loans may include fees, rounding rules, or different day-count conventions, so confirm figures with your lender.