What This Calculator Does

The Student Loan Repayment Calculator estimates what you'll pay each month on a fixed-rate, fully amortising student loan. Enter three figures and it returns your monthly payment, the total amount you'll repay over the life of the loan, and the total interest cost. It also builds a full month-by-month amortisation schedule so you can see how each payment splits between interest and principal. The dollar ($) inputs make this most relevant to borrowers in the United States, but the maths works for any fixed-rate instalment loan.

The Three Inputs

- Loan Amount ($): the principal you borrowed (or your current balance).

- Annual Interest Rate (%): your nominal yearly rate, e.g. 5.5.

- Loan Term (years): how long you'll take to repay, e.g. 10.

The Formula

The calculator uses the standard amortising loan payment formula:

$$M = P \cdot \frac{i\,(1+i)^{n}}{(1+i)^{n}-1}$$where P is the loan amount, i is the monthly interest rate (annual rate ÷ 12 ÷ 100), and n is the number of payments (years × 12). Total payment is \(M \times n\), and total interest is the total payment minus the principal. For the schedule, each month's interest equals the remaining balance \(\times\, i\), the rest of the payment reduces principal, and the balance shrinks accordingly until it reaches zero.

Worked Example

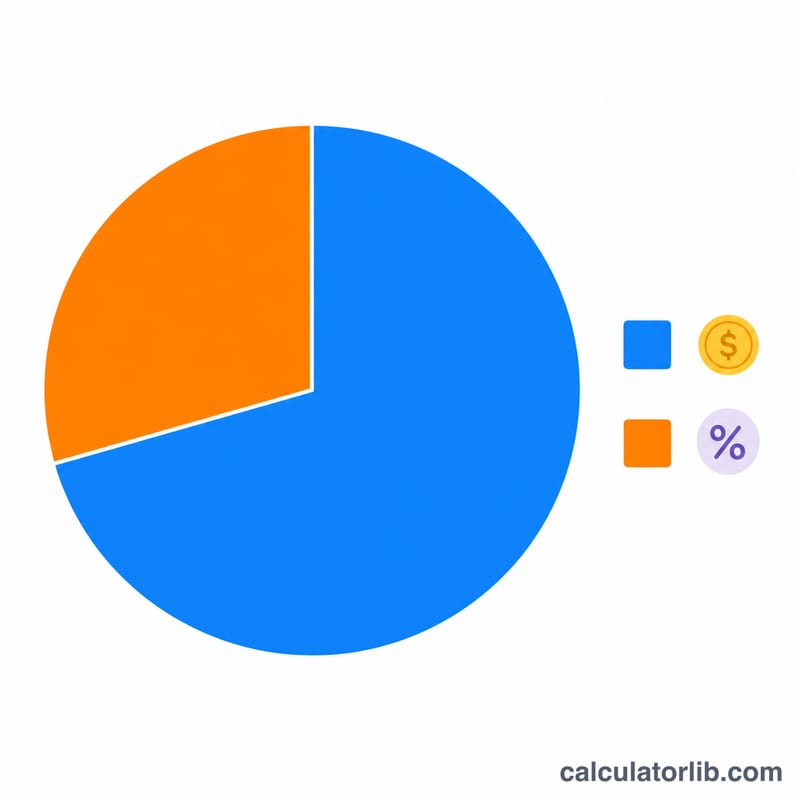

Suppose you borrow $30,000 at 5.5% over 10 years:

- Monthly rate \(i = 5.5 \div 12 \div 100 = 0.0045833\)

- Payments \(n = 10 \times 12 = 120\)

- Monthly payment \(M \approx\) $325.59

- Total repaid \(\approx\) $39,070

- Total interest \(\approx\) $9,070

In month one, interest is about $137.50 and roughly $188 goes to principal — and that principal share grows every month.

FAQ

Why does so much early payment go to interest? Interest is charged on your remaining balance, which is highest at the start. As the balance falls, the interest portion shrinks and more of each fixed payment chips away at the principal.

How can I cut total interest? Choosing a shorter term raises the monthly payment but lowers total interest dramatically. Paying extra toward principal also reduces the balance faster than the schedule shows.

Does this include fees or variable rates? No. It assumes a single fixed rate and no origination fees, late charges or rate changes, so treat the result as a clean baseline estimate.