What this calculator does

The Loan Repayment Schedule Calculator works out your periodic payment and produces a complete amortization table showing the interest portion, principal portion, and remaining balance for every payment. It supports two common repayment methods, optional rate changes part-way through the loan, and an initial grace (deferment) period during which only interest is charged. The underlying math is standard amortization and applies to any currency.

How to use it

Enter the loan amount (choose plain currency units or the x10,000 "man-yen" unit), select the repayment method, frequency, and rounding rule, then enter the interest rate and term. For a fixed-rate loan, set the "rate thereafter" equal to the initial rate. Leave the start year blank if you only want period numbers instead of calendar dates.

The formula explained

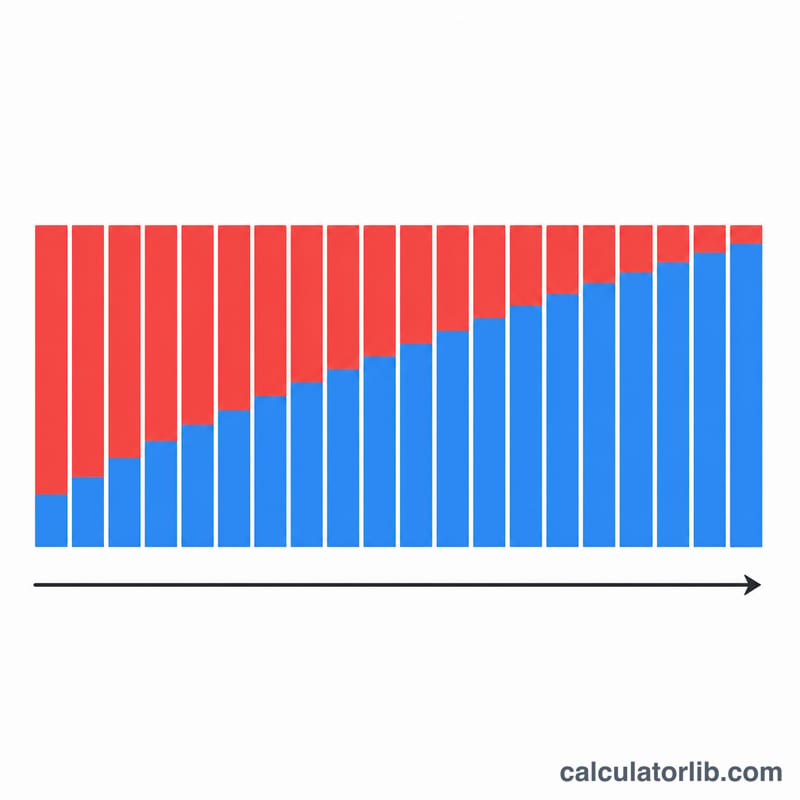

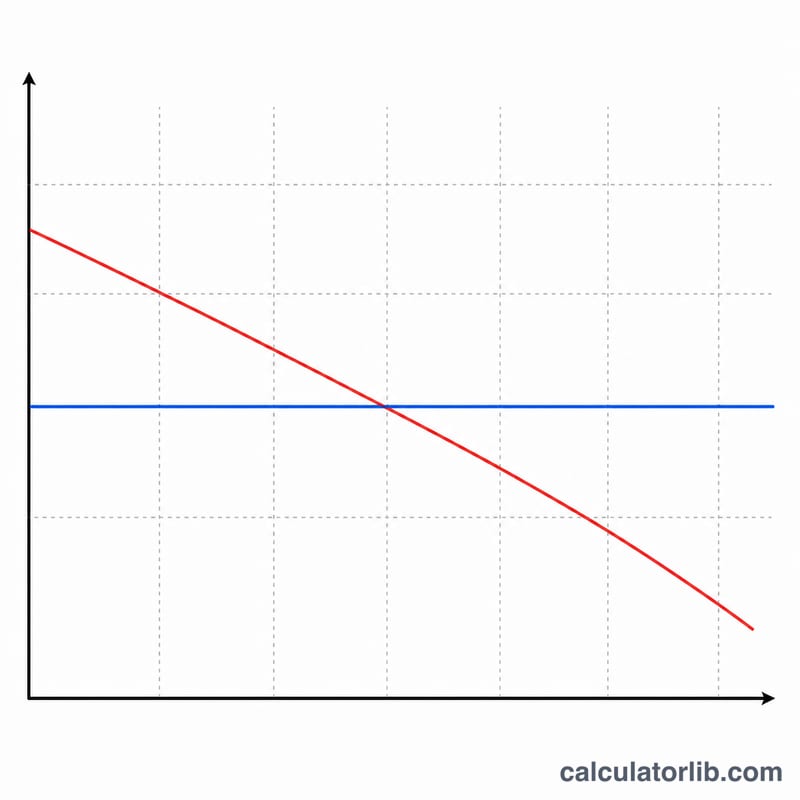

For the equal total payment method, each constant-rate phase uses $$A = \frac{B \cdot i}{1 - (1 + i)^{-n}}$$ where \(B\) is the current balance, \(i\) is the per-period rate (annual rate / 100 / payments per year), and \(n\) is the number of remaining payments. Each period the interest equals \(B \cdot i\) and the rest reduces principal. For the equal principal method, the principal portion stays constant at \(P/n\) while interest declines, so total payments fall over time. The final payment is adjusted to clear any rounding remainder so the balance closes at exactly zero.

Worked example

Borrow 10,000,000 at a fixed 2% over 10 years, paid monthly. Per-period rate \(i = 0.02/12 = 0.00166667\) and \(N = 120\). Payment $$A = \frac{10{,}000{,}000 \times 0.00166667}{1 - 1.00166667^{-120}} \approx 92{,}013 \text{ per month}$$ Total repaid is about 11,041,560, so total interest is roughly 1,041,560.

FAQ

Why does the last payment differ? Rounding each payment leaves a small residual, which the final payment absorbs so the balance reaches zero.

What is a grace period? During the grace period you pay interest only; principal repayment begins afterward and is amortized over the remaining payments.

Is this accurate for my lender? Results are informational. Banks differ in rounding and day-count conventions, so your actual schedule may vary slightly.